Wear Plate Market 2026 Strategic Outlook: Executive Briefing for Decision‑Makers

PW Consulting’s latest Wear Plate Market report synthesizes five years of historical performance (2020–2025) and an actionable seven‑year forecast (2026–2032) to equip senior executives with the commercial intelligence needed to make high‑stakes decisions in 2026. The study combines market sizing, supplier benchmarking, technology validation and regulatory scenario planning into a single, operationally focused deliverable designed for procurement chiefs, plant managers, business development leads and corporate strategy teams.

Wear Plate Market

Why this report matters for 2026 decisions

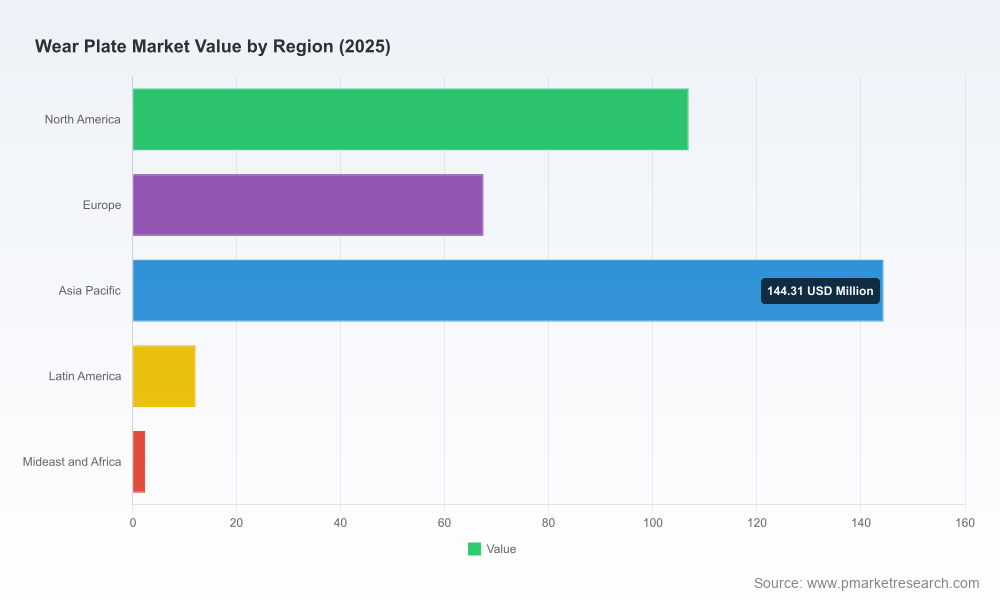

After tracking the market from a base of USD 252.0 Million in 2020 to USD 333.0 Million in 2025 (base year), PW Consulting models the wear plate market to grow at a compound annual growth rate (CAGR) of 6.7% during the 2026–2032 forecast period, reaching an estimated USD 519.0 Million by 2032. These macro dynamics indicate a market expanding faster than many traditional steel‑consumable categories and create a narrow window in 2026 for firms to reposition around product innovation, supply‑chain resilience and lifecycle economics.

Wear Plate Market

Our research is designed as a practical playbook rather than a purely academic study. It translates top‑line growth into prioritized actions that materially affect OPEX, CAPEX and competitive positioning over the next three to five years.

Wear Plate Market

Key takeaways executives must consider in 2026

- Growth is structural, not cyclical: The market’s trajectory through 2025 and the modeled 6.7% CAGR to 2032 reflect more than temporary demand spikes — they signal persistent replacement cycles, broader adoption of engineered overlays, and rising requirements for abrasion and impact resistance across heavy industries.

- Consolidation remains limited: Market concentration is low‑to‑moderate (CR3 and CR5 measures indicate a fragmented supplier landscape). This fragmentation creates opportunities for both scale plays and niche specialists to win differentiated margins through technical superiority or service excellence.

- Lifecycle economics trump first‑cost in buyer decisions: Procurement strategies that emphasize total cost of ownership, scheduled exchange windows and on‑site hardfacing capability capture more value than those anchored to unit price alone.

- Regulation and carbon pricing will reconfigure sourcing: The EU Carbon Border Adjustment Mechanism (CBAM), effective from 2026, changes the calculus for imported plates and overlay materials and will force supply‑chain redesigns for companies exposed to EU markets.

What the report contains — a practical summary

PW Consulting’s report is structured to move teams from insight to implementation. The core sections include:

- Market sizing & outlook: Transparent methodology, historical reconciliation (2020–2025), and scenario forecasts (2026–2032) that support budgeting and strategic planning.

- Demand drivers & end‑use economics: Breakdown of the forces shaping purchases — equipment replacement cycles, abrasive media evolution, regulatory drivers and OEM specification trends — with actionable levers for procurement and operations.

- Supply‑chain diagnostics: Raw material flow mapping, lead‑time and logistics stress testing, and a cost‑to‑serve model that identifies the top three sensitivity points that materially affect landed cost.

- Technology & product matrix: Comparative evaluation of key wear solutions (steel overlays, ceramic inserts, polymer linings and hardfacing alloys) using standardized wear‑test conversion factors and lifecycle curves developed from lab and field data.

- Supplier scorecards & negotiation playbook: A repeatable framework to assess vendor technical capabilities, manufacturing footprint, quality control and carbon intensity — accompanied by templated RFP language and negotiation levers tailored to volume bands and service levels.

- Strategic growth & M&A roadmap: Playbooks for bolt‑on acquisitions, licensing strategies and co‑development partnerships that accelerate time‑to‑market for higher‑performance overlays.

- Regulatory & scenario planning: Specific scenarios modelling the near‑term impact of trade measures and carbon tariffs, and recommended mitigation pathways for exposed buyers and suppliers.

Competitive landscape — who to watch and what they mean for your strategy

The industry comprises specialty fabricators, hardfacing alloy suppliers and vertically integrated manufacturers. Key firms profiled in the report include Wear Plate USA, ASGCO Manufacturing, JADCO Manufacturing, Halden, Tianjin Leigong Welding Alloys and Metco Joining & Cladding. Each profile includes capabilities mapping, manufacturing technologies, geographic footprint, customer segments and strategic intent.

- Wear Plate USA (North Carolina, USA): Focused on custom‑engineered wear plates and hardfacing solutions for mining and heavy equipment — a go‑to partner for application‑specific engineering and rapid customization.

- ASGCO Manufacturing (Allentown, USA): Known for Chromium Carbide Overlay (CCO) and engineered ceramic solutions for conveyance and chute protection — strong in aftermarket channel partnerships.

- JADCO Manufacturing (Harmony, USA): Maintains integrated CCO production and has recently introduced thinner CCO plates that extend service life in tight‑space applications — an example of incremental product innovation that changes replacement cadence.

- Halden (China): A supplier with high‑volume abrasion‑resistant steel production and custom hardfacing capability, offering cost advantages for large‑scale projects.

- Tianjin Leigong Welding Alloys (Tianjin, China): Specializes in hardfacing wires and overlay solutions optimized for mining and steel applications; relevant for firms evaluating upstream alloy consistency.

- Metco Joining & Cladding (Westbury, USA): Provides welding overlays and alloy solutions, serving industrial and mining customers that require specialized metallurgical support.

Recent market activity underscores an innovation‑led cadence: product launches and catalog refreshes from OEMs and suppliers signal a shift to higher value, performance‑oriented offerings. For example, a 2025 launch of thin Chromium Carbide Overlay plates with narrower hardfacing bead widths reflects a deliberate push to increase service life in high‑abrasion equipment, while catalog updates from established players indicate ongoing product refinement rather than commoditization.

Regulation, decarbonization and supply‑chain resilience

The regulatory environment is an active variable for 2026 planning. CBAM and similar carbon‑linked trade measures create a two‑fold effect: first, they change landed costs for imported plates and overlay feedstock; second, they elevate the value of low‑carbon manufacturing footprints in supplier selection. PW Consulting models carbon tariff sensitivity across plausible trajectories and provides mitigation playbooks — from near‑term contractual hedges to mid‑term supplier diversification and long‑term local capacity investments.

Companies that proactively quantify embedded carbon in wear plate lifecycle assessments and incorporate carbon clauses into supplier scorecards will enjoy both commercial protection and preferential access to increasingly climate‑conscious buyers.

Actionable recommendations for 2026

- Reframe procurement KPIs: Shift from unit price to lifecycle cost metrics that include installation downtime, scheduled maintenance windows, and reclamation or recycling value.

- Run supplier stress tests: Execute a rapid diagnostic on your top three suppliers across lead time, carbon intensity, and technical interchangeability to identify single‑points‑of‑failure.

- Pursue targeted co‑development: Negotiate joint development agreements for thin‑overlay and ceramic‑hybrid plates where equipment design enables longer replacement intervals.

- Prepare for CBAM exposure: Map your import exposure into EU markets, and prioritize low‑carbon or local suppliers for critical, high‑volume flows.

- Use M&A selectively: Look for bolt‑on engineering houses with unique metallurgical competencies or regional fabrication footprints to accelerate service coverage without large greenfield investments.

How PW Consulting’s report supports implementation

Beyond analysis, the report provides templates and tools that accelerate action in 2026: vendor RFP templates, total cost of ownership calculators, a supplier scorecard with weighted criteria, wear‑test conversion matrices and scenario planning decks that can be dropped into board and investment committee materials. Our consulting engagement layer converts findings into a 90‑day implementation sprint tailored to client priorities (procurement rationalization, technical trials, or M&A diligence).

About the intelligence you won’t find here (and why)

In keeping with our “trailer” approach, this briefing presents the strategic signal and the operational levers you need to decide to act in 2026, while preserving the report’s granular segmentation tables, supplier pricing curves and downloadable vendor scorecards for licensed report access. The report contains detailed splits by region, material and application, supplier concentration tables, and downloadable annexes required for procurement bid rounds — content we intentionally reserve for the full report to preserve the commercial integrity and reusability of those datasets.

Next steps

- If you are preparing capital or sourcing plans for 2026: engage PW Consulting for a tailored 90‑day readiness assessment.

- If you lead procurement or plant operations: request the supplier scorecard and lifecycle cost model to validate supplier negotiations and maintenance schedules.

- If you are a C‑level executive evaluating strategic moves: leverage our M&A readiness checklist and CBAM exposure assessment to align board guidance with regulatory shocks.

For executives ready to convert market insight into measurable outcomes, PW Consulting’s Wear Plate Market report is the operational intelligence package to prioritize initiatives, accelerate trials and protect margins as the market scales toward the projected USD 519.0 Million mark in 2032. To access the full dataset, granular segmentation and downloadable tools, visit the PW Consulting research portal or contact our industry practice.

For detailed analysis of this topic, please visit the official page:Wear Plate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com