Automotive Wheel Bearing Market 2026: Strategic Imperatives from PW Consulting’s New Industry Report

As original equipment manufacturers (OEMs), tier suppliers, aftermarket distributors, and private-equity investors calibrate portfolios for 2026, the automotive wheel bearing sector presents a focused mix of predictable engineering demand and disruptive technological inflection. PW Consulting’s new market study—anchored on 2025 as the base year with a historical review spanning 2020–2025 and forecasts through 2032—combines granular supplier intelligence, pragmatic scenario analysis, and executable playbooks designed to inform high-stakes capital and product decisions.

Automotive Wheel Bearing Market

Key headline: a stable, mid-single-digit growth market with rising structural complexity

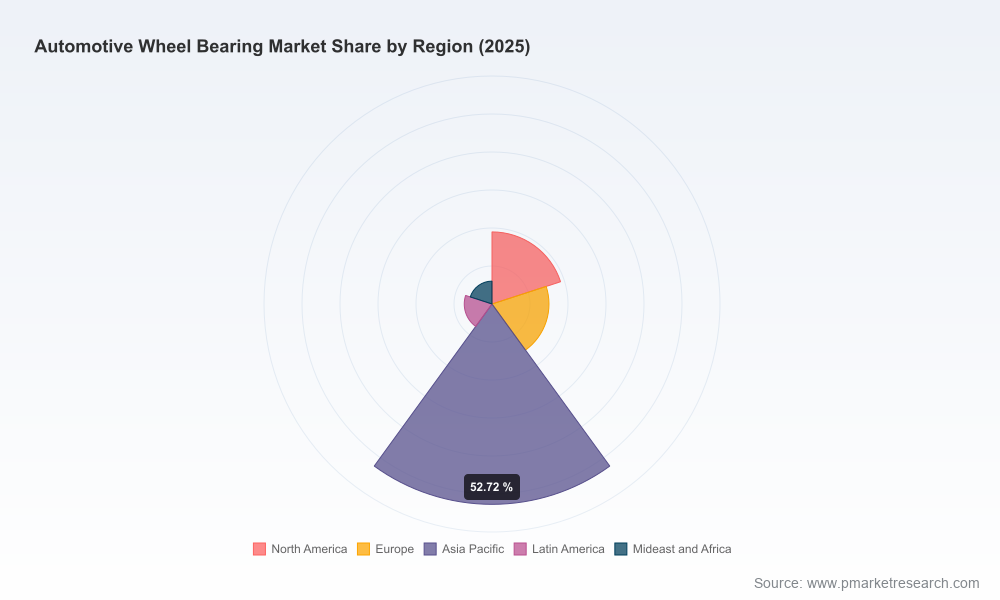

Our analysis shows the global automotive wheel bearing market reached USD 305.0 Million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 6.5% over the 2026–2032 forecast window, arriving at approximately USD 466.0 Million by 2032. This trajectory reflects a blend of steady OEM replacement cycles, accelerating sensor and lubrication innovations, and aftermarket opportunities driven by aging parc and extended service models.

Automotive Wheel Bearing Market

Why this matters to decision-makers in 2026

- Capital allocation clarity: The mid-single-digit CAGR signals an investable, defensible market that rewards targeted R&D and selective capacity expansion rather than broad-brush scale plays. Boards should prefer focused investments—sensor integration, low-drag sealing, and grease lifecycle technologies—over commoditized volume bets.

- Timing M&A and partnerships: Market concentration is meaningful: the upper-tier incumbents capture a majority share of OEM supply and aftermarket channels, enabling acquirers to pursue tuck-ins that enhance systems capabilities (e.g., bearings + sensing + lubrication monitoring) rather than market-share consolidation alone.

- Aftermarket vs OEM strategic choices: With extended vehicle lifecycles and diverse service models, companies that develop repeatable aftermarket programs—analytics-driven remanufacturing, warranties tied to predictive maintenance—stand to compound lifetime revenues beyond one-time OEM sales.

What the report delivers: actionable, practice-oriented intelligence

PW Consulting’s report is built to be operational. It contains the following deliverables designed for executive and commercial teams:

Automotive Wheel Bearing Market

- Market sizing and trend narratives (2020–2025 historicals and 2026–2032 scenarios) that reconcile macro demand drivers with hands-on supply-side constraints.

- Scenario-based forecasting models (base, upside, downside) with adjustable levers for EV penetration, OEM design-cycle shifts, raw-material cost shocks, and regulatory changes—delivered as an editable workbook for internal planning.

- Supplier and OEM ecosystem maps: proven supply routes, single-source dependency hotspots, and near-term capacity inflection points for strategic procurement and supplier development.

- Cost-to-serve and manufacturing cost curves that isolate the real drivers of margin for different product architectures (bearing types, hub-unit integration, pre-lubrication solutions).

- Technology readiness assessments for sensor-integrated bearings, low-torque sealing, and advanced greases—scored for maturity, integration complexity, and likely adoption timelines.

- Regulatory and standards impact briefing: how recent ASTM, SAE, and academic/industrial studies translate into product, testing, and warranty implications (see Dynamics below).

- Competitive playbooks and vendor scorecards: procurement negotiation priorities, product roadmaps to watch, and suggested alliance strategies tailored to OEMs, aftermarket players, and investors.

Market dynamics: the immediate technical and regulatory signals you cannot ignore

The sector’s near-term technical trajectory is being shaped by discrete advances in testing standards, predictive analytics for life assessment, and lubrication/ sealing science. PW Consulting’s report synthesizes these developments and translates them into commercial implications:

- The ASTM D1263 standard for leakage tendencies of wheel bearing greases sharpens product differentiation: manufacturers with demonstrably lower leakage and higher thermal stability will capture endurance-sensitive OEM programs.

- Emerging SAE methodologies for real-time life prediction of bearings reposition life-cycle services: integrators that couple load-data analytics with bearing design can propose extended-warranty offerings and condition-based maintenance contracts.

- Academic and industry work on drag torque modeling and interference optimization is changing the design calculus for sealing systems. Lower drag at the seal interface improves fuel economy and EV range; suppliers who demonstrate validated torque reductions will enter conversations about whole-vehicle efficiency trade-offs.

- Device-level innovations—such as multi-bearing grease repacking equipment—are lowering the total cost of ownership for service networks, enabling aftermarket actors to offer faster turnarounds and higher-margin remanufactured units.

Competitive landscape: synthesis and strategic implications

The market’s supplier map is dominated by established engineering-centric companies with global OEM relationships and deep materials and tribology expertise. Key players profiled in the report include:

- SKF Group (Gothenburg, Sweden) — Producer of hub bearing units and aftermarket solutions, notable for integrated sensors and pre-lubricated assemblies.

- Schaeffler AG (Herzogenaurach, Germany) — Offers a range of branded wheel-bearing systems and comprehensive aftermarket kits focused on repairability and serviceability.

- NSK Ltd. (Tokyo, Japan) — Known for advanced sealing and mounting technologies in hub unit bearings tailored for chassis applications.

- NTN Corporation (Osaka, Japan) — Supplies OEM and aftermarket hub assemblies with a focus on passenger and light commercial vehicle segments.

- JTEKT Corporation (Osaka, Japan) — Produces hub units that emphasize sensor coverage and high-reliability sealing solutions.

- The Timken Company (North Canton, Ohio, USA) — Offers engineered hub units with tested performance for passenger and light-truck applications.

Strategic takeaways from our competitive analysis:

- Incumbents are investing along three vectors: sensor/telemetry integration, advanced sealing/low-drag designs, and aftermarket services. New entrants should either specialize in one vector or partner with incumbents to avoid competing on mature manufacturing capability alone.

- Consolidation remains a realistic play for private-equity groups seeking scale in distribution and aftermarket reach rather than pure manufacturing capacity. The industry’s top tier accounts for a clear majority of OEM business, but aftermarket fragmentation creates pockets ripe for platform roll-ups.

- OEMs are increasingly evaluating suppliers on systems-level contributions—bearing performance now sits alongside sensing and predictive maintenance as a procurement criterion.

Practical strategic recommendations for 2026

Executives reading this in 2026 should consider the following priority actions, each grounded in the report’s quantitative and qualitative analysis:

- Prioritize product roadmaps for sensor-enabled units: Commit milestone funding to bearing assemblies that support embedded condition monitoring. The runway for OEM specification cycles is converging with increasing interest in predictive maintenance programs from fleet operators.

- Target margins through lubrication and sealing innovations: Invest in partnerships or licensing arrangements for advanced grease chemistries and low-drag seal geometries that reduce warranty exposure and improve vehicle efficiency—a lever especially relevant to EV OEMs.

- Optimize aftermarket go-to-market: Build remanufacturing centers near high-density service regions, and couple physical capacity with analytics-driven predictive replacement offerings to increase retention and ARPU.

- De-risk supply chains: Map single-source dependencies for critical steels and sealing polymers; qualify dual-source suppliers and hold strategic safety-stock for components sensitive to raw-material volatility.

- Use M&A defensively and offensively: Pursue acquisitions that fill capability gaps—sensor firms, testing labs, or regional aftermarket distributors—rather than chasing volume alone.

- Prepare for regulatory and standards shifts: Align R&D testing to ASTM/SAE advances described above to shorten OEM qualification timelines and reduce late-stage rework costs.

What we intentionally withhold—and why

In keeping with PW Consulting’s “trailer” principle, this communication is designed to establish confidence in our methodology and highlight strategic choices available to leadership teams in 2026. To preserve the report’s commercial value for clients and to avoid substituting for the full analytic asset, we have intentionally withheld detailed regional and application-level split tables, and the granular company market shares found in the full study. The complete report contains interactive regional and application breakdowns, supplier-level share models, and downloadable financial templates that your team can use immediately for budgeting and negotiation.

Next steps: how to convert insight into action

Clients seeking to operationalize these findings can commission one of three PW Consulting deliverables tailored for 2026 planning cycles:

- A two-week diagnostic including supplier due-diligence and a prioritized capex roadmap for product and service investments.

- A six-week go-to-market and aftermarket optimization program, delivering contract templates, pricing playbooks, and a near-term pilot plan for predictive maintenance services.

- A full acquisition or JV target assessment using our confidential competitor financial model and integration playbook.

For strategic teams preparing budgets and roadmaps for 2026, PW Consulting’s Automotive Wheel Bearing Market report provides the actionable mix of quantitative forecasting, supplier intelligence, and implementation-ready recommendations needed to make confident capital and commercial decisions. To access the full dataset, company profiles, and the editable forecast model, please visit our report page and download the executive summary.

For detailed analysis of this topic, please visit the official page:Automotive Wheel Bearing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com