United States Game Testing Services Market by 2031 — Analysis & Industry Overview

Other |

2026-03-31 13:51:41

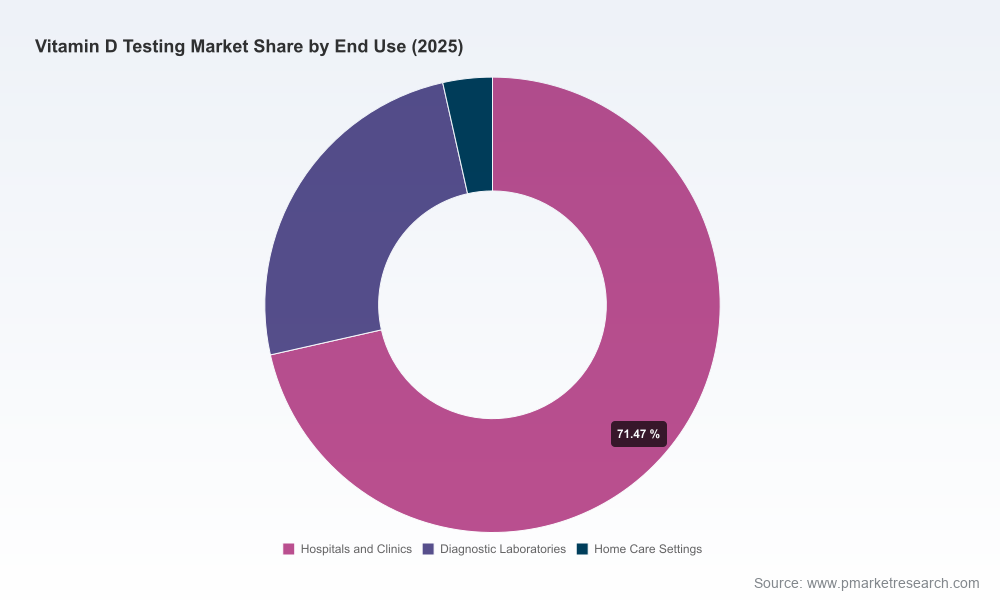

PW Consulting’s latest Vitamin D Testing Market report (base year 2025; historical review 2020–2025; forecast period 2026–2032) delivers a practical, decision-focused intelligence package for executives planning moves in 2026. The underlying market is sizable and accelerating: global revenue grew from approximately USD 822 million in 2020 to USD 1,149.5 million in 2025, and is projected to reach roughly USD 1,985.5 million by 2032—a compound annual growth rate (CAGR) of 8.15%. These macro figures frame a market with robust demand drivers, meaningful room for innovation, and clear strategic inflection points for manufacturers, laboratories, and payers alike.

Vitamin D Testing Market

The headline metrics above reflect sustained growth driven by expanding preventive screening, rising clinician and consumer awareness of vitamin D’s role in chronic disease management, and technology-driven reductions in per-test cost. The market exhibits moderate concentration: the top three firms account for just under half of global sales (CR3 ~47.5%), and the top five drive nearly 59% (CR5 ~58.9%).

Vitamin D Testing Market

PW Consulting’s report contains fine-grained regional, modality and end-use splits, competitive share tables and price-point matrices. In keeping with our “trailer” approach, this public summary deliberately does not disclose the proprietary segmented figures. Those datasets, plus modelled scenario outputs and supplier-level P&L sensitivity analyses, are available in the full report and through our client portal.

Vitamin D Testing Market

Our research is designed for immediate operational use by commercial, clinical and corporate development teams. Key deliverables include:

The Vitamin D testing ecosystem is a mix of large diagnostic conglomerates, instrument manufacturers and niche reagent/kit specialists. Below are practical takeaways on core incumbents covered in the report and the tactical actions we recommend for 2026.

Roche’s strengths include broad laboratory automation integration and established laboratory relationships. A notable recent development: in September 2025, the FDA/CLIA pathway recognized Roche’s Ionify 25-Hydroxy Vitamin D total assay as Moderate Complexity—the first mass spectrometry-based total 25-OH D system to receive this designation—expanding access to a wider swath of clinical laboratories. Strategic implication: players must reassess MS as a mainstream platform rather than a niche specialty offering. For rivals, recommended responses include accelerated interoperability partnerships, and for labs, piloting moderate-complexity MS workflows to retain testing volume in-network.

Known for immunoassay-based offerings optimized for automated analyzers, DiaSorin’s global footprint and established assay kits make it a reliable incumbent for high-throughput environments. We advise commercial teams to emphasize value-adds—turnaround time, standardization programs, and bundled QC solutions—to defend share against MS entrants.

Abbott’s large installed base and broad diagnostic platform give it distribution scale. In 2026, its competitive play will likely combine system-level integration with loyalty programs for hospital networks. Competitors should prepare targeted key-account strategies that highlight assay differentiation and total cost of ownership.

Siemens’ large institutional presence positions it to defend hospital lab channels. We recommend evaluating bundled service contracts and instrument-placement economics when negotiating with multi-hospital systems.

Beckman’s clinical chemistry and immunoassay capabilities make it a core vendor for mid-to-large labs. Its strategic focus should be on assay standardization and post-market support—a key decision criterion for procurement teams.

As a principal supplier of LC-MS instrumentation and laboratory consumables, Thermo Fisher plays a critical enabling role as MS becomes more accessible. Lab leaders evaluating MS adoption should include Thermo Fisher in vendor selection and total-cost-of-ownership analyses.

Quidel’s competence in rapid diagnostics and POC devices positions it to capture demand where convenience and speed trump laboratory throughput. For POC market entrants, Quidel represents both competitive pressure and potential co-development partner.

Bio‑Rad’s strengths in QC products and niche assays make it an attractive partner for labs focused on quality assurance and assay harmonization. Vendors should evaluate joint go-to-market opportunities around standardization programs.

Strategic implication: commercial teams must build payer playbooks now—mapping the differences among active LCDs, updating laboratory claim-edit engines, and creating clinician-facing ordering guidance to preserve test volumes and revenue in 2026.

If your 2026 plan includes new product launches, channel expansion, payer negotiations, or M&A, PW Consulting’s Vitamin D Testing Market report will shorten your path to value. The full report provides the proprietary segment-level datasets, vendor-by-vendor market shares, pricing ladders, and executable templates referenced in this summary.

Contact PW Consulting to schedule a briefing where we will: walk you through scenario implications for your specific portfolio, adapt our payer playbook to your commercial footprint, and identify the 90‑day experiments that will de-risk your 2026 investments. The briefing is the fastest way to turn the market-level insights presented here into board-ready investment decisions.

For detailed analysis of this topic, please visit the official page:Vitamin D Testing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com