Feed Pellet Machine Market Regional Analysis 2025 to 2031

Other |

2026-03-11 18:38:51

As radiopharmaceuticals transition from niche clinical tools to mainstream oncology and diagnostic staples, corporate leaders face a compressed window to convert scientific momentum into durable commercial positions. PW Consulting’s new market study — grounded in a 2025 base year and a historical review spanning 2020–2025, with forecasts through 2032 — synthesizes commercial, operational and regulatory intelligence to support high-consequence decisions in 2026. The global market, which we measure in USD Billion, expanded from roughly 3.5 in 2020 to 6.0 in 2025 and is projected to reach approximately 10.56 by 2032, reflecting a compound annual growth rate (CAGR) of 8.5% across the 2026–2032 forecast window.

Radiopharmaceuticals Market

Acceleration and scale: Renewable clinical adoption, improved isotope availability and favorable reimbursement constructs are collectively shifting radiopharmaceuticals from specialized programs into scalable product lines. Boardrooms need quantitative evidence and actionable roadmaps to time investments — especially in manufacturing and supply chain — to avoid both underinvestment and stranded assets.

Radiopharmaceuticals Market

Policy-driven economics: Recent policy changes and draft regulatory guidance are altering the economic calculus for domestic production, pricing and reimbursement. Firms without a clear regulatory and reimbursement scenario plan risk margin compression or missed market access windows.

Radiopharmaceuticals Market

Consolidation opportunity: Market concentration metrics in our analysis indicate a moderate-to-high level of aggregation among leading players, creating distinct M&A and partnership arbitrage possibilities for entrants and incumbents alike.

PW Consulting’s report is designed as a working toolkit for 2026 decision-making. It combines proprietary datasets, facility-level capability assessments and strategic playbooks to enable rapid execution. Key deliverables include:

Comprehensive market model (2020–2032) in USD Billion with scenario runs that stress-test demand, pricing, tariff shocks and reimbursement permutations.

Facility and capacity atlas: an operational map of GMP-capable sites, ramp timelines and capital intensity estimates to support build-vs-buy decisions.

Supply-chain risk heatmap focused on critical isotopes and inputs, with mitigation pathways (e.g., contract manufacturing, vertical integration, geographic hedging) tied to cost and time trade-offs.

Regulatory and reimbursement playbook: distilled implications of recent CMS and FDA actions with templated filing and evidence-generation roadmaps aligned to fast-to-market clinical strategies.

Commercial launch templates and pricing models that translate clinical effect sizes into revenue curves under alternative reimbursement regimes.

M&A and partnership screen: prioritized capability gaps, likely targets by strategic fit, and accretion/dilution scenarios for near-term transactions.

The competitive field is dynamic: established CDMOs, vertically integrated isotope producers and agile therapeutics developers are each staking adjacent plays. Our qualitative and quantitative assessment highlights several strategic positions to monitor in 2026.

Telix Pharmaceuticals (Melbourne, Australia) — Telix Manufacturing Solutions has operationalized major GMP capacity in Europe and expanded into Japan. Their multi-site manufacturing footprint positions them well to serve cross-border clinical and commercial demand, especially where regional regulatory acceptability and speed-to-supply are important. Expect Telix to press on both scale and service breadth.

ITM Isotope Technologies Munich SE (Garching near Munich, Germany) — ITM’s vertical integration and leadership in key therapeutic isotopes position them as a strategic supplier for oncology-focused radiotherapies. Their control over isotopics and late-stage manufacturing chain reduces single-source risk for partners and clients seeking secure supply.

CDMOs — Nucleus RadioPharma (Rochester) and Evergreen Theragnostics (Springfield) — These US-based full-service providers are central to commercial scale-out strategies for sponsors that choose outsourced manufacturing. Their ability to offer end-to-end development and regulatory support will be a decisive factor for mid-size sponsors and novel therapy entrants.

Specialist producers — PanTera (Mol, Belgium), RayzeBio (San Diego) and Perspective Therapeutics (Florida) — PanTera’s specialized photonuclear approach for precursors and its recent permitting milestone indicate a potential step-change in precursor security. RayzeBio and Perspective’s therapy-focused pipelines (Lu-177 and targeted alpha emitters respectively) illustrate the therapeutic innovation driving long-term market value.

Distribution and scale partners — Cardinal Health (Dublin, Ohio) — Incumbent logisticians and distributors remain central to clinical deployment. Their network and regulatory know-how lower commercialization friction and are often decisive for payer acceptance and hospital adoption.

Manufacturing and partnership moves: Strategic investments and new facilities announced in 2025–2026 (including partnerships to build sizeable research and manufacturing sites and go-live of new GMP facilities) expand capacity but also underscore the long lead times required to monetize capacity — a key timing risk for 2026 strategies.

Isotope supply tension: Persistent shortages in high-demand isotopes such as Lu-177 and Ac-225 have been documented industry-wide. These shortages mean sponsors and CDMOs will increasingly compete on guaranteed supply, not just cost.

Tariffs and trade policy: The April 2026 Section 232 proclamation introducing significant tariffs on pharmaceutical imports and key starting materials alters the economics for global sourcing. Firms must model the phased effective dates and run sensitivity analysis on supply chain reconfiguration costs.

Reimbursement and regulatory signals: Two policy shifts are immediately actionable — a CMS add-on payment favoring domestically produced Tc-99m doses and CMS retention of a mean unit cost methodology for radiopharmaceuticals — and the FDA’s August 2025 Draft Guidance on dosage optimization for oncology radiotherapeutics. Together, these create both incentive and complexity for domestic production and clinical trial designs.

We recommend executives center 2026 planning on five pragmatic priorities.

Prioritize supply certainty over unit cost — Where isotopes are constrained, the premium associated with guaranteed availability often outweighs marginal manufacturing cost advantages. Secure multi-year supply agreements, invest in secured precursor capacity or pursue JV structures for critical isotopes.

Reassess the build-versus-buy calculus — Tariff exposure and new domestic reimbursement add-ons change the NPV of local manufacturing. Run parallel capital allocation scenarios that reflect tariff incidence, ramp timelines and payor responses to domestically sourced products.

Embed regulatory-readiness into clinical development — FDA dosing guidance and CMS payment rules create an advantage for sponsors who design trials to support optimized dosing and cost-effectiveness evidence from first-in-human studies through registrational stages.

Use M&A and partnerships to close capability gaps quickly — Given the measured concentration of market share among top players, targeted acquisitions or capacity-sharing agreements can accelerate market access and secure distribution channels more quickly than greenfield builds.

Stress-test commercial models against policy shocks — Incorporate tariff scenarios and CMS rule changes into pricing, payer negotiations and payer mix forecasts. Opportunistic reshoring strategies should be evaluated not only for cost but for competitive differentiation in reimbursement negotiations.

The full report offers the analytic foundation to execute the priorities above: granular facility-level timelines, capital cost curves, a supplier risk index, and an M&A target matrix prioritized by strategic fit and execution risk. Our scenario engine quantifies the revenue and margin sensitivity to tariffs, reimbursement changes and isotope availability so executives can pivot from hypothesis to action with confidence.

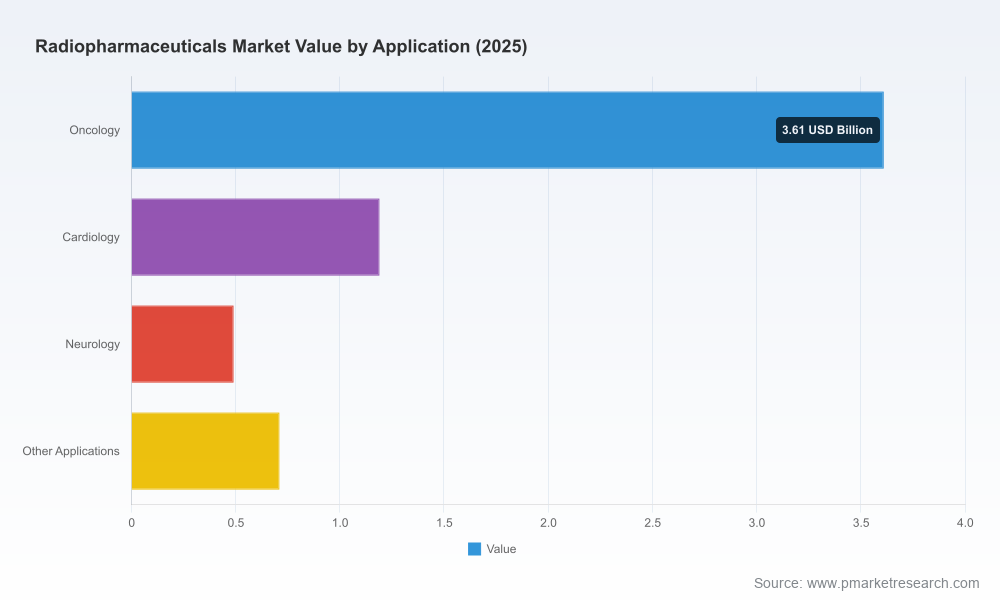

We have intentionally omitted detailed regional and application-level breakdowns from this release to preserve the strategic value of the full dataset. The complete report contains the segmented forecasts, pricing ladders and facility-by-facility capacity assumptions that boards and investment committees will require to approve capital deployment in 2026.

Request a strategy briefing: PW Consulting offers tailored executive workshops that translate the report’s scenarios into a 90‑ to 180‑day action plan for manufacturing, regulatory and commercial teams.

Run a supply-chain stress test: Use our supplier risk index and scenario models to quantify exposure to tariffs and isotope shortages and identify rapid mitigation options.

Evaluate M&A and partnership candidates: Leverage our M&A scoreboard to prioritize targets that accelerate time to market and secure isotopic inputs.

For senior teams preparing 2026 budgets and capital plans, the difference between opportunity capture and playing catch-up will hinge on timely, data-driven choices about capacity, partnerships and regulatory strategy. PW Consulting’s Radiopharmaceuticals Market report combines the market sizing, policy impact analysis and operational intelligence to make those choices practical and defensible. To obtain the full report and schedule a briefing, visit our website or contact our industry desk for access to the underlying datasets and bespoke scenario modeling.

For detailed analysis of this topic, please visit the official page:Radiopharmaceuticals Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com