Display Market Potential Strengthens with Immersive Retail and Virtual Experience Solutions

Other |

2026-05-07 06:09:58

As companies prepare strategic plans for 2026 and beyond, the Xylooligosaccharides (XOS) market is transitioning from niche innovation to scalable commercial opportunity. PW Consulting’s latest market study — anchored on a 2025 base year and projecting through 2032 — synthesizes market-size trajectories, competitive dynamics, regulatory contours, and practical playbooks that executives, corporate development teams, and investors can apply immediately. This briefing highlights the report’s strategic value while preserving the high-resolution data that drives tactical choices; the detailed segment-level and price-elasticity models are reserved for the full report.

Xylooligosaccharides (XOS) Market

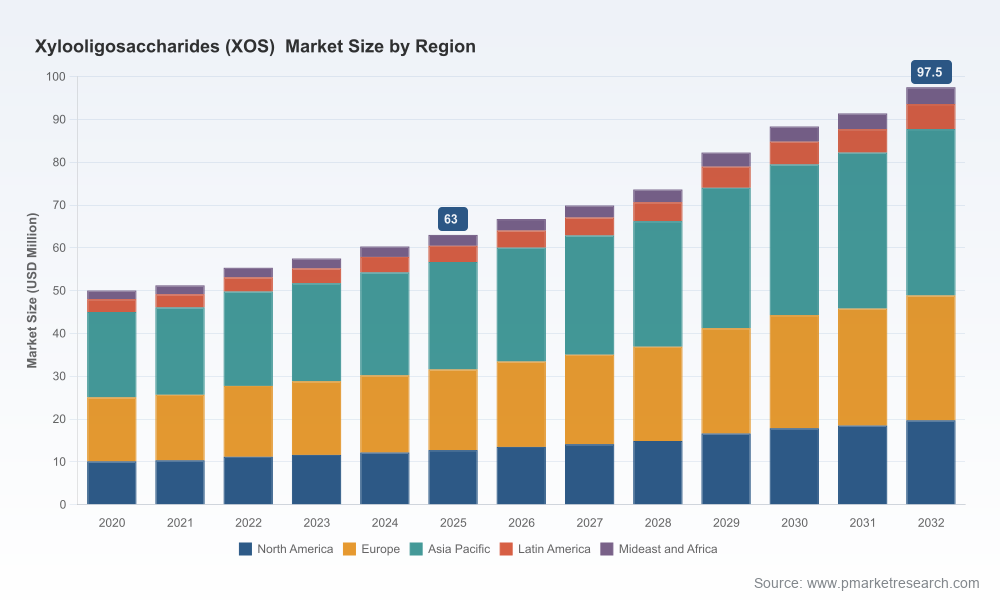

Our macro analysis shows the industry moving from an early-adopter base to a broader commercial cadence. From an observed market of approximately USD 50.0 Million in 2020, XOS demand has expanded steadily through 2025 (USD 63.0 Million), and our forecast models indicate continued growth across 2026–2032. Under a base-case trajectory, the market grows to an estimated USD 66.7 Million in 2026 and reaches roughly USD 97.5 Million by 2032, reflecting a compound annual growth rate (CAGR) of 6.5% over the forecast period.

Xylooligosaccharides (XOS) Market

These macro dynamics reflect three durable drivers: (1) widening industrial adoption across food & beverages, animal nutrition and nutraceuticals; (2) industrialization of feedstock-to-product value chains where low-cost agricultural residues enable cost-competitive production; and (3) regulatory clarity in key jurisdictions that reduces commercial friction for established use cases.

Xylooligosaccharides (XOS) Market

PW Consulting organizes the XOS opportunity around pragmatic decision levers. Highlights of the deliverables include:

Feedstock economics are foundational. Corn cobs — widely available as a low-cost agricultural by-product with high xylan content — remain the primary upstream feedstock. This positions regions with robust corn production to serve as low-cost manufacturing hubs, but it also ties producers’ input costs to seasonal harvest cycles and local commodity-price dynamics. Our cost-sensitivity scenarios show that feedstock availability and logistics can be the difference between a competitively priced product and a margin-constrained offering.

Regulation shapes commercial runway. Regulatory regimes differ materially: in the United States, XOS enjoys GRAS recognition for defined uses, which facilitates faster route-to-market for ingredient suppliers and their food customers. In Canada, non-novel determinations for certain feedstock-derived XOS remove procedural uncertainty. By contrast, the European Union treats XOS as a novel food under Regulation (EU) 2015/2283, requiring pre-market authorization and a longer lead time for widespread penetration. This regulatory patchwork creates both barriers and arbitrage opportunities: producers with substantiated safety dossiers can prioritize markets with lower friction while preparing dossiers for high-value but slower EU entry.

Concentration and competition. The market exhibits moderate concentration, with the top three firms accounting for a significant share of capacity and the top five controlling a broader portion of available supply. This structure creates a hybrid competitive environment: scale matters for raw-material procurement and route-to-market, but product differentiation — purity grades, liquid vs. powder formats, and beverage-compatible formulations — offers a defensible route to margin enhancement for smaller, agile players.

Our vendor ecosystem analysis combines public disclosures, industry interactions and capacity verification. Key themes include: rapid capacity additions among several Chinese producers, Asian incumbency in manufacturing know-how, and pockets of western innovation focused on specialty applications and branded formulations.

For commercial counterparties, the practical implication is clear: scale players will continue to exert pricing pressure on commodity-grade XOS, while innovation in purity, formulation and application-specific delivery will command premium positioning. Strategic buyers should balance short-term cost objectives with longer-term access to differentiated grades and co-development pathways.

Executives and investors approaching XOS-related decisions in 2026 should focus on three interlocking priorities:

Our deal framework encourages a pragmatic combination of minority investments, offtake agreements and co-development partnerships rather than binary M&A strategies, especially for new entrants. Recommended actions for corporate development teams include:

The XOS market in 2026 is marked by continued expansion, selective consolidation and product-form innovation. Our forecast — reflecting historical development from 2020 to 2025 and projecting through 2032 — quantifies this pathway and translates it into actionable scenarios that companies can use to stress-test investments, prioritize R&D allocations, and design supply-chain hedges.

PW Consulting’s report is designed as a decision tool, not a reference appendix. Subscribers will receive the underlying spreadsheets supporting our market-size trajectories, supplier cost curves, and a prioritized M&A/partnership shortlist based on quantitative scoring. The public briefing above is intentionally tactical but high-level: we demonstrate the analytical backbone while reserving the granular segment-level splits and price schedules for clients who require transaction-grade intelligence.

PW Consulting’s XOS report consolidates the quantitative foresight and qualitative market intelligence needed to act decisively in 2026. To access the full dataset, segmentation tables, and the executable playbooks referenced above, please visit our report page for subscription details and client engagement options.

For detailed analysis of this topic, please visit the official page:Xylooligosaccharides (XOS) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com