PW Consulting: Water Treatment Equipment Market Outlook — Strategic Briefing for 2026 Decision‑Makers

PW Consulting today publishes a strategic briefing accompanying our full Water Treatment Equipment Market research report, designed to equip boardrooms, corporate development teams, investors, and public utilities with the forward‑looking intelligence required for high‑stakes decisions in 2026. Built on a comprehensive historical base (2020–2025) with 2025 as the report’s base year, our forecast extends through 2032 and quantifies a robust industry expansion at a 6.2% CAGR. The global market reached USD 66.0 Billion in 2025 and, under our central scenario, is on a trajectory toward roughly USD 100 Billion by the end of the forecast window.

Water Treatment Equipment Market

Why this briefing matters for 2026

- Fiscal planning and CapEx cycles: Municipal and industrial capital programs are being reworked in response to new regulation and infrastructure financing opportunities. The timing and scale of procurement decisions made in 2026 will determine technology lock‑in and cost structures for the next decade.

- Regulatory inflection points: Recent and imminent policy actions are accelerating demand for smart, energy‑efficient, and legally compliant systems. Our report maps regulatory levers to market outcomes so you can prioritize compliance investments and capture upside in incentivized projects.

- Technology and service transformation: Digital monitoring, AI‑enabled controls, next‑generation membranes, and modular ZLD systems are shifting competitive advantage from hardware alone to integrated outcomes. Our briefing highlights which capabilities translate to sustainable margin expansion.

- M&A and partnership timing: With market concentration remaining relatively low (top‑three players do not command majority control; the top five account for roughly 30% of the market), the industry is ripe for strategic consolidation and cross‑border alliances in 2026.

Methodology and the rigor behind our projections

Our conclusions reflect a multi‑layered research methodology: primary interviews with OEMs, utilities, and large industrial users; proprietary demand models calibrated across the historical period (2020–2025); bottom‑up equipment shipment analysis; and macro overlays incorporating energy, regulatory, and infrastructure funding scenarios. We stress‑tested our base case with upside and downside scenarios that incorporate accelerated regulatory rollout, energy price shocks, and rapid adoption of circular water technologies. All forecasts are provided in constant USD and include sensitivity bands to support rapid scenario planning.

Water Treatment Equipment Market

What the full report delivers — practical, board‑ready outputs

- Comprehensive market model (2020–2032) with downloadable financial templates you can adapt to company‑level assumptions.

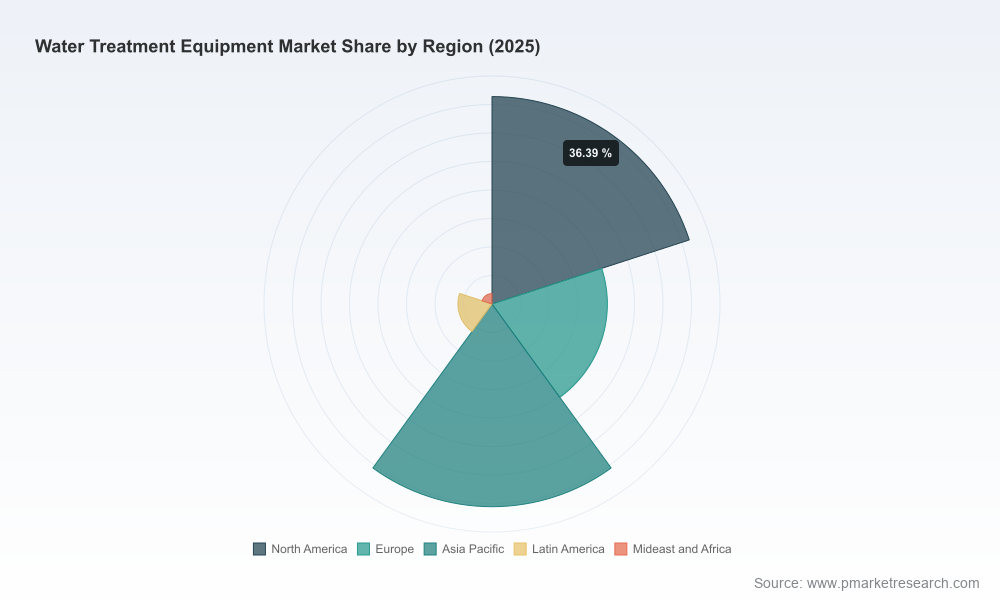

- Segmentation and demand drivers by type, application, and region (note: the public briefing intentionally omits detailed segment tables; the full report contains granular splits and interactive dashboards).

- Strategic playbook for incumbents, challengers, and new entrants—covering product, service, pricing, and channel strategies.

- Supplier and component risk matrix, including membrane and pump sourcing vulnerabilities and mitigation levers.

- Go‑to‑market frameworks for retrofit vs. greenfield opportunity capture, and procurement frameworks aligned to public financing instruments.

- Detailed company profiles and competitive scorecards covering technology portfolios, commercial capabilities, and M&A positioning.

- Case studies and CAPEX/OPEX benchmarking drawn from municipal and industrial implementations.

Market dynamics shaping 2026 strategy

The water treatment equipment market in 2026 will be shaped by an interplay of regulatory pressure, infrastructure investment needs, energy considerations, and rapid product innovation. Key dynamics we highlight in the report include:

Water Treatment Equipment Market

- Regulatory funding and mandates: Public financing programs and mandates for smart water management continue to unlock large retrofit pipelines. Financing instruments are re‑shaping procurement, creating structured opportunities for vendors that can offer performance guarantees and lifecycle services.

- Infrastructure backlog and prioritization: National assessments of clean water infrastructure highlight vast remediation and replacement needs. These imperatives prioritize projects that deliver demonstrable resilience and efficiency gains, accelerating demand for modular, quick‑deploy solutions.

- Energy and lifecycle economics: Water and wastewater systems are a meaningful portion of municipal energy demand. Advances in energy optimization—driven by AI‑enabled pump control and process electrification—are now a primary decision criterion for buyers seeking total cost of ownership reductions.

- Technology diffusion: The market is experiencing parallel innovation fronts—advanced disinfection and membrane technology, modular zero liquid discharge, and integrated digital platforms that convert equipment into recurring service revenue streams.

Competitive landscape — from global integrators to specialized innovators

The competitive map is a mosaic of global integrators, specialty equipment manufacturers, chemistry and consumables providers, and regional system houses. Leading global players combine service networks, engineering scale, and digital platforms; specialist firms compete on niche technology and cost‑effective modularization. Representative companies profiled in our study include Aquatech, Calgon Carbon, The Dow Chemical Company, Evoqua, Veolia, SUEZ, Xylem, Pentair, Ecolab, Kurarita Water Industries, Grundfos, Newater, and a set of strong U.S. distributors and system integrators.

Key strategic patterns we identify:

- Platformification: Firms that layer digital monitoring, predictive maintenance, and outcome‑based contracting onto equipment capture higher recurring revenue and tighter customer relationships.

- Vertical bundling: Chemistry providers and OEMs are leveraging bundled solutions (chemicals + control + equipment) to increase switching costs and improve margins.

- Modularization and speed to market: New entrants offering modular ZLD and containerized treatment systems are outflanking traditional EPC models on speed, capital intensity, and suitability for constrained sites.

- Service and retrofit focus: Given the large installed base, aftermarket services, retrofits, and efficiency upgrades are proving as valuable as new equipment sales for long‑term growth.

Recent industry signals and tactical implications

- Product innovation continues: The market has seen launches of intelligent pump systems and next‑generation UV and RO systems that combine higher performance with lower energy intensity. These product introductions validate the premium assigned to energy and digital features in procurement decisions.

- Modular ZLD momentum: New modular ZLD solutions target industrial customers under tightening discharge rules, making ZLD economically feasible for a broader set of facilities.

- Policy tailwinds: Public financing programs and smart‑technology mandates are increasing project pipelines while shifting buyer preferences toward vendors that can demonstrate end‑to‑end compliance and energy savings.

Strategic implications and recommended 2026 actions

- Prioritize product roadmaps that reduce lifecycle energy and integrate digital controls. Energy efficiency is now a procurement pass/fail criterion in major public tenders.

- Accelerate service‑centric business models. Convert one‑time equipment sales into recurring revenue through digital monitoring, spare part programs, and performance guarantees.

- Prepare for bolt‑on M&A focused on modular technologies, digital platforms, or regional distribution networks—targets that improve margin resilience and customer proximity.

- Pursue public‑private financing partnerships. Vendors who can structure performance‑based contracts aligned to available funds will win larger shares of municipal projects.

- Embed supply chain resilience into product costing. Membranes, advanced polymers, and specialized electronics are focal points for lead times and cost volatility.

Risk considerations for investors and operators

Decision‑makers should weigh several asymmetric risks in 2026: regulatory reversals or delays in funding disbursements; accelerated energy price inflation that could compress operator budgets; and rapid technology commoditization that pressures hardware margins. Conversely, firms that own software IP, service contracts, and financing capability are positioned to capture outsized returns.

Next steps — obtaining the full intelligence

This briefing is a strategic extract designed to inform immediate 2026 planning. The full PW Consulting Water Treatment Equipment Market report contains the granular segmentation tables, regional and application breakdowns, company valuations, deal flow maps, and the downloadable market model used to generate our forecasts. For organizations planning capital commitments, portfolio pivoting, or M&A in 2026, we recommend commissioning a tailored briefing that applies our model to your asset base and risk tolerance.

To request the full report or arrange a customized executive workshop, contact PW Consulting’s industry team. Our analysts are available to present scenario walk‑throughs, validate pipeline assumptions, and co‑develop a 90‑day action plan aligned to your strategic priorities.

For detailed analysis of this topic, please visit the official page:Water Treatment Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com