Multi-Mode Blue Laser Diode Market: Strategic Imperatives for 2026 — PW Consulting Market Brief

Executive summary

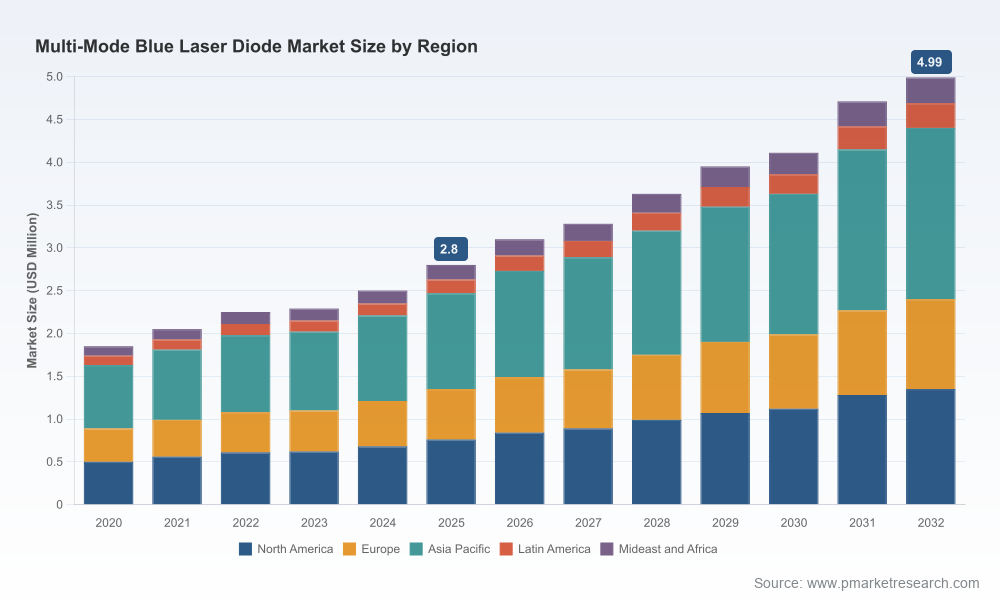

The multi-mode blue laser diode market is entering a decisive growth phase. Our PW Consulting analysis shows the market expanding from USD 1.85 Million in 2020 to USD 2.8 Million in 2025, and we forecast continued momentum through 2032 to reach USD 4.99 Million at a compound annual growth rate (CAGR) of 8.6% for the 2026–2032 period. For executives making capital-allocation, product-development, and M&A decisions in 2026, this report synthesizes macro trajectories, supplier dynamics, technology inflection points, and actionable go-to-market playbooks to convert market opportunity into sustainable advantage.

Multi-Mode Blue Laser Diode Market

Why this matters for 2026 decision-making

- Timing of investment: With a clear acceleration window beginning in the mid-2020s, firms that commit to targeted capacity expansion, thermal-management R&D, or strategic partnerships in 2026 will gain first-mover cost and integration advantages.

- Technology-driven differentiation: The transition to higher-power multi-die GaN-based architectures and improvements in beam quality are reshaping value capture across industrial, projection, and specialty markets. Product roadmaps initiated in 2026 will determine whether companies participate in premium segments or remain commodity suppliers.

- Fragmented supplier landscape: Market concentration is relatively low — the top firms do not dominate the industry outright — creating room for consolidation, selective alliances, and vertical integration. Strategic M&A or partnership activity launched in 2026 can materially improve share and scale economics heading into the 2030s.

What our analysis reveals (without spoiling proprietary splits)

The report combines quantitative trend modeling with primary supplier interviews and engineering assessments to provide three layers of insight: macro sizing and a 2020–2032 forecast; technology and end-market dynamics; and a practical playbook for operators and investors. We deliberately avoid publishing sensitive application- or region-level breakdowns in this executive summary; instead, we highlight directional implications that matter for strategy.

Multi-Mode Blue Laser Diode Market

- Growth drivers: Adoption in industrial machining and projection systems, an uptick in automotive sensing and illumination, and specialized medical and defense applications are driving demand. These drivers interact with technology shifts—particularly multi-die and packaging innovations—that increase effective power density per module.

- Cost and supply levers: The largest near-term levers are improvements in thermal design, higher-yield manufacturing processes for GaN substrates and facets, and optimized supply agreements for critical components. Improvements in these areas can materially bend unit economics in favor of suppliers prepared to invest.

- Revenue trajectory: The market’s path from USD 1.85 Million in 2020 to USD 2.8 Million in 2025, and onward to an estimated USD 4.99 Million by 2032 (CAGR 8.6% for the forecast period) creates windows for different strategic plays depending on tolerance for capital intensity and speed to market.

Competitive landscape: who matters and why

The competitive field blends legacy optoelectronics manufacturers, specialized laser houses, and conglomerates pursuing adjacent optics capabilities. Our report profiles leading firms and benchmarks them across technology, scale, channel access, and route-to-market.

Multi-Mode Blue Laser Diode Market

- Nichia Corporation (Tokushima, Japan): A recognized leader in GaN-based blue laser technology, Nichia’s strengths are R&D depth and a pipeline of high-reliability devices for high-power modules. Strategy implication: incumbency in GaN IP positions Nichia to monetize through licensing and premium OEM partnerships.

- ams-OSRAM AG (Premstaetten, Austria): The company has signaled a move toward higher-power multi-die solutions; in September 2025 it introduced a multi-die edge-emitting device delivering 42 W optical output at 455 nm from its Vegalas Power series. Strategy implication: aggressive product premiumization by established optoelectronics suppliers is compressing the performance threshold for commodity vendors.

- Sony Corporation and Sharp Corporation (Japan): Both emphasize integration into consumer and projection ecosystems. Strategy implication: their depth in system-level design and channel relationships makes them natural partners for integrators targeting consumer-grade projection and display applications.

- ROHM, Panasonic (Japan): Broad semiconductor portfolios and diversified end-market access make these firms strategic suppliers for automotive and medical markets where qualification cycles are longer but margins can be higher.

- Coherent, IPG Photonics, TRUMPF (USA/Germany): These laser-specialist companies compete on system integration and high-power industrial modules. Strategy implication: for applications requiring turnkey systems (welding, additive manufacturing), system suppliers capture disproportionate value over bare-die vendors.

Strategic plays for 2026

The following plays are designed to be immediately actionable in 2026 and are grounded in our modeling and supplier assessments:

- Selective capacity expansion with process control: Expand capacity only in facilities implementing yield-improving process controls (facet protection, epitaxy uniformity). Uncapped capacity expansion risks margin erosion in a fragmented market.

- Vertical capture through modules and optics: Move up the stack by offering pre-aligned modules and optical subsystems rather than raw diodes. This reduces commoditization risk and increases switching costs for OEM customers.

- Strategic partnerships for thermal management: Prioritize alliances with materials and thermal-solution providers. Thermal efficiency improvements unlock higher wattage operation and permit new use cases in compact consumer and automotive systems.

- Targeted M&A and bolt-on acquisitions: Given the low-to-moderate market concentration, bolt-on acquisitions of niche suppliers (optical packaging, beam-shaping components) can be accretive and defensible, especially if executed in 2026 ahead of competitors.

- Qualification-first go-to-market for regulated verticals: For automotive and medical segments, initiate qualification programs in 2026; long lead times require early engagement even if near-term revenue is modest.

Risk scenarios and mitigation

Our scenario analysis models three pathways for 2026–2032: base case (CAGR ~8.6%), accelerated adoption, and downside stress (supply-chain shocks or slower-than-expected end-market uptake). Key mitigants include diversified supplier contracts, staged capital expenditure tied to yield milestones, and adaptable product platforms that allow rapid customization for different use cases.

- Supply risk: Concentration in substrate and epitaxy suppliers can create single-point failures. Mitigation: dual-sourcing strategies and selective inventory hedging.

- Technology obsolescence: Rapid advances in packaging and beam-shaping could leave legacy products uncompetitive. Mitigation: ring-fence R&D spend for modular upgrades and maintain a roadmap that supports backward compatibility.

- Customer concentration: Heavy dependence on a small set of OEMs increases negotiating pressure. Mitigation: develop service and module offerings that increase stickiness and enable premium pricing.

What the full PW Consulting report delivers

This market brief is an entrée to a comprehensive research package tailored for executive and investor action. The full report includes:

- Complete 2020–2032 quantitative model with scenario variants and sensitivity analysis.

- Supplier scorecards, capability matrices, and a detailed competitive benchmarking framework.

- Practical playbooks: M&A diligence checklist, OEM engagement templates, go-to-market timelines, and a commercial negotiation guide for long-term supply contracts.

- Operational tools: unit-economics models, thermal and yield improvement breakeven calculators, and integration checklists for module assembly.

- Investment heatmaps identifying where to prioritize capital outlays by technology and use case over the 2026–2028 window.

How to use this intelligence in 2026

Executives should treat 2026 as the hinge year: adopt a “test-and-scale” approach by executing limited-capacity expansions tied to yield thresholds, formalizing strategic supplier partnerships, and initiating selective qualification programs for high-value verticals. Investors and corporate development teams should prioritize targets that offer modularity in systems, IP control in GaN epitaxy or packaging, and route-to-market access in projection and industrial segments.

Conclusion — an invitation to deeper intelligence

The multi-mode blue laser diode market presents a clear, quantifiable growth path and a diverse strategic landscape. The underlying numbers show steady expansion, and the technical and commercial levers available to participants mean that well-timed, focused actions in 2026 can produce disproportionate returns. PW Consulting’s full market study supplies the granular models, supplier assessments, and executable playbooks that boards and executive teams need to move from intent to outcome.

To access the full dataset, proprietary segmentation, and the operational playbooks referenced here, please visit the PW Consulting report page for the Multi-Mode Blue Laser Diode Market. Our team is available for bespoke briefings and scenario workshops tailored to your organization’s strategic priorities for 2026.

For detailed analysis of this topic, please visit the official page:Multi-Mode Blue Laser Diode Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com