Slitter Market 2026 Strategic Briefing — A PW Consulting Insight

As global manufacturing confronts tighter tolerances, stretched supply chains and fast-evolving end-market demands, the slitter market has moved from a niche capital-equipment conversation to a strategic lever for industrial competitiveness. PW Consulting’s latest Slitter Market report (base year 2025; historical review 2020–2025; forecast period 2026–2032) synthesizes market-scale modeling, technology roadmapping and practical decision frameworks tailored for senior executives planning 2026 capital allocation, supply-chain reconfiguration and M&A activity.

Slitter Market

Key takeaways for 2026 decision-makers

- Market momentum: The slitter market has shown steady historical expansion and is forecast to grow at a 6.2% CAGR through 2032. Our modeling places the global market at USD 215.0 Million in 2025, rising to USD 234.68 Million in 2026 and tracking to approximately USD 344.8 Million by 2032—illustrating a resilient mid-single-digit expansion driven by electronics, advanced packaging and packaging-sector automation.

- Fragmented supplier base: Market concentration remains low, with top-three and top-five firm shares indicating an industry still open to product and commercial consolidation—an attractive dynamic for strategic investors andOEMs seeking scale.

- Near-term risk factors: Component lead-times and raw-material volatility are acute. Precision optics and specialty gases exhibit extended lead-times beyond six months, and commodity pressures (notably copper) materially amplify input-cost risk.

- Regulatory and tariff inflection points: Machinery-safety regulations and tariff classifications for high-precision slitters are already shaping go-to-market choices for exporters and importers; compliance timelines are now a procurement and product-engineering constraint.

Why 2026 is an inflection year

Three converging forces make 2026 a make-or-break planning year for slitter equipment strategies:

Slitter Market

- Technology adoption in adjacent industries. Semiconductor packaging trends—such as panel-level packaging and larger glass panel processing—are expanding the technical demands placed on slitter designs. Recent product launches from strategic equipment suppliers underscore a pivot toward machines that support large-format substrates, micron-level tolerances and tighter inline metrology.

- Supply-chain realism. Several upstream bottlenecks have hardened into structural risks: precision optics and specialty gas shortages have pushed lead-times beyond six months, and copper pricing volatility has elevated the cost base for slitting consumables and components. Procurement teams must plan for longer order lead-times and contingency sourcing.

- Regulatory and tariff headwinds. For companies operating in or exporting to the EU, compliance with European machinery safety law remains mandatory and has concrete implementation timelines that must be factored into product roadmaps and certification pipelines. Additionally, certain high-precision slitters targeted at thin copper strips are now explicitly captured under specific tariff codes—an operational detail with implications for landed cost and sourcing strategies.

Market outlook — numbers that matter

PW Consulting’s topline modeling shows steady expansion from the historical baseline: the market rose from roughly USD 163.15 Million in 2020 to USD 215.0 Million in 2025, reflecting a compound response to rising packaging automation and electronics manufacturing demands. Under a central-case scenario, the market grows at a 6.2% CAGR through 2032, with modeled figures landing near USD 234.68 Million in 2026 and approaching USD 344.8 Million by 2032.

Slitter Market

Interpretation for strategy: these are not merely volume signals. They reflect upgraded buyer requirements—precision, automation, inline inspection and compatibility with semiconductor and advanced-packaging workflows—that favor suppliers who can demonstrate integrated solutions and predictable lifecycle economics.

Competitive landscape — who matters and why

The slitter ecosystem today is characterized by a mix of specialized manufacturers and larger capital-equipment players who integrate slitting capabilities into broader semiconductor or materials-processing product suites. Key firms we profile in detail include:

- Applied Materials, Inc. (Santa Clara, USA) — recognized for precision wafer dicing and cutting equipment that intersects with slitting needs for films and substrates in semiconductor workflows.

- Tokyo Electron Limited (Tokyo, Japan) — a major semiconductor-equipment player whose offerings include dicing machines and materials-handling platforms relevant to high-throughput slitting and slicing.

- KLA Corporation (San Jose, USA) — a leader in inspection and metrology that increasingly integrates inline quality assurance into slitting and dicing processes.

- Toray Engineering (Tokyo, Japan) — focused on film slitting solutions and active in panel-level packaging, with recent product launches emphasizing compatibility with larger glass panels and PLP workflows.

- ACRETECH Co., Ltd. (Tokyo, Japan) — a specialist in precision dicing machines for wafer slitting and related electronics-manufacturing operations.

Collectively, the competitive footprint signals an industry where product differentiation is shifting from basic mechanical throughput to integrated system performance—metrology, automation, material handling and after-sales service. The low aggregate concentration (top-three/top-five metrics indicate notable fragmentation) creates opportunities for both organic scale-up and acquisitive consolidation.

Recent industry signals to watch

- Product launches targeting panel-level packaging and large-panel compatibility are explicit indicators that semiconductor-packaging demand will be a key pull through 2026–2028.

- Extended supplier lead-times for critical components mean that procurement cycles must be moved forward, and buffer strategies for spares and consumables are now cost-of-doing-business decisions.

- Tariff and classification updates affecting high-precision slitters used for thin copper strips have immediate P&L implications for cross-border supply chains; companies should re-evaluate landed-cost models in light of updated HTS assignments.

- Elevated copper prices and other commodity shocks will compress margins for vendors that cannot pass through costs or hedge exposure effectively.

What the PW Consulting report delivers — an actionable toolkit

The full report blends market intelligence with practitioner tools designed for decision-makers. Highlights include:

- Five-year and long-run revenue models (2026–2032) with scenario toggles for demand shock, tariff shock and technology-adoption acceleration.

- Capital allocation frameworks: step-by-step ROI and payback calculators adjusted for automation intensity, uptime improvement and scrap reduction.

- Vendor due-diligence playbook: technical checklists, supplier audit templates, software/integration assessment and service-level benchmarking.

- Regulatory compliance roadmap: checklist and timeline for EU machinery directives and relevant tariff-code implications—mapped to product-design and certification milestones.

- Supply-chain stress tests and multi-sourcing strategies: quantitative templates to size inventory buffers, evaluate dual-sourcing trade-offs and optimize lead-time hedges.

- Go-to-market playbooks for OEMs and systems integrators, including white-space identification, bundling strategies and channel-partner scorecards.

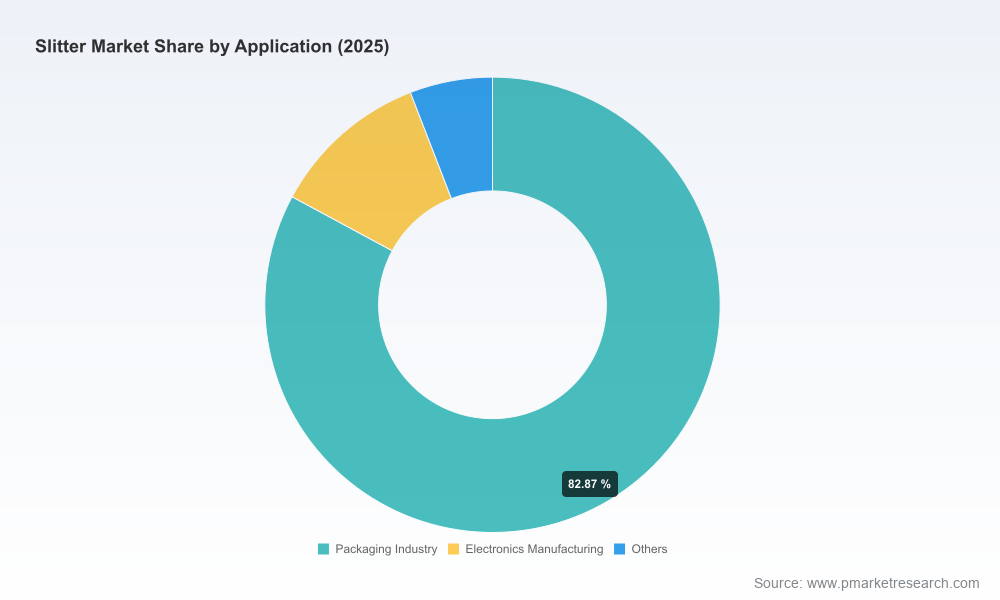

Note: granular regional shares, application-level splits and supplier-level pricing tables are intentionally reserved for the full report. These detailed breakouts are essential for operational implementation and are available via the PW Consulting distribution channel.

Strategic recommendations for 2026

- Reprioritize CapEx toward precision and automation. Purchase decisions should favor systems that reduce manual touchpoints, integrate inline inspection and offer modular upgrade paths—protecting against rapid specification shifts in semiconductor and packaging customers.

- Lock in lead-times and spares contracts now. Given component lead-times that can exceed six months, procurement teams should negotiate longer-term agreements, strategic consignment of critical spares and collaborative lead-time visibility with key suppliers.

- Hedge commodity exposure. Copper price volatility is a real cost-driver. Hedging strategies, index-linked supplier contracts and substitution roadmaps (where feasible) should be part of procurement playbooks.

- Embed regulatory compliance into product roadmaps. Ensure machinery-safety certifications and tariff-classification checks are completed early in design cycles to avoid delayed market access—especially for EU trade lanes and high-precision copper-slit products.

- Evaluate partnerships with semiconductor-equipment firms. The fastest route to market for advanced slitter capabilities is often co-development or technology partnerships with established semiconductor-equipment vendors who can provide commercialization channels.

- Pursue targeted consolidation. For investors and larger OEMs, the fragmented market signals opportunities for bolt-on acquisitions to secure IP, aftermarket revenue and geographic reach.

How PW Consulting supports your 2026 planning

Our engagement model is designed for rapid, executable impact: from an executive briefing that translates our market model into a board-level decision memo, to a hands-on procurement deep-dive and a technical due-diligence package for M&A teams. For clients preparing for 2026 procurement cycles, we provide immediate-access scenario models and a regulatory-compliance checklist aligned to the most pressing timelines.

For operational teams and strategists who require the full regional and application-level intelligence—alongside supplier pricing, product roadmaps and step-by-step implementation templates—PW Consulting’s complete Slitter Market report is available through our client portal. The public briefing above is a curated preview intended to enable informed conversations; the full dataset and executable playbooks remain gated to support confidential, implementable strategies.

For detailed analysis of this topic, please visit the official page:Slitter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com