Power Up Smarter: Emerging Trends Shaping the Future of Energy Drinks in 2025 and Beyond

Other |

2026-04-24 10:18:26

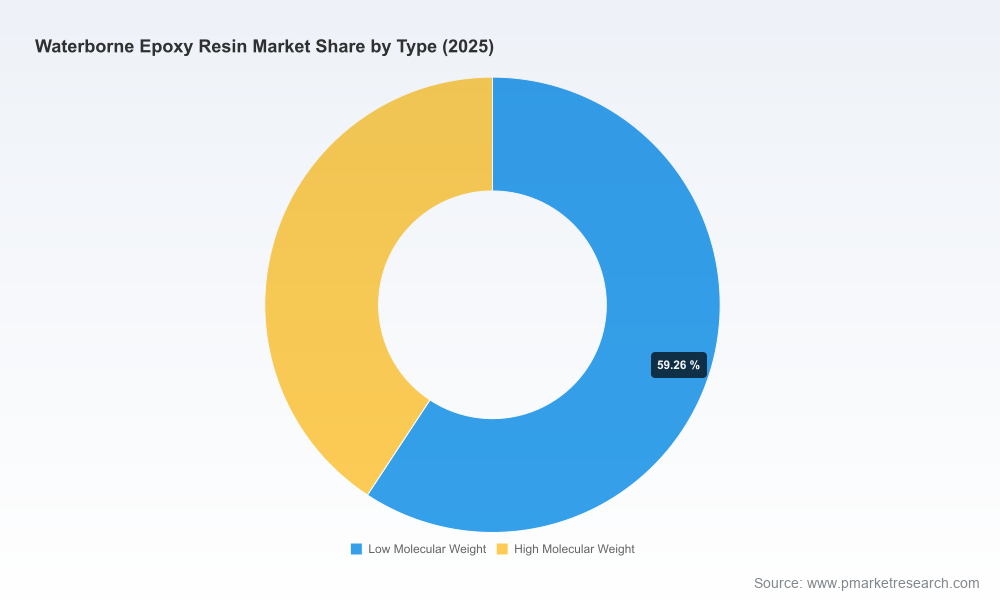

The global waterborne epoxy resin market has transitioned from niche sustainability play to a core strategic arena for coatings, adhesives and composites producers. Our analysis shows the market expanding from approximately USD 3,078.2 Million in 2020 to USD 4,230.0 Million in 2025 (base year), with a projected compound annual growth rate (CAGR) of 7.8% across the 2026–2032 forecast period. By 2032 the market size is estimated to exceed USD 7,100 Million.

Waterborne Epoxy Resin Market

These headline figures understate an important feature: market structure is moderately concentrated, with the top three and five participants holding meaningful but not overwhelming shares — a market that rewards scale and technical differentiation. For 2026 corporate planning, this market profile creates a narrow runway where tactical moves (capacity deployment, reformulation, and targeted partnerships) will materially alter competitive positioning.

Waterborne Epoxy Resin Market

Regulatory inflection points are compressing time-to-market for reformulated chemistries. Public policy drivers — including VOC limits and restrictions on legacy precursors — are reshaping product roadmaps and capital plans for coatings and raw-material producers.

Waterborne Epoxy Resin Market

Raw-material and supply-chain volatility requires companies to convert forecast uncertainty into robust hedging and sourcing strategies; both procurement and R&D must be aligned to avoid margin erosion and delivery disruptions.

Commercially, buyers are bifurcating: procurement-driven large accounts prize total cost of ownership and regulatory compliance, while mid-market buyers value turnkey formulations and rapid technical support. This necessitates differentiated GTM models within supplier organizations.

This report is designed as a practical toolkit for 2026 planning. It goes beyond narrative and provides executable assets that procurement, R&D, strategy and corporate development teams can deploy immediately:

Top-line market model (2020–2032) with scenario toggles — base, accelerated sustainability adoption, and regulatory shock — enabling sensitivity testing of volume and revenue outcomes under alternate assumptions.

Supplier and technology scorecards that benchmark producers on formulation capability, low-VOC qualifications, supply-chain resilience, and commercial reach — structured to inform sourcing and M&A screening.

Regulatory impact matrix and compliance playbook mapping EPA, REACH and domestic standards (including China’s clean air initiatives) to product attributes and certification steps.

Raw-material stress-test models that quantify margin exposure to bisphenol A (BPA) and epichlorohydrin price swings, along with recommended hedging and substitution pathways.

Go-to-market playbooks for four commercial archetypes: global integrators, regional specialists, formulation innovators, and toll-manufacturing partners — including channel KPIs and a prioritized pilot program checklist.

M&A and partnership heatmap highlighting targets by capability (bio-based chemistries, curing technology, low-VOC dispersions) and playbook for transaction diligence focused on regulatory liabilities and IP strength.

Executive dashboards and board-ready slide packs synthesizing the data into investment cases for capex, plant siting, and R&D pipeline funding.

Leading chemical companies have already embedded waterborne epoxies into their core portfolios, leveraging global supply bases, formulation ecosystems, and channel relationships. PW Consulting’s competitive benchmarking centers on firms with demonstrable capabilities in waterborne dispersions, hardener systems, and low-VOC productization. Selected profiles in our study include:

Allnex — Specialist in waterborne epoxy dispersions and two-component hardener systems; recent capacity expansions signal a strategic bet on Asian demand and faster commercialization pathways for eco-oriented resins.

Huntsman Corporation — Brings established Araldite branding and industrial/architectural coatings reach; its global formulation labs remain an advantage for high-spec applications.

Evonik Industries AG — Focused on waterborne dispersions for flooring, corrosion protection and OEM coatings; strong technical collaborations with end-users are a differentiation point.

Olin Corporation — Offers epoxy platforms and recently introduced curing agents targeted at durability in harsh environments; its innovation cadence is an important benchmark for competitive response.

Kukdo Chemical, ADEKA, and DIC — Regional and technology specialists with compliant low-VOC resins and market access in Asia; they illustrate the competitive mix of global incumbents and locally strong players.

Recent industry moves reinforce two strategic themes. First, new product launches focused on CMR-free and low-VOC portfolios demonstrate technical differentiation as a primary route to commercial share. Second, capacity expansions in Asia and product introductions in North America and Europe point to a dual-track approach: volume scale plus formulation leadership. PW Consulting quantifies concentration dynamics (top-three and top-five shares) to guide where scale vs. niche bets are most profitable.

The market’s growth is propelled by environmental regulation, customer demand for low-emission solutions, and end-use growth in infrastructure and industrial coatings. Yet several interlocking risks demand active management:

Precursor regulation: Bisphenol A (BPA) and epichlorohydrin — key precursors — face growing regulatory scrutiny and reformulation pressure due to health and environmental concerns. REACH and similar frameworks have already triggered ingredient substitution programs in Europe.

VOC constraints: EPA and major national programs have tightened VOC ceilings for industrial and architectural coatings, accelerating adoption of waterborne systems but also raising qualification hurdles for performance parity.

Supply volatility: Epichlorohydrin logistics and capacity disruptions have produced price spikes historically; companies without diversified sourcing and strategic inventory plans are exposed to margin compression.

Innovation treadmill: Achieving durability, adhesion and chemical resistance with low-VOC or bio-based systems remains technically challenging. Firms that under-invest in application-specific testing risk costly warranty exposure and lost contracts.

Based on the market model and scenario analysis, PW Consulting recommends a prioritized set of actions tailored to mid-size and large manufacturers facing 2026 decisions:

Accelerate formulation roadmaps toward BPA-free and halogen-free chemistries with funded pilot lines and accelerated qualification timelines for key OEMs and infrastructure customers.

Deploy a two-tier supply strategy: secure long-term contracts for critical precursors with multiple geographic suppliers, and create a rotational hedging program for price spikes.

Pursue targeted M&A or JV activity to acquire niche capabilities (e.g., bio-based epoxy platforms, advanced curing agents) rather than broad roll-ups; use our M&A heatmap to triage targets by technical fit and regulatory cleanliness.

Invest in demonstrable compliance certification and end-user trials in regulated geographies; regulatory proof points materially shorten procurement cycles for large industrial customers.

Optimize manufacturing footprint using our site-selection model: balance proximity to key customers with access to secure precursor supply and regulatory risk exposure.

Differentiate commercially through value-added services — formulation support, on-site testing, and lifecycle assessments — converting technical expertise into sticky revenue streams.

This document is intentionally directional. The full PW Consulting report contains the granular tools required to convert these strategic recommendations into operational plans: editable financial models, supplier scorecards, detailed regulatory mapping, and a prioritized action matrix. We have purposely withheld granular segment tables and proprietary company-level revenue splits in this brief to ensure that executives access the full analytical toolkit hosted on our report portal.

For teams running 2026 annual planning, corporate development, or R&D portfolio reviews, the next immediate steps are:

Request the full PW Consulting Waterborne Epoxy Resin Market Report to obtain the scenario-enabled market model and supplier scorecards.

Run the raw-material stress-test against your 2026 procurement plan using our hedging and substitution recommendations.

Use the M&A heatmap to create a shortlist of inorganic targets or partners for rapid capability acquisition; prioritize deals that close technical gaps on low-VOC and BPA-free chemistries.

PW Consulting’s research equips leaders to convert a 7.8% CAGR market trajectory into profitable growth rather than reactive compliance spending. The coming 18 months will determine which companies establish durable advantage in the waterborne epoxy ecosystem — those that align regulatory foresight, sourcing resilience and formulation leadership will outpace peers. For the complete analytical kit and operational templates, please consult the full report available through PW Consulting.

For detailed analysis of this topic, please visit the official page:Waterborne Epoxy Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com