Revealed: Metal Cutting Machine Tools Demand Surges

Other |

2026-04-22 10:27:28

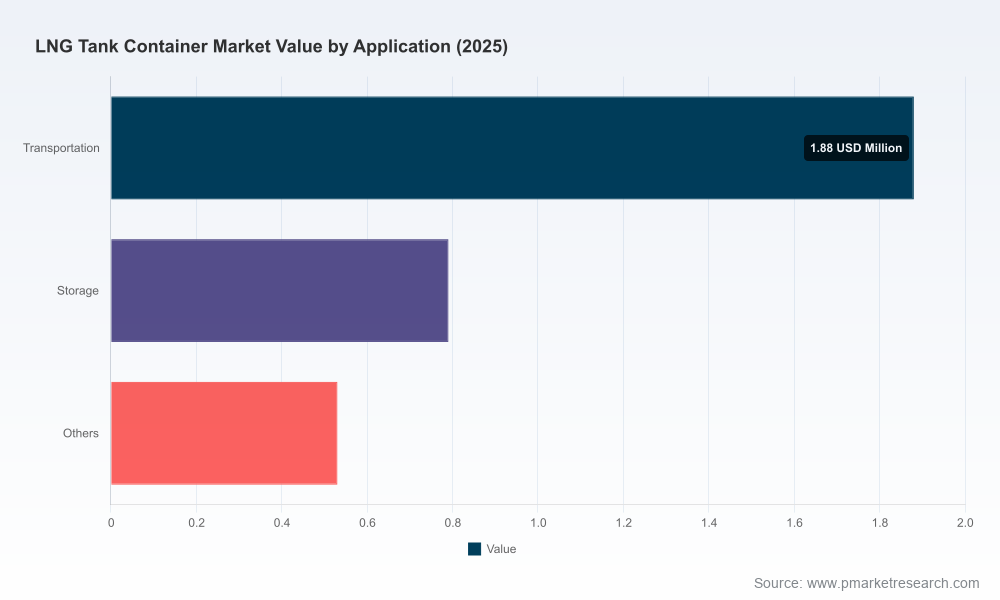

PW Consulting today issues a strategic preview of our forthcoming LNG Tank Container Market report, designed as an operational playbook for executive teams making decisions in 2026. Built on a 2025 base year and a 2020–2025 historical dataset, our model projects the market forward through 2032. The global market—measured in revenue terms—has expanded steadily from an earlier base and reached approximately 3.2 Million USD in 2025. Under a set of conservative-to-realistic scenarios, our central forecast points to a compound annual growth rate of 7.5% over 2026–2032, culminating in a projected market size of roughly 5.31 Million USD by 2032.

LNG Tank Container Market

Timing and capacity planning: With a clear multi-year growth trajectory and predictable momentum, procurement teams can avoid the twin risks of overspending on idle assets or losing market share because of delayed capacity additions. Our preview outlines the key lead times and points of inflection that will matter for ordering cycles in 2026.

LNG Tank Container Market

Commercial structuring: As operators weigh leasing vs. owning, the market’s structural characteristics—including a moderately concentrated supplier base—signal differing bargaining dynamics across procurement channels. The report translates concentration metrics into practical negotiation levers for both lessees and lessors.

LNG Tank Container Market

Regulatory and certification readiness: New contract wins increasingly hinge on compliance with multimodal and class society standards. Our analysis maps regulatory thresholds that buyers and OEMs must clear to operate across multiple geographies.

Technology and margin preservation: Insulation techniques, materials selection and manufacturing labour skills materially influence unit economics. The preview synthesizes where technical differentiation creates defensible margins and where standardization compresses them.

Proprietary market sizing & forecast model (2020–2032) with scenario outputs tailored for CAPEX planning, fleet optimization, and M&A screening.

Demand-driver taxonomy and near-term catalysts — including cold-chain expansion, virtual pipeline projects, LNG-to-power deployments and new maritime/regulatory drivers — with quantified sensitivity for each lever.

Supply-side diagnostics covering manufacturing footprints, capacity bottlenecks, raw material exposure, labour skill nodes and quality assurance regimes that affect lead times and warranty risk.

Practical procurement templates: RFP checklists, vendor scorecards, total cost of ownership (TCO) modelling worksheets, and lease-versus-buy calculators tailored to LNG tank container attributes.

Competitive benchmarking and investment due diligence kits for target screening — including capability maps, certification comparators and manufacturing-readiness assessments that investors and strategists can deploy immediately.

Risk matrices and contingency playbooks addressing material-price swings, certification delays, and workforce constraints, with prescriptive mitigation tactics for operations and procurement teams.

The market exhibits a concentrated leadership layer with meaningful room for differentiated players. Our concentration analysis indicates that the top three suppliers capture a majority share of market power, while the top five extend that dominance further — a dynamic that will continue to shape bargaining power, price dynamics and service availability in 2026.

Key corporate profiles we examine in depth include manufacturers, regional representatives and leasing specialists. Highlights of their strategic positioning include:

CIMC Enric Holdings Limited (Shenzhen, China): A full-range OEM producing ISO-format LNG tank containers across multiple lengths with certifications to international standards. Their integrated manufacturing and global compliance posture make them a reference design and delivery partner for large-scale deployments.

Zhangjiagang Furui Group Co., Ltd. (Zhangjiagang, China): Focused on cryogenic ISO tanks with high-vacuum multilayer insulation and a portfolio designed for multimodal transport of LNG and other cryogens. Recent cross-border deliveries underscore their ability to serve international supply chain projects.

TransWorld Equipment (United States): Operating as a regional representative and engineering partner for major global manufacturers, they bridge OEM capacity with North/South American demand, supporting larger-format containers for high-throughput programs.

Chart Industries, Inc. (United States): An established cryogenic systems supplier offering ISO intermodal containers and transportable storage that meet T-class performance and durability benchmarks. Their product exhibits a close fit for virtual pipeline and off-grid distribution use cases.

Srisen Energy Technology Co., Ltd. (China): A niche manufacturer offering both vertical and horizontal tank types, with flexibility across smaller and mid-size capacity ranges—an option for site-specific storage and last-mile logistics.

MCM Management, Control & Maintenance SA (Switzerland): A leasing and fleet-management specialist expanding its ISO-Tank fleet with new designs focused on operational versatility. Their product launches signal the growing importance of flexible fleet ownership models.

Recent industry developments reinforce the market’s dynamism: manufacturers continue transcontinental deliveries to support new LNG supply chains, leasing firms are launching higher-spec containers with baffle and capacity innovations, and exhibitors are showcasing solutions intended for virtual pipeline and off-grid distribution. These events collectively accelerate adoption pathways while raising performance expectations for new assets.

Materials and fabrication: Inner vessels are predominantly fabricated from established carbon and stainless steel grades, while frames use structural steels suited to multimodal handling. Material selection influences thermal performance, manufacturability and life-cycle costs; procurement strategies must account for steel market volatility and lead times for cryogenic-qualified alloys.

Standards and certification: Compliance with ISO 1496 variants, IMDG/ADR/RID, ASME and class society certifications (LR, BV, DNV, CCS, etc.) is non-negotiable for cross-border operations. Certification timelines and test requirements should be built into contracting schedules to avoid deployment delays.

Labour and technical skills: High-vacuum insulation and cryogenic assembly require specialised welding and test competencies. Where in-house capabilities are weak, companies should plan for partner-based manufacturing or targeted training programs to reduce rework and warranty exposure.

Usage evolution: Transportation and short-term storage remain core applications, but emerging use-cases—such as temporary power projects, industrial feedstock deliveries, and remote LNG-to-power deployments—are reshaping demand profiles and unit design priorities.

Align procurement cadence with forecasted demand inflection points. Use our model to map order placement to production lead times and certification windows to minimize cash drag and ensure availability where growth accelerates.

Adopt a modular supplier strategy: combine large OEMs for scale with niche suppliers for specialized configurations. This reduces single-vendor dependency while preserving access to differentiated technologies.

Run a lease-versus-buy analysis that factors lifecycle operating costs, depot maintenance capabilities and utilization assumptions. For many players, leasing from fleet-specialists can accelerate go-to-market while deferring capital intensity.

Prioritize certification and quality assurance early in supplier selection. Include class-society gate reviews in contract milestones and tie payments to demonstrated compliance to protect against late-stage redesigns.

Invest in workforce readiness where vertical integration is strategic. Training in cryogenic welding and vacuum-insulation assembly reduces defects, shortens ramp-up and preserves warranty margins.

Use scenario-based TCO modelling to stress-test investments under commodity, regulatory and utilization shocks. Our report’s downloadable models make it straightforward to adapt assumptions for internal approval processes.

This preview aims to equip senior leaders with the strategic context and immediate actions required for 2026. It demonstrates the type of granular, operational intelligence PW Consulting delivers while intentionally withholding the full segment-level breakdowns, vendor scorecards, and transaction-ready models that are included in the complete report. Those datasets—covering granular regional/application splits, unit economics by format and detailed competitive scorecards—are essential for transaction execution and procurement negotiations and are available exclusively with the full report.

To access the complete LNG Tank Container Market report, including all appendices, modelling files and procurement templates, please visit the PW Consulting research center. For enterprise licensing, custom scenario runs, or to commission a bespoke supplier due diligence package, contact our Advisory Desk to secure prioritized support in 2026.

For detailed analysis of this topic, please visit the official page:LNG Tank Container Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com