Functional Cacao Mix Market Growing at 5.6% CAGR Through 2034

Other |

2026-06-16 10:37:58

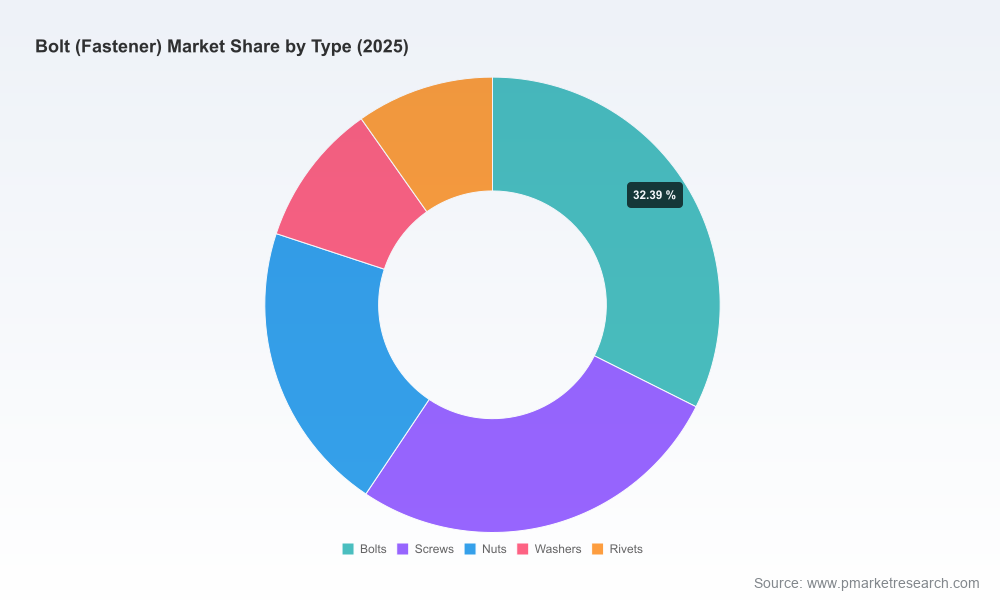

PW Consulting today releases a strategic preview of our forthcoming Bolt (Fastener) Market report, designed to equip corporate leaders with decision-grade insight as they firm up plans for 2026. Built on a comprehensive base-year of 2025 and a detailed historical review from 2020–2025, the study projects forward through 2032. At the macro level, the global bolt and fastener market expanded from approximately USD 71.0 Million in 2020 to USD 91.04 Million in 2025, and our modelling anticipates a compound annual growth rate (CAGR) of 3.48% across the 2026–2032 forecast horizon, with a scenario range that sees the market approaching the mid-hundreds by 2032.

Bolt (Fastener) Market

Timing: 2026 is a pivot year for supply chain normalization, standards consolidation, and capital allocation across manufacturing-intensive sectors. Companies that integrate near-term market scenarios into procurement, product roadmaps, and M&A pipelines will materially improve execution risk and ROI.

Bolt (Fastener) Market

Clarity amid complexity: Raw material volatility, emerging standards, and shifting regional demand patterns are creating friction in sourcing and price forecasting. Our preview identifies the levers executives must control to convert uncertainty into competitive advantage.

Bolt (Fastener) Market

Operational readiness: The report is structured to translate market intelligence into operational tasks — from inventory optimization and dual-sourcing playbooks to product qualification and supplier rationalization templates.

Between 2020 and 2025 the market demonstrated steady recovery and expansion — climbing from roughly USD 71.0 Million to USD 91.04 Million — reflecting a rebound in end-use industries and structural restocking. Our forecast shows continued positive momentum into 2026 and beyond, with modeled outcomes that account for mid-cycle volatility. The base-case indicates a continuation of modest growth at a 3.48% CAGR through 2032, with the market trending toward a significantly larger absolute scale by the end of the forecast period.

Importantly, the historical and forecast series reveals episodic variance rather than uninterrupted growth — a pattern that underscores the need for scenario planning. For example, short-term supply shocks, raw-material spikes, or demand-side pullbacks can produce year-on-year fluctuations. Leading firms will translate this insight into flexible contracts, dynamic safety-stock policies, and expedited qualification processes that reduce time-to-market for critical cold-rolled and high-strength fasteners.

Raw-material pressures: Steel remains the single largest input cost driver for most fastener product lines. As of June 5, 2026, steel prices stood at 3,152 CNY/T — roughly 6.88% higher than the same point a year earlier — reinforcing the need for hedging strategies, alloy substitutions where feasible, and contract clauses that share price risk.

Standards and technical governance: The Industrial Fasteners Institute’s recent initiatives — including the first Standards Camp and strengthened technical committee oversight — signal an industry moving toward harmonized specifications. Firms that engage early on standards development gain first-mover advantages in certified products and reduce later rework and qualification costs.

Macro policy responses: The OECD’s Steel Outlook has highlighted intensifying international efforts to address steel excess capacity, which has downstream implications for supply availability and pricing dynamics. Manufacturers must evaluate geopolitical risk overlays in sourcing and evaluate regional supplier portfolios accordingly.

Labor and capacity constraints: Global industry employment remains sizable, with over three million workers associated with the fastener sector. Labor shortages persist in several production hubs, driving automation investment, selective reshoring, and a redefinition of cost models that incorporate higher direct-operating labor risk.

The market shows a moderate degree of concentration; our analysis estimates the top three players account for roughly 35% of the market, while the top five approach 42% — a configuration that creates both competitive pressure and partnership opportunities for mid-market suppliers. Key companies playing noticeable strategic roles include:

Würth Group (Künzelsau, Germany) — A global full-line supplier with an extensive branch network and a broad catalog covering bolts, screws, and industrial assembly materials. Their worldwide footprint and distribution model make them a benchmark for aftermarket and trade-channel strategies.

LISI Group (Grandvillars, France) — Known for fasteners and assembly components tailored to aerospace, automotive and medical applications. Their high-spec engineering focus highlights the premium segment dynamics and the importance of qualification cycles.

Bossard Group (Zug, Switzerland) — A specialist in fastening technology and logistics systems for manufacturing and automation. Bossard exemplifies the integration of inventory-as-a-service and engineering support that many OEMs now demand.

SFS Group (Heerbrugg, Switzerland) — Focused on precision mechanical fastening systems and assemblies. SFS’s product breadth for industrial use-cases underlines the strategic importance of engineering-to-order capabilities.

Bulten AB (Gothenburg, Sweden) — A supplier focused on automotive fasteners and precision components, illustrating supplier strategies tied to major OEM programs and tiered supplier ecosystems.

Hilti Corporation (Schaan, Liechtenstein) — Playing in high-performance construction fasteners and associated toolsets, Hilti demonstrates how product-plus-service models capture long-run value in professional construction markets.

Precision Castparts Corp (Lake Oswego, Oregon, USA) — A provider of investment-cast and forged components including high-strength fasteners for aerospace and power generation, emphasizing the pull from capital-intensive end markets.

Collectively, these players illustrate divergent strategic archetypes — full-line distributors, engineering-specialists, logistics-integrators, and premium OEM suppliers — each implying different competitive responses for smaller producers and buyers alike.

Our full report is engineered for application. Highlights include:

Actionable procurement playbooks — including contract designs, pricing indexation templates, and dual-sourcing decision matrices calibrated to the fastener product family.

Supply-chain resilience protocols — step-by-step guides for rapid supplier qualification, on-call manufacturing capacity triggers, and inventory containment strategies that balance working capital with service levels.

Product strategy blueprints — prioritized R&D and qualification roadmaps for high-strength, coated, and precision fastener lines addressing aerospace, automotive, construction and industrial machinery needs.

M&A and partner-screening frameworks — valuation levers, integration risk checklists, and functional scorecards tailored to bolt/fastener target companies, including due-diligence red flags tied to material sourcing and technical certification.

Scenario-based financial models — three market scenarios (conservative, base, upside) that stress-test revenue, margin, and working-capital outcomes across 2026–2032; models are delivered in editable formats for client-specific inputs.

Note: while this preview highlights the structure and strategic utility of the report, granular segmentation tables and proprietary model outputs are deliberately reserved for the full publication and subscriber portal.

Procurement: Implement indexed contracts tied to transparent steel-price benchmarks and create a two-tier sourcing strategy that differentiates long-lead, high-value fasteners from commodity items.

Operations: Prioritize modular automation investments in high-labor-cost production lines and accelerate supplier digital-integration pilots to reduce qualification lead times.

R&D and Product: Fast-track coatings and lightweight alloys for segments where performance premium justifies extended qualification times, and align product roadmaps with emerging standards from technical bodies.

Corporate Strategy: Use the report’s M&A playbook to identify bolt/fastener assets that provide access to specialized OEM channels or logistics capabilities that shorten delivery windows.

Trade forums: Fastener Fair USA (May 2026, Louisville) and the International Fastener Expo (October 2026, Phoenix) will reveal supplier roadmaps, new tools for automated assembly, and distribution strategies. Attendance is recommended for commercial and sourcing teams intent on rapid supplier vetting.

Standards engagement: The Industrial Fasteners Institute’s ongoing programs — including its recent Standards Camp and leadership changes — are a leading indicator for forthcoming specification updates. Early participation or monitoring is essential for product teams managing qualification timelines.

Commodity markets: Monitor steel price movements and OECD policy announcements on capacity management, as these will materially affect margin timing and contract negotiation levers.

Our findings derive from a synthesis of primary supplier interviews, purchaser surveys, public financial statements, trade-show intelligence gathered in 2026, and macro inputs. Where possible we triangulated price and volume movements with independent market sources and validated scenario outcomes against historical volatility patterns observed between 2020 and 2025.

This preview is intended to catalyze strategic conversations and operational planning for 2026. For access to the complete dataset, detailed segmentation tables, interactive scenario models, and proprietary supplier scorecards, please consult the full PW Consulting Bolt (Fastener) Market report and subscriber portal. The complete report contains the specific, transaction-ready intelligence organizations need to convert market visibility into measurable advantage.

PW Consulting remains available to brief executive teams, lead bespoke strategy workshops, and operationalize the report’s recommendations into deliverable programs. Contact details and subscription options are available on our publication landing page.

For detailed analysis of this topic, please visit the official page:Bolt (Fastener) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com