Food Automation Market: Size, Share, and Future Growth

Other |

2026-05-05 07:00:10

PW Consulting today releases a strategic preview of our forthcoming Physiological Saline Market report (base year 2025, forecast 2026–2032). The global market demonstrated steady expansion through the first half of the decade — rising from approximately USD 3,500 million in 2020 to USD 5,200 million in 2025 — and is projected to reach roughly USD 8,800 million by 2032, reflecting a 7.4% compound annual growth rate over the forecast window. For 2026 corporate planning cycles, this trajectory demands a calibrated mix of supply-side resilience, channel optimization, and targeted portfolio moves. This article summarizes the operationally oriented insights and strategic implications contained in the full report; detailed subsegment sizing and granular competitive matrices are intentionally reserved for the full study to preserve proprietary value and guide readers to our source page for complete intelligence.

Physiological Saline Market

Demand momentum: With the market expanding materially from 2020–2025 and the forecast signaling continued acceleration, organizations must convert top-line growth into durable margins through process, product and channel interventions.

Physiological Saline Market

Supply-side volatility: The industry’s recent disruption cycle has demonstrated the operational impact of manufacturing, raw-material and regulatory shocks — making redundancy, alternative packaging formats and strategic inventory policy business-critical.

Physiological Saline Market

Regulatory and reimbursement context: Recent regulatory shifts and coding updates have immediate commercial repercussions for contracting, pricing and service models across inpatient and outpatient channels.

Competitive dynamics: A moderately concentrated supplier base — with leading firms commanding a clear share advantage — creates both partnership opportunities and consolidation threats for mid-tier players.

The market expanded from about USD 3.5 billion in 2020 to roughly USD 5.2 billion by the 2025 base year, with a discrete uptick around 2023–2025 as manufacturing re-capacity and restored supply chains supported resumed clinical demand. Our forecast conservatively models continuation of the secular drivers — increased procedural volumes, growth in ambulatory infusions, emergency preparedness and rising access in emerging healthcare systems — resulting in an estimated market size of approximately USD 5.46 billion in 2026 and approaching USD 8.8 billion by 2032. The underlying 7.4% CAGR reflects a balance of steady clinical demand and incremental value-capture opportunities across packaging, formulation and channel innovation.

Robust market-sizing and forecasting methodology, including scenario modeling and sensitivity analyses for raw material price shocks, capacity outages and regulatory interventions.

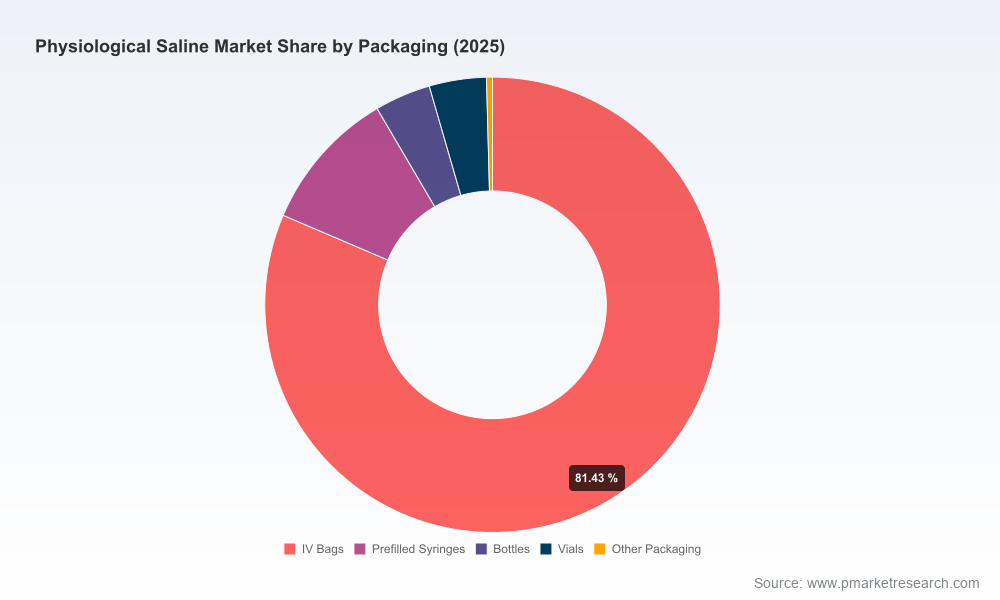

Segment taxonomy and demand mapping across concentration types, packaging formats and go-to-market channels — with unit economics and margin ladders for each node.

Supply-chain risk heatmap and mitigation playbooks: supplier scorecards, dual-sourcing templates, onshore/offshore manufacturing trade-offs and packaging transition roadmaps (PVC vs non-PVC/DEHP-free options).

Commercial playbooks: contracting levers, payer negotiation templates, and pricing scenarios aligned with HCPCS/CPT coding dynamics and recent reimbursement benchmarks.

Competitive landscape dossiers and strategic profiles for incumbent and emerging suppliers, including capability matrices, channel footprints and M&A opportunity maps.

Implementation toolkits: financial models, KPI scorecards, milestone-driven project plans for capacity expansion or partnership roll-outs.

Supply normalization: The FDA officially declared the nationwide shortage of sodium chloride 0.9% injection resolved in August 2025; hospitals were advised to transition back to FDA‑approved sources. While this reduces immediate procurement strain, it also resets baseline supplier expectations and contractual standards.

Coding and billing implications: HCPCS code J7030 continues to be a reference point for billing of 1,000 cc normal saline infusions under Medicare, with reimbursement typically ranging in the low-single digits per unit depending on setting — an important factor in infusion economics and contracting discussions. In parallel, CPT revisions relevant to pre‑packaged IV hydration services took effect in September 2025, re-shaping revenue flows for outpatient infusion providers.

Implication for payers and providers: These regulatory touchpoints reinforce the need for manufacturers to present clear value propositions — stability of supply, packaging compatibility with infusion systems, and documentation to support coding and reimbursement.

The market’s competitive topology remains defined by a mix of global medtech and pharma-grade IV fluid manufacturers, regional formulators and specialized contract manufacturers. Market concentration is meaningful — the top three players account for a majority share and the top five increase that share materially — creating a backdrop where strategic partnerships and distribution alignments often unlock the fastest route to scale.

Baxter International Inc. (Deerfield, IL) continues to leverage its Viaflex and Viaflo container platforms and broad hospital relationships to deepen penetration. Recent geographic expansion initiatives underscore Baxter’s focus on widening commercial access.

B. Braun Melsungen AG (Melsungen, Germany) relies on a longstanding presence in IV therapy and a manufacturing footprint optimized for extracellular fluid replacement products, prioritizing supplier reliability and clinician familiarity.

Fresenius Kabi AG (Bad Homburg, Germany) couples its Freeflex bag technology with distribution partnerships to increase availability in targeted markets — a strategy recently amplified through new distribution agreements.

ICU Medical, Inc. (San Clemente, CA) has differentiated with flexible non‑PVC/non‑DEHP container offerings and joint manufacturing arrangements that prioritize compatibility with evolving infusion systems and clinician safety preferences.

Grifols and related entities remain focused on hospital and plasma-donation channels with polypropylene bag formats, leveraging their plasma-business scale and hospital relationships.

Otsuka Pharmaceutical participates in North American supply through localized entities and partnerships, emphasizing regulatory compliance and localized production pathways.

AdvaCare Pharma and smaller contract manufacturers populate niches in irrigation and saline injections for specific use cases, making them interesting targets for tactical acquisitions or outsourcing agreements.

Recent developments reinforce these strategic postures: Baxter announced a geographic expansion in March 2026 to strengthen access to its saline portfolio, and Fresenius has moved to shore up distribution through a March 2026 partnership — both moves that speak to the importance of scale and channel control in 2026 planning.

Strengthen supplier resilience: Implement dual‑sourcing and contract clauses that prioritize on‑time delivery, quality KPIs and rapid scale-up options. Consider co-investment models with select contract manufacturers to secure prioritized capacity.

Optimize packaging strategy: Accelerate evaluation of non‑PVC and other clinician-preferred formats to anticipate hospital procurement preferences and regulatory shifts. Packaging transitions take quarters to operationalize and should be started now.

Align commercial strategy with coding and reimbursement: Use HCPCS and CPT updates to build payer negotiation playbooks that emphasize total cost-of-care advantages for stable supply and lower downstream administrative burden.

Pursue targeted M&A or distribution partnerships: For mid‑sized firms, partnership with a leading distributor or acquisition of niche packaging capabilities can shortcut market access and materially improve bargaining power.

Operationalize scenario-led planning: Run three supply‑disruption scenarios in your 2026 budget cycle (baseline, adverse, and severe) and attach contingency budgets and trigger-based surge plans to each.

For executives preparing 2026 budgets and strategic roadmaps, the full PW Consulting Physiological Saline Market report provides the decision-grade intelligence needed to prioritize investments, structure commercial agreements, and execute operational changes with confidence. Our deliverables include downloadable financial models, supplier scorecards and a phased implementation playbook tailored to manufacturers, distributors and large health systems.

Please note: to preserve competitive integrity and to encourage direct engagement with our analysts, the full subsegment tables and granular regional/application-level sizing are available exclusively in the full report. If your organization requires bespoke scenarios, integration analysis or competitor due diligence, PW Consulting offers a short-form advisory engagement that converts the report’s findings into a prioritized 90-day action plan.

Visit our report page to access the full study and supporting models.

Schedule a briefing with PW Consulting’s Healthcare and Life Sciences practice to review customized implications for your organization’s 2026 plans.

PW Consulting’s senior analysts remain available to walk through the report’s assumptions, sensitivity analyses and the practical steps that will convert market growth into sustained commercial advantage in 2026.

For detailed analysis of this topic, please visit the official page:Physiological Saline Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com