Polymer Gas Separation Membrane Market: Strategic Imperatives for 2026 — PW Consulting Report Preview

Executive summary

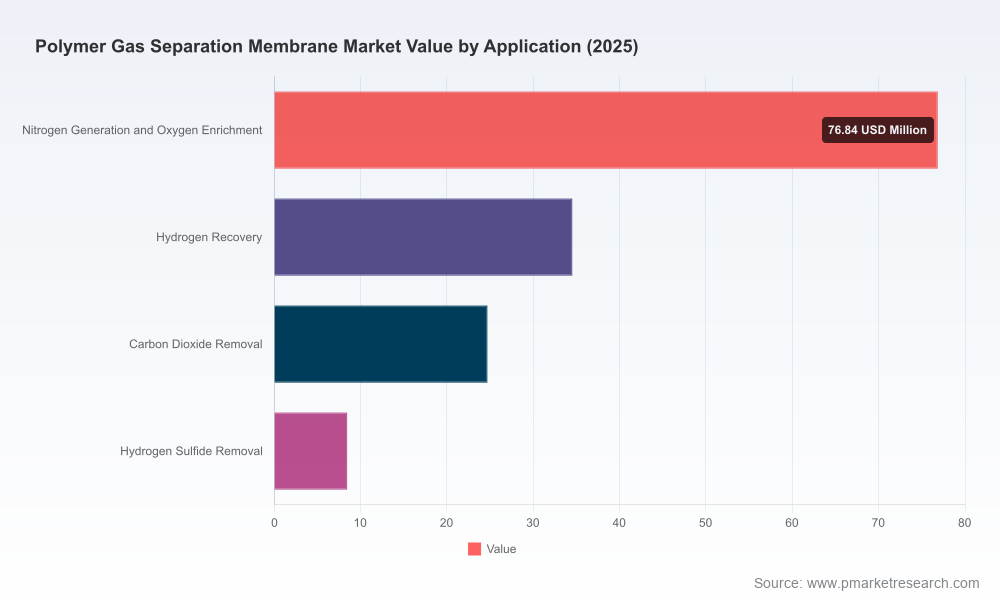

PW Consulting’s latest market study on Polymer Gas Separation Membranes synthesizes five years of historical performance (2020–2025) and presents a forward view across the 2026–2032 forecast horizon. The global market has expanded from a modest base in 2020 to an estimated USD 144.5 Million in the report’s base year (2025), and is projected to follow a compound annual growth rate (CAGR) of 6.3% through 2032, reaching roughly USD 220 Million by the end of the forecast period. This trajectory underscores a sustained commercialisation phase for polymer membranes driven by decarbonization programs, the evolving hydrogen economy, and persistent demand in industrial gas processes.

Polymer Gas Separation Membrane Market

Why this briefing matters for 2026 decision-making

- Timing: The market’s mid-single-digit CAGR indicates that strategic moves made in 2026 will play out across an expanding but competitive landscape — 2026 is not a distant opportunity window but an inflection point for capability building and resource allocation.

- Investment signal: The size and growth profile justify medium-to-long-term investments in manufacturing scale, R&D for high-performance polymers, and commercial teams focused on fast-growing end-markets such as hydrogen recovery and carbon management.

- Risk management: Momentum in demand is counterbalanced by input-cost volatility and policy uncertainty, making 2026 the year to harden procurement strategies and to pilot alternative sourcing and recycling pathways.

Market dynamics shaping corporate strategy in 2026

PW Consulting’s report identifies a set of converging forces that will determine winners and laggards in the polymer membrane domain:

Polymer Gas Separation Membrane Market

- Demand drivers: Accelerating deployment of carbon capture, new-build and retrofit hydrogen value chains, and ongoing demand for industrial nitrogen/oxygen generation are the principal pull factors. These applications are expanding the addressable market beyond traditional separations.

- Technology evolution: Advances in polyimide and other polymer chemistries, hollow-fiber architectures, and module integration are improving selectivity and throughput while tightening the gap with alternative separation technologies. R&D trajectories favour materials and process improvements that lower levelized cost of separation.

- Supply-chain sensitivity: Upstream chemical feedstocks (notably ethylene derivatives) and energy inputs are material to production economics. For example, North American ethylene price points observed in mid-2026 and ongoing natural gas price volatility materially affect operating cost assumptions for manufacturers and end-users.

- Policy and trade: Tariff actions on inputs and components can increase landed costs for membranemakers that rely on cross-border supply chains. Simultaneously, stringent environmental frameworks—particularly in Europe—are creating preferential demand for low-carbon separation solutions.

Competitive landscape — concentration, capability and strategic plays

The polymer gas separation market is moderately concentrated at the top: the three-largest players account for close to half of the market, and the five-largest approach just above the halfway mark. This concentration level produces a dual-structure dynamic: established suppliers possess strong channel, IP and quality credentials while a deep tail of specialised players competes on niche performance or service models.

Polymer Gas Separation Membrane Market

Key corporate archetypes and strategic postures identified in the report:

- Global industrial gas incumbents (e.g., established air separation and gas suppliers) leverage existing customer bases and systems integration capability to bundle membranes with broader gas-supply solutions. Their strength lies in project origination, long-term service agreements, and capital anchoring for large installations.

- Specialist membrane manufacturers with material-chemistry IP lead on product performance and cost-per-separation metrics. These firms typically compete through continuous process innovation, proprietary hollow-fiber designs, and targeted capex to increase capacity.

- Integrated engineering suppliers combine membrane modules with process engineering to serve complex gas-processing and upstream applications. Their differentiation is systems-level modelling and field-proven delivery in demanding environments.

Representative companies profiled in the report (summary only): Air Liquide Advanced Separations, Air Products and Chemicals, Evonik Industries, Honeywell UOP, UBE Corporation, Membrane Technology and Research (MTR), GENERON, Parker Hannifin, FUJIFILM Advanced Separations, SLB (Schlumberger), AirRane, DIC Corporation and Grasys. Each profile maps capability (materials, module formats), commercial reach, recent investments and a risk assessment for 2026 decision-makers.

Recent strategic moves to watch (selected)

- Partnerships and alliances: A late-2025 collaboration announced by a major industrial gas player signals intensified industry interest in coupling renewable energy and membrane technologies for carbon capture solutions.

- New product introductions: Announcements in 2025 of membranes tailored to hydrogen separation show vendors moving to capture high-margin, high-growth applications.

- Capacity and manufacturing: Investment in North American manufacturing capacity and greenfield plant commitments in 2025 reflect supplier responses to regional demand growth and supply security considerations.

Practical contents of the PW Consulting report (what you will actually use)

The report is structured to be decision-ready for 2026 corporate planning cycles. Key deliverables include:

- Top-down and bottom-up market models (2020–2032) with sensitivity scenarios that isolate demand by major application groups, polymer family performance, and regional rollout timing.

- Cost curves and benchmarking tools to evaluate supplier economics under varying input-price scenarios (including ethylene and natural gas exposure), allowing procurement and finance teams to stress-test capital projects.

- Supplier maps and capability matrices that identify manufacturing nodes, proprietary technologies, and service footprints—designed to inform sourcing and make-or-buy decisions.

- Technology readiness and commercialization roadmaps that rank polymer chemistries and module formats by maturity and scale-up risk, tied to practical pilot-to-commercial pathways.

- A playbook for partnerships, licensing and M&A including valuation heuristics, integration risk checklists, and sample term structures for off-take agreements and technology licensing.

Note: In keeping with the report’s role as a comprehensive market intelligence product, detailed sub-segment tables and granular regional/application shares are reserved for the full report and accompanying data workbook. This preview is intentionally high-level to guide strategic thinking while directing technical teams to the full dataset for transactional decisions.

Strategic recommendations for 2026

For corporate leaders allocating capital, negotiating supply agreements, or refining R&D priorities in 2026, PW Consulting advises a pragmatic, staged approach:

- Secure supply and hedge input exposure: Lock in feedstock and component contracts where feasible; evaluate localized supply or backward integration where tariffs and logistics materially affect costs.

- Prioritize pilot-to-scale projects with clear economic thresholds: Use targeted pilots to derisk scale-up for hydrogen and carbon-focused applications; require milestones that trigger incremental capital.

- Partner for speed and capability: Joint development and co-investment with technology specialists can accelerate time-to-market while spreading technical risk, particularly for advanced polymer formulations and module integration.

- Differentiate beyond materials: Compete on systems integration, lifecycle service, and data-driven performance guarantees to extract premium value over commoditized membrane modules.

- Use scenario-based capital planning: Build financial models that incorporate raw-material price swings and potential tariff scenarios to ensure resilience of investment cases.

Implications for M&A, procurement and R&D

The market’s moderate concentration and the acceleration of strategic activity mean that acquisitive moves in 2026 should be highly selective. Targets should offer one or more of: proprietary materials with demonstrable scale-up pathways, manufacturing or regional footholds that de-risk supply, or complementary systems-integration capabilities.

Procurement teams should move from transactional sourcing toward strategic supplier partnerships that align incentives across volume growth, quality yields and co-development milestones. R&D investments should be balanced between near-term performance gains (selectivity and flux improvements) and mid-term material breakthroughs that reduce long-run total cost of separation.

How to get the full intelligence

This preview is designed to inform executive-level strategy for 2026 while directing technical, commercial and M&A teams to the full PW Consulting dataset and analytical models. The complete report includes the downloadable data workbook, supplier scorecards, scenario model templates and a deal-structuring annex that are essential for operationalizing the recommendations summarized here.

To obtain the full Polymer Gas Separation Membrane Market report and the associated tools that support 2026 decision-making, please visit PW Consulting’s report page or contact our industry research desk for a guided briefing and a demo of the interactive models.

For detailed analysis of this topic, please visit the official page:Polymer Gas Separation Membrane Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com