Kombucha Market Expansion at 14.8% CAGR Fueled by Probiotic Trends

Food |

2026-04-09 14:23:22

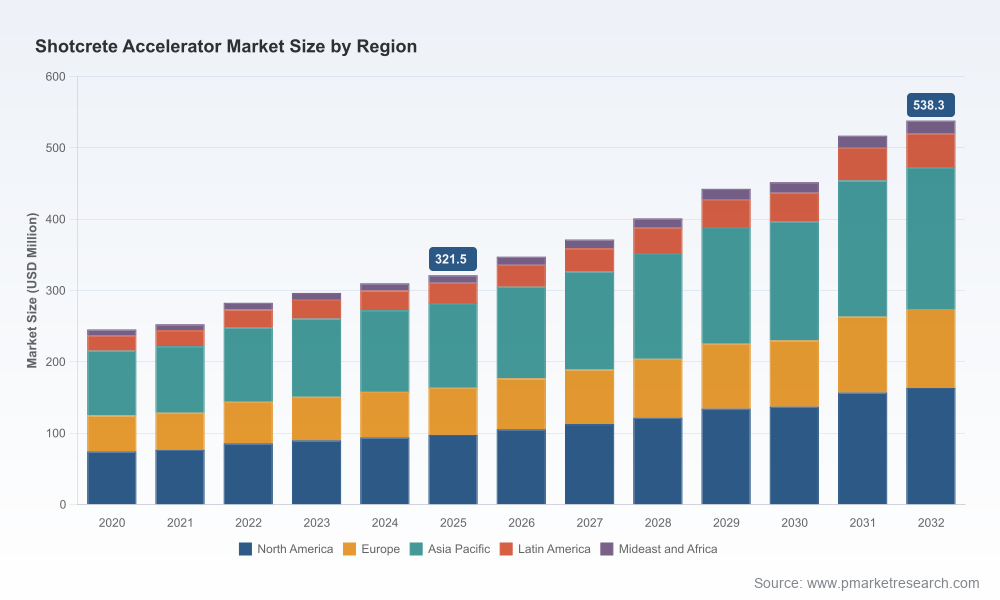

PW Consulting’s new Shotcrete Accelerator Market report (base year 2025) delivers an evidence-based, decision-ready playbook for executives navigating the accelerating underground-construction and mining rebound. Built on a five-year historical review (2020–2025) and a forward-looking forecast (2026–2032), the study quantifies industry momentum—the global market reached USD 321.5 Million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 7.85% through the forecast horizon—while translating that macro trajectory into practical strategic imperatives for 2026.

Shotcrete Accelerator Market

Timing: 2026 is a watershed year—capital-intensive tunneling programs, post‑pandemic infrastructure catch‑ups and a selective recovery in mining capex are converging. The projection path to mid‑2030s upside means near‑term decisions will amplify returns across the cycle.

Shotcrete Accelerator Market

Actionability: The report couples market sizing and scenario projections with supplier-level benchmarking, margin stress tests, raw‑material exposure maps and go‑to‑market playbooks—designed so procurement, R&D and corporate development teams can translate insight into initiatives within 90 days.

Shotcrete Accelerator Market

Risk‑to‑opportunity framing: Volatility in feedstock and regulatory shifts are creating both supply‑side strain and innovation windows. Our analysis isolates the levers that separate price‑sensitive manufacturers from premium, low‑rebound solution providers.

After a steady recovery period from 2020–2025, the shotcrete accelerator market is entering a high‑growth phase. The market size in 2025 (USD 321.5 Million) is expected to follow an upward trajectory through 2032, underpinned by continued tunneling and underground infrastructure investment, renewed mining activity in specific commodities, and broader adoption of mechanized wet‑mix processes. With a compounded growth rate of 7.85% over the forecast period, the sector presents attractive scale economics for both specialty-chemical incumbents and focused regional players.

Regulatory and product migration: The industry is witnessing a structural shift away from legacy sodium‑silicate chemistries toward alkali‑free gel and liquid accelerators. Regulatory drivers—particularly stringent discharge and worker‑safety standards in sensitive jurisdictions—are accelerating adoption of lower‑alkalinity formulations and influencing project specifications.

Raw‑material exposure and margin resilience: Feedstock cost volatility remains a core operational risk. Energy‑related disruptions have translated into meaningful price swings for nitrate‑ and sulfate‑based inputs in recent seasons, pressuring margins for manufacturers with thin pass‑through mechanisms. Aluminum sulfate and calcium‑based feedstocks are singled out as recurring pressure points.

Technology integration and system selling: Equipment suppliers and full‑system integrators are increasingly bundling accelerators with spray robotics and delivery systems. This trend creates opportunities for accelerators to be positioned as differentiated system components (performance guarantees, rebound reduction, compatibility warranties) rather than commodities.

Channel and format evolution: While dry‑mix (bagged) accelerators retain strategic relevance for distributed repair and remote mining installations, wet‑mix and preblended system formats are gaining share in large tunneling contracts due to productivity and consistency benefits. Contracting patterns are therefore shifting procurement toward fewer, long‑tenor suppliers.

The market exhibits a medium level of concentration with the top three vendors representing a material portion of global capacity and the top five accounting for a clear majority. This structure favors scale players that can combine formulation expertise with global distribution, while leaving strategic openings for niche players focused on regional specialties, low‑rebound chemistries, or system integration.

Sika AG (Baar, Switzerland) – Recognized for its Sigunit® alkali‑free liquids and powder portfolio, Sika combines product breadth with deep tunneling project references, positioning it to win specification‑driven contracts in demanding environments.

BASF SE (Ludwigshafen, Germany) – With MasterRoc® and Rheobuild® product families spanning powder and liquid formats, BASF leverages formulation R&D and global supply chains to serve both dry‑mix and wet‑mix requirements.

Mapei S.p.A. (Milano, Italy) – Mapei’s MasterSprayed® range targets wet‑mix European applications and benefits from strong regional project relationships and technical service capabilities.

GCP Applied Technologies Inc. (Cambridge, MA, USA) – Offers a mix of admixtures and accelerators aimed at mining and underground projects, emphasizing compatibility with heavy‑duty applications.

The Euclid Chemical Company (Cleveland, OH, USA), Fosroc International Ltd. (Chennai, India), Chryso S.A. (Courbevoie, France), Denka (Tokyo, Japan), Normet Group Oy (Oulu, Finland), and MC‑Bauchemie (Hamburg, Germany) – Each brings regional strength, specialized chemistries or systems expertise that matter in tender‑specific contexts.

Recent field moves underscore these dynamics: in May 2026 Master Builders Solutions expanded U.S. manufacturing capacity to capture rising underground construction demand, while Chryso showcased performance‑driven concrete solutions at The Precast Show in January 2026—signals that both scale expansion and downstream market engagement are active strategies among leading players.

For manufacturers: Accelerate investment into alkali‑free gel formulations, and prioritize backward integration or long‑term off‑take agreements for volatile sulfate and nitrate feedstocks. Capex decisions made in 2026 that improve localized blending and rapid delivery will compound margin benefits by 2028–2030.

For business development and M&A teams: Look for targets that provide either a differentiated low‑rebound chemistry, regional market access in high‑tunnel growth corridors, or equipment integration capabilities. Consolidation dynamics still reward bolt‑on acquisitions that deepen service offerings to large OEMs and tunneling contractors.

For procurement: Rebalance supplier scorecards to include raw‑material hedging provisions, technical‑service SLAs and formulation change‑management clauses. Single‑sourcing for price is increasingly risky; dual‑sourcing linked to performance KPIs reduces delivery exposure.

For R&D and product teams: Prioritize compatibility certifications with modern wet‑mix spray systems and develop low‑alkalinity variants that reduce environmental compliance costs for clients. Formulation patents and performance warranties are viable levers to shift competition away from price alone.

The PW Consulting report is structured for execution. Key deliverables include:

Global market sizing and a transparent forecast model (2026–2032) with scenario pathways tied to tunneling, mining capex cycles and adoption rates of wet versus dry processes.

Supplier scorecards and a competitive heatmap that assess technical breadth, geographic reach, integration capability and raw‑material exposure.

Raw‑material exposure matrix and margin sensitivity testing—identifying which feedstocks create the biggest P&L swings under different energy‑price scenarios.

Go‑to‑market playbooks for three archetypal entrants: global scale player, regional specialist and systems integrator—each with 12‑ and 36‑month KPIs.

M&A screening framework and valuation multiples calibrated to both chemical specialty norms and construction‑service premiums.

Case studies and procurement clause templates that speed contract negotiation for major tunneling and mining projects.

The study synthesizes primary interviews with procurement leads, technical specialists, suppliers and contractors, triangulated with trade statistics and company disclosures across the 2020–2025 historical window. Forecasting employs a blended approach: demand drivers (tunneling schedules, mining capex, repair cycles), adoption curves for process formats, and supply‑side constraints (feedstock availability, capacity expansions).

PW Consulting intentionally applies the “trailer” principle in the public summary: we reveal the macro market trajectory and the strategic implications you need to act, while retaining detailed subsegment tables, region/application breakdowns and proprietary vendor scoring models within the full report and our interactive data portal. This preserves the utility of our actionable insight while protecting the calibrated segmentation that clients use for bidding, pricing and M&A diligence.

Lock in strategic feedstock hedges or long‑term supply agreements for sulfate/nitrate inputs to mitigate near‑term margin shock.

Pilot alkali‑free gel formulations in two live tunneling contracts to validate performance and secure spec‑level references.

Initiate a capacity gap assessment for quick‑win blending sites within priority markets identified in the full report.

Embed equipment compatibility guarantees into product contracts to capture system premium opportunities with OEMs.

Scan M&A targets using our three‑archetype filter and open one exclusivity discussion for a bolt‑on acquisition that expands technical capability or geographic reach.

PW Consulting’s Shotcrete Accelerator Market report equips leaders with the macro clarity and operational playbooks required to convert a 7.85% CAGR environment into sustainable margin expansion and market share gains. For access to the full data tables, vendor scorecards and the interactive forecast model—essential for executing the 90‑day moves described above—visit our report landing page or contact our sector team to schedule a tailored briefing.

For detailed analysis of this topic, please visit the official page:Shotcrete Accelerator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com