Agricultural Liquid Fertilizers Guide

Other |

2026-04-14 09:59:06

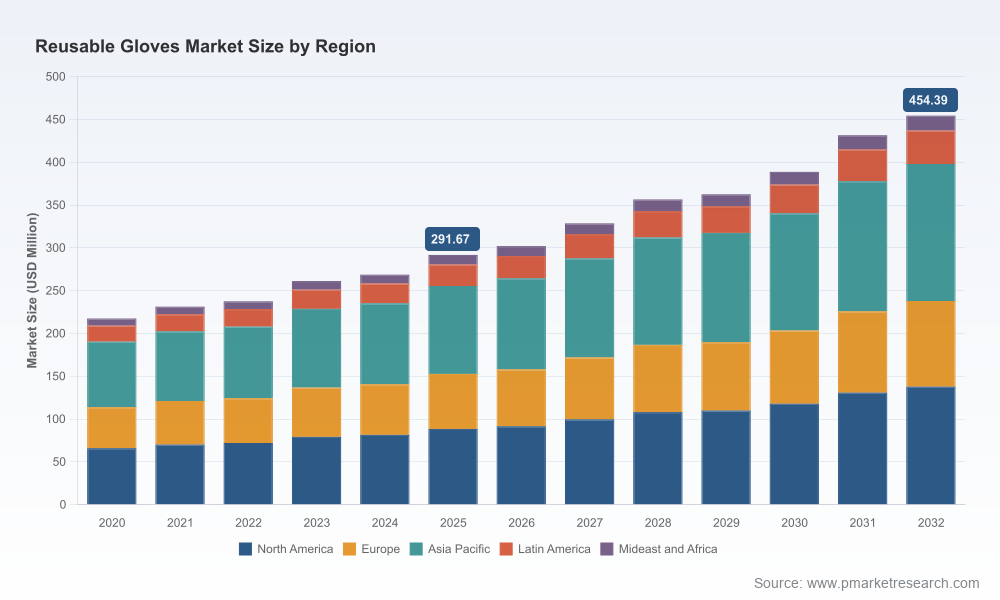

PW Consulting’s latest market study on the Reusable Gloves Market provides a focused, decision-ready intelligence package for executives planning for 2026 and beyond. Drawing on a five‑year historical baseline (2020–2025) and a detailed forecast window (2026–2032), the report quantifies a clear recovery and acceleration pattern: the market expanded from its 2020 footing and reached an estimated USD 291.67 Million in the 2025 base year, and under a central case we model a compound annual growth rate (CAGR) of 6.5% through 2032, reaching approximately USD 454.39 Million by the end of the forecast period. These headline metrics underpin the practical guidance in the study and frame the strategic pathways available to manufacturers, healthcare systems, distributors and private equity investors.

Reusable Gloves Market

Validation of momentum: The reusable glove category has moved beyond pandemic-driven volatility into a sustained growth phase. The combined influence of cost-per-use economics, tighter medical device regulation, and institutional sustainability targets is reshaping total addressable demand.

Reusable Gloves Market

Actionable timing: The report’s 2026-oriented scenario planning isolates immediate tactical moves (procurement pilots, certification roadmaps, channel expansion) from medium-term structural plays (manufacturing scale, service offerings such as laundering/sterilization and take-back programs).

Reusable Gloves Market

Risk calibration: With market concentration metrics that indicate a moderately fragmented supplier base—our CR3 stands at 28.5% and CR5 at 33.2%—there are windows of opportunity for both incumbent leapfrogging and targeted consolidation. The study shows where scale matters and where specialized capabilities can command premium margins.

Executive dashboard: One‑page scorecards for quick boardroom briefings—market size trajectory, high‑impact regulatory changes, and near-term demand levers.

Historical sizing and forward forecasting (2026–2032): Granular, model-driven revenue curves, sensitivity tables tied to input cost (raw material, energy, labor) and adoption rates for reusable programs.

Regulatory and standards playbook: Step‑by‑step implications of the latest compliance landscape for manufacturers and procurement (including recent changes to medical device quality frameworks).

Total cost of ownership (TCO) models: Pre‑built, customizable templates that quantify per‑use cost versus disposables—factoring in procurement, replacement cycles, laundering/sterilization, labor impact, and waste handling.

Procurement & operations toolkit: Vendor selection templates, KPIs for reusable glove programs, operating protocols for sterilization partners, and pilot design outlines.

Go‑to‑market and product development roadmaps: Positioning matrices for material technologies (e.g., nitrile vs. latex vs. specialty elastomers), service bundling strategies, and pricing frameworks for bundled O&M offerings.

Competitive intelligence and M&A readiness: Standardized one‑page competitor profiles, valuation playbooks, and integration risk checklists for acquirers and strategic partners.

Scenario & stress tests: Three strategic scenarios (base, upside, downside) reflecting variations in material costs, labor availability for decontamination services, and regulatory tightening, with explicit trigger points for each recommended action.

Regulatory tightening: A major shift in the medical device quality regime became effective in early 2026, requiring alignment with international manufacturing quality standards. For medical‑grade reusable gloves, this raises the bar for manufacturers to validate sterile processing and quality management systems—changing both capex needs and time‑to‑market calculations.

Unit economics vs. operational cost: Evidence from sector studies and occupational safety authorities shows material-level economics favor reusable products—reusable nitrile variants, for example, typically demonstrate lower cost per use versus disposable equivalents. However, implementing reusable programs requires new operational investments: laundering, re‑sterilization, and logistics add approximately 10–15% to operational labor costs in hospital settings, necessitating rigorous TCO modelling to preserve the expected savings.

Procurement incentives: Institutions that pilot reusable glove programs report significant annual savings on hand protection costs; these realized savings are prompting procurement teams to re-evaluate long-standing disposable‑first policies and to demand supplier partnerships that include service level guarantees.

Standards and infection control compliance: Reusable medical gloves must meet established ASTM and EN standards for permeation and dexterity. Achieving certification—alongside ISO-aligned quality systems—has become a commercial differentiator and a barrier to entry for smaller suppliers.

Value chain externalities: Environmental and waste‑management pressures now play into purchasing decisions. Suppliers that can demonstrate lower life‑cycle environmental footprints and offer closed‑loop services have a pricing advantage in public tenders and private health systems with ESG mandates.

The market is populated by a mix of global incumbents and specialized regional players. Leading manufacturers bring complementary strengths—material science, industrial safety credentials and medical‑grade product lines—while regional specialists excel at customization and regulatory navigation in their home markets. Notable examples profiled in the report include established multinationals with diversified PPE portfolios and smaller firms focused on specific material technologies or service propositions.

Manufacturers with integrated R&D and certification pipelines are best positioned to meet the new quality regime and to launch premium, compliance‑aligned products.

Industrial safety players that combine product distribution with training and after‑sales services can capture margin through services and reduce buyer switching costs.

Smaller, agile firms can win share by targeting niche clinical or industrial applications (e.g., chemotherapy handling, high‑chemical‑exposure environments) where performance and specialty testing command price premiums.

Recent market events underscore these trends: a number of manufacturers introduced advanced medical and chemotherapy‑grade nitrile products during 2025, and several new product launches emphasize protein content, powder‑free formulations and drug permeation resistance—each a response to clinical and regulatory demand signals. Collectively these moves create near‑term differentiation opportunities but also raise compliance-related entry costs for new entrants.

For manufacturers: Prioritize ISO‑aligned quality system upgrades and targeted certification investments for medical lines; deploy modular manufacturing capacity to hedge against raw material volatility and to accelerate specialty product launches.

For distributors and channel partners: Bundle product with services (e.g., inventory management, sterilization partnerships) and develop outcome‑based contracting options to capture long procurement cycles from large healthcare systems.

For hospital procurement: Implement pilot programs with full TCO tracking; negotiate supplier SLAs that allocate reprocessing and sterilization risk; and require third‑party certification evidence aligned to ASTM/EN standards.

For investors: Target tuck‑ins that offer value‑added services (laundering, certification consultancy) or intellectual property in advanced materials—these assets materially reduce execution risk for scale plays.

In keeping with our “trailer” principle—demonstrating rigour while reserving the full signal for subscribers—we have not disclosed detailed segment shares or dollar values by region, type, or application in this press release. The full report contains the complete segmentation tables, market share breakouts, and the raw model files that underpin our forecasts. This approach allows stakeholders to validate assumptions directly and to run bespoke sensitivity analyses relevant to their portfolios.

Start internal TCO pilots now: Use the high‑level findings to assemble cross‑functional teams (procurement, clinical, facilities) and pilot a controlled reusable glove program in 2026.

Map compliance gaps: Initiate supplier questionnaires aligned to ISO 13485 and ASTM/EN test protocols to identify which suppliers will require remediation investment to remain eligible for medical tenders post‑2026.

Evaluate partnerships: Identify sterilization and logistics partners for outsourced models; consider shared investments to reduce unit economics for hospital networks.

PW Consulting’s full Reusable Gloves Market report provides the data tables, company profiles, supplier scorecards, and downloadable models needed to move from planning to implementation. For procurement teams, manufacturers and investors aiming to set strategic priorities in 2026, the study offers a single, integrated source of truth—validated forecasts, compliance roadmaps and commercial playbooks. To access the complete report, datasets and annexes, visit PW Consulting’s market intelligence portal and download the full study.

For detailed analysis of this topic, please visit the official page:Reusable Gloves Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com