Best Luxury Hotels in Velachery Chennai-Experience Comfort at Dhans

Other |

2026-06-19 11:34:20

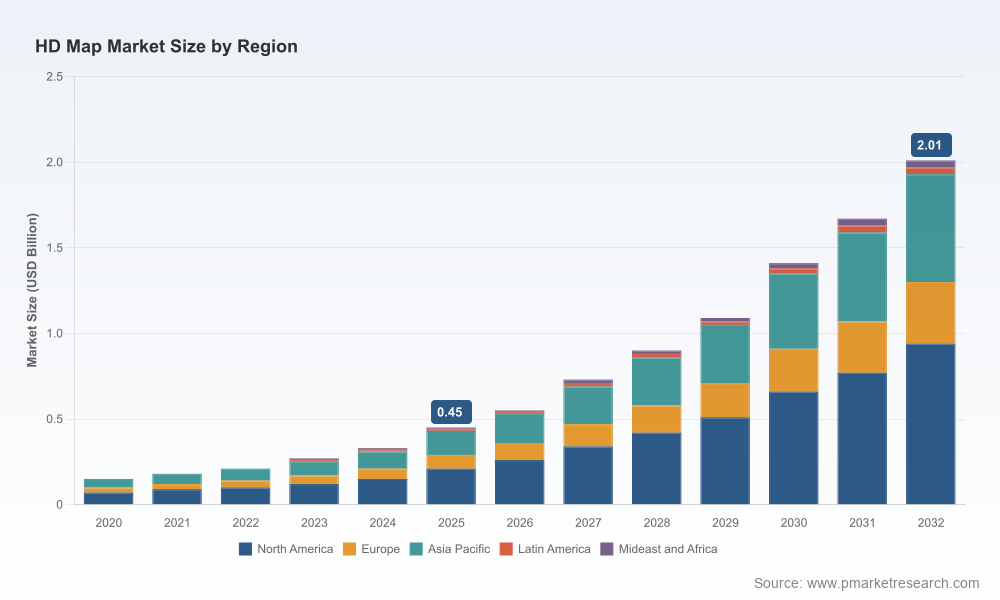

PW Consulting’s latest HD Map Market report (base year 2025) offers a forward-looking, decision-grade synthesis for executives planning capital deployment, partnerships, and product roadmaps in 2026. At a high level, the market has moved from niche proof-of-concept deployments toward a commercially scalable segment—growing from the low hundreds of millions in 2020 to an estimated USD 0.45 Billion in 2025, and forecast to expand at a compound annual growth rate (CAGR) of approximately 21.7% through our 2026–2032 horizon, reaching just over USD 2.0 Billion by 2032. This expansion is not linear: it is punctuated by technology inflection points, regulatory milestones, and infrastructure bottlenecks that will determine winners and losers over the next 18–36 months.

HD Map Market

Prioritization under uncertainty — The HD map landscape is capital- and labor-intensive. Our report translates macro growth assumptions into tactical “do now / defer / partner” recommendations for OEMs, Tier-1 suppliers, fleet operators, and software platforms so that limited R&D and procurement dollars are allocated to initiatives that create optionality rather than stranded capacity.

HD Map Market

Regulatory foresight — HD maps are evolving from convenience features to compliance enablers for Intelligent Speed Assistance (ISA) and other safety regulations, and they increasingly underpin Operating Design Domains (ODDs) for SAE Level 2–4 activations. The report maps regulatory trajectories to product certification paths so product and regulatory affairs teams can sequence effort efficiently in 2026.

HD Map Market

Ecosystem orchestration — The report decodes how data partnerships, sensor fleets (MMS), cloud services, and edge-software tie together into commercially viable stacks. It gives procurement and alliance teams the negotiating language to secure long-term value from data licensing, co-mapping agreements, and joint validation programs.

Vehicle automation adoption & feature mix — The prevalence of advanced driver assistance and incremental automation features continues to increase demand for centimeter-level positional context and lane-level semantics. That demand powerfully amplifies recurring revenue potential for map providers, especially where updates and telemetry are monetized as services.

Regulatory mandates and safety systems — Policymakers in multiple jurisdictions are embedding map-backed functionalities into compliance frameworks. Accurate speed limit data and precise lane definitions are now inputs into both vehicle safety systems and certification dossiers, accelerating procurement cycles for validated HD map data.

Hardware and data-collection economics — The production of HD maps relies on specialized mobile mapping systems equipped with LiDAR, camera arrays, and GNSS‑RTK, and the availability and cost of this equipment influences where and how quickly coverage can scale. In parallel, choices between manual labeling and machine learning-driven automation materially affect margin profiles for map producers.

Software-defined vehicle initiatives — OEMs are repositioning their roadmaps toward software-defined vehicle architectures. Live, updatable HD maps are being integrated into those architectures as a foundational capability for navigation, e‑horizon services, and remote feature delivery.

Executive dashboards: consolidated market sizing, CAGR scenarios, and revenue curves for strategic planning (base year 2025). These dashboards are engineered for board-level briefings and investment committee memos.

Practical playbooks: specific guidance on commercial models (OEM licensing, subscription, data-exchange frameworks), vendor selection criteria, and integration blueprints for in-car stacks and cloud-native pipelines.

Procurement templates: sample RFx language, SLAs for map update cadence and accuracy, and KPI suggestions for mapping quality, latency, and coverage verification.

Validation & safety annex: recommended test matrices to demonstrate map-based feature performance across ODDs, plus traceability controls for regulatory submissions.

Investment and M&A signals: a checklist of technological and commercial milestones that should trigger acquisition, minority investment, or strategic JV conversations in 2026.

The market exhibits a mix of global platform players, automotive-focused specialists, and nimble mapping firms. PW Consulting’s competitive deep-dive highlights three profiles that exemplify distinct strategic approaches:

HERE Technologies (Eindhoven, Netherlands; https://www.here.com) — A long-established platform player offering a live HD map product suite focused on high-precision tiles and layered services for ADAS and automated driving across passenger and commercial use cases. HERE continues to invest in AI-enabled live map capabilities and software-defined vehicle integrations, reflecting a platform-plus-services strategy that aims to capture recurring telemetry and update revenues.

Dynamic Map Platform (DMP) (Livonia, Michigan, USA; https://dmp-maps.com) — An automotive-focused provider emphasizing absolute positional accuracy and broad regional coverage with specialized software for e‑Horizon and ODD support. DMP’s recent coverage expansions underscore an execution focus on deterministic accuracy and class-tiered road coverage that appeals to OEM safety programs and commercial fleet integrations.

Mapbox (San Francisco, California, USA; https://www.mapbox.com) — A cloud-native map and navigation company that has extended into HD capabilities with lane-level features and in-vehicle integrations. Strategic partnerships with OEMs and integrators demonstrate a channel-led approach to embedding HD map features within consumer and fleet vehicles.

Recent strategic moves (product launches and coverage expansions in 2025–early 2026) indicate an acceleration of commercialization activities: platform-level AI live maps, coast-to-coast coverage completions, and new OEM integrations are already reshaping procurement conversations. PW Consulting evaluates these moves in the report and provides negotiation playbooks tailored to counterparty strengths.

Labor and automation trade-offs — High-definition map production is resource-intensive. Firms face a choice: invest in large labeling teams or higher-performance compute for ML-driven pipelines. Our scenario analysis quantifies break-even points and recommends hybrid operating models that balance accuracy, update cadence, and unit economics.

Equipment and supply-chain exposure — The need for professional MMS vehicles and high-end sensing kits creates single-point dependencies on suppliers based in advanced economies. The report contains mitigation strategies, including pooling mechanisms, rental fleets, and regional sourcing playbooks to reduce capital intensity.

Regulatory and safety dependencies — As HD maps transition into the compliance layer for many vehicle safety functions, map providers must demonstrate auditable quality controls and alignment with evolving standards. Our regulatory roadmap aligns anticipated policy timelines with product certification gates to minimize go-to-market friction.

Market concentration and partner selection — Competition is neither atomistic nor monopolistic; a handful of platform and specialist players are shaping market norms. The report offers a framework to assess when to partner with, buy from, or build capabilities in-house, including counterparty risk matrices and contingency playbooks.

Consolidation scenario — If platform players continue to bundle HD maps with broader vehicle services and enforce tight API/contract terms, OEMs should accelerate strategic partnerships or consider equity stakes to secure supply continuity and favorable commercial terms.

Open-standards proliferation — Should industry consortia accelerate open data standards and tooling for HD map interchange, software vendors and fleet operators gain leverage to diversify suppliers; procurement teams should prepare modular integration architectures and insist on interoperable data formats.

Coverage-as-differentiator — For services where local high-fidelity coverage materially affects feature enablement (e.g., urban robo-taxi corridors), players should prioritize micro-investments in targeted MMS campaigns and co-funded mapping initiatives to rapidly close capability gaps.

Define a two-tier supplier strategy: core provider for validated, regulation-grade layers and a secondary quick-update partner for near-real-time event capture.

Insist on auditable SLAs tied to update cadence, positional accuracy metrics, and rollback processes. Sample SLA language and acceptance tests are included in the report.

Structure commercial agreements with optionality: start with pilot volumes, include uplift clauses linked to commercial deployment milestones, and preserve escape clauses if coverage or accuracy thresholds are not met.

Invest in cross-functional validation labs combining mapping, perception, and safety engineering to accelerate integration and shorten time-to-certification.

PW Consulting’s HD Map Market study synthesizes primary interviews across OEMs, Tier‑1s, mapping firms, and regulatory experts, combined with a bottom-up model of installed vehicle fleets, feature adoption curves, and recurring revenue models. Historical calibration spans 2020–2025 with forecasts from 2026 through 2032. The body of the report includes granular regional and application segment analysis, vendor share matrices, and financial scenarios—intentionally withheld in this preview to preserve the report’s role as the single source of truth for procurement and strategic decisions.

For executives preparing 2026 budgets, partnership pipelines, or M&A playbooks, the detailed annexes and tactical templates in PW Consulting’s full HD Map Market report provide the work-ready artifacts required to move from strategy to execution. Contact PW Consulting to obtain the complete report and the dataset behind the forecasts so your 2026 roadmap is aligned with verified market and technology signals.

For detailed analysis of this topic, please visit the official page:HD Map Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com