Plastic Drums Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-04 06:08:58

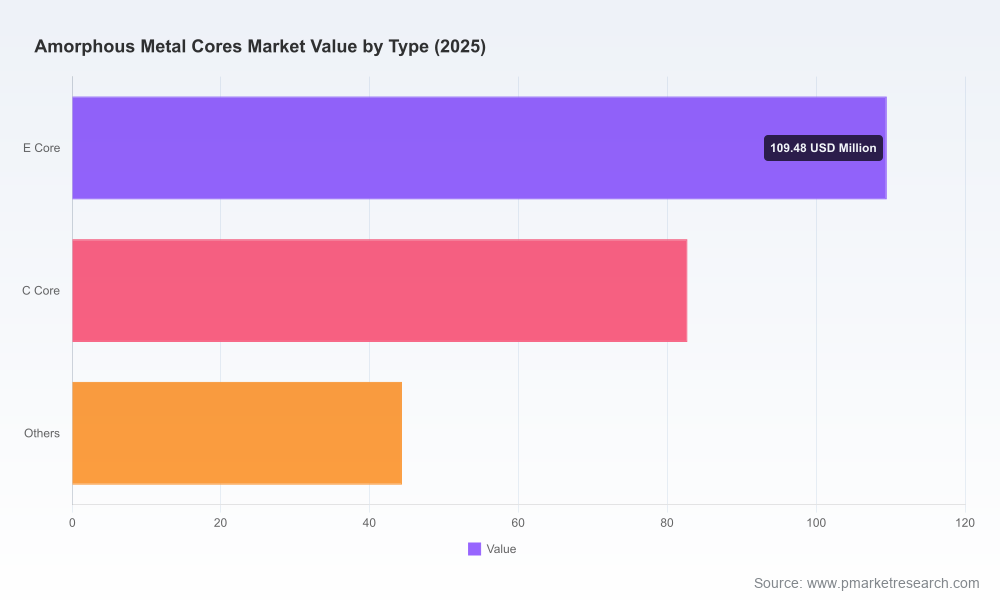

PW Consulting’s new market intelligence on the Amorphous Metal Cores market positions industry leaders and strategic investors to act decisively in 2026. Built on a rigorous historical analysis (2020–2025, base year 2025) and forward-looking modeling through 2032 (forecast period 2026–2032), the report quantifies a robust market expansion driven by energy-efficiency imperatives, electrification trends, and product innovation. The global market, measured in USD Million, grew from the low hundreds in 2020 to an estimated USD 236.5 Million in 2025 and is forecast to reach approximately USD 385.6 Million by 2032 — a compound annual growth rate (CAGR) of 7.5% over the forecast window.

Amorphous Metal Cores Market

Energy policy and efficiency targets are accelerating demand for low-loss magnetic cores. Decision-makers who lock in supply arrangements and technology roadmaps now can capture efficiency-driven premium demand across utility transformers, power electronics and traction systems.

Amorphous Metal Cores Market

Supply-side investments and regional capacity rebalancing — including large greenfield announcements — are altering cost curves and access to advanced ribbon materials. Strategic timing of capital expenditure, long-term contracts, and offtake partnerships will materially influence gross margins in 2026–2028.

Amorphous Metal Cores Market

Product differentiation is migrating from “commodity” magnetic materials to system-level efficiency and reliability gains (e.g., no-load loss reduction, high-frequency performance). Firms that combine metallurgical capabilities with application engineering will outpace purely volume-driven competitors.

The report is designed as a practical playbook for management teams and investors. At a glance, the deliverables include:

Market sizing and growth modeling (historical 2020–2025; forecast 2026–2032) with scenario alternatives tied to policy, electrification, and raw-material volatility.

Commercial segmentation and demand-side analysis (by product types, applications and regions), with structural demand drivers and adoption curves.

Supply-chain mapping and cost-stack analysis highlighting manufacturing throughput constraints, ribbon production economics, and key input sensitivities.

Competitive landscaping and capability benchmarking of the principal producers, including strategic profiles, plant footprints, capacity plans, and recent transactions/announcements.

Technology outlook and product roadmaps covering amorphous vs. nanocrystalline alloys, Co- and Fe-based variants, saturation and frequency performance metrics, and R&D trajectories.

Commercial strategies: pricing frameworks, tender playbooks for utilities and OEMs, channel and aftermarket approaches, and recommended partnership structures.

M&A and capital allocation guidance, with accretion/dilution modeling for acquisitive growth versus organic scale-up.

The Amorphous Metal Cores market sits at the intersection of policy-driven efficiency programs and the electrification of energy end-uses. Two dynamics deserve special emphasis for 2026 planning:

Efficiency Mandates and Asset Replacement Cycles — Regulatory pressure to reduce distribution transformer losses, combined with the economics of lifecycle cost evaluation, is extending the addressable market beyond premium retrofit projects into mainstream procurement.

Technology Differentiation — Advances in alloy chemistry and ribbon processing are enabling step-changes in no-load loss and performance at high frequencies. These technical advantages are being translated into system-level value (reduced operational losses, lower cooling burdens, and smaller form factors for power electronics), shifting procurement criteria from first-cost to total-cost-of-ownership.

Operationally, these trends mean procurement leaders should: (a) include lifecycle loss valuation in tender specifications, (b) qualify multiple alloy suppliers to de-risk single-source exposure, and (c) collaborate early with core producers on design-for-efficiency to secure performance guarantees.

The competitive landscape remains moderately fragmented. Top-tier specialist producers play to distinct strengths — proprietary alloy families, manufacturing scale, and regional execution — while a broad base of regional suppliers competes on price and delivery agility. Notable strategic signals we highlight:

Proterial, Ltd. is a primary player with a globally recognized Metglas™ portfolio. Its asset footprint, including U.S. production and recent greenfield capacity moves, signals a deliberate push to secure regional supply and capture demand tied to energy-efficiency initiatives. The company’s material claims — including substantial reductions in no-load loss compared with electromagnetic steel sheets — make it a preferred partner for projects where lifecycle losses are monetized.

Metglas, Inc. (part of the same group) remains central to distribution-transformer applications in markets where U.S.-based manufacturing and local supply chains are strategic advantages.

VACUUMSCHMELZE GmbH & Co. KG differentiates on alloy portfolio and high-performance grades (VITROVAC®), including Co-based and Fe-based formulations with high saturation flux densities suited to pulse-compression and high-frequency applications. These materials are particularly attractive for advanced power electronics and specialty transformer use-cases.

Large Chinese manufacturers have scaled ribbon and core production aggressively, enabling competitive pricing and high-volume supply for distribution transformer programs. Their manufacturing capabilities are reshaping the global cost base and creating localized supply options in high-volume markets.

Market concentration metrics indicate a top-three share below one-third and a top-five share modestly higher — a structure that affords both competitive tension and opportunities for consolidation in value-added segments.

Capacity expansions and regionalization: Recent production-site announcements point to a rebalancing of supply closer to end demand. These investments compress lead-times and lower landed costs for forward-looking buyers who prioritize nearshoring.

Material performance claims: Suppliers are publicizing quantified gains (for example, substantial no-load loss reductions and high saturation flux densities). Buyers should require third-party validation and contractually enforce performance testing to avoid first-cost trade-offs.

Product placement into high-growth applications: High-frequency power electronics and renewable/inverter-coupled systems are emerging as higher-margin avenues for advanced amorphous and nanocrystalline materials.

Recast procurement evaluation to total cost of ownership. Embed lifetime loss valuation and quantifiable performance clauses in RFPs.

Secure multi-year supply agreements with performance milestones; prioritize suppliers with verifiable production-scale and geographic diversification to mitigate logistics and geopolitical risk.

Allocate R&D or co-development funding to material-application integration projects that translate alloy advantages into system-level savings — this creates defensible differentiation and premium pricing potential.

Build scenario-based capacity plans: evaluate whether to pursue capacity augmentation or adopt a “virtual capacity” model using strategic sourcing and tolling arrangements.

Pursue selective partnerships or bolt-on acquisitions to access proprietary alloy technology or to secure downstream manufacturing capabilities (core assembly, impregnation, and testing).

Engage with regulators and standards bodies early to shape lifecycle evaluation protocols and efficiency testing standards that reward higher-performing amorphous solutions.

This briefing samples the high-level findings. The full report provides the market model (USD Million, base year 2025), granular segmentation and demand forecasts, supplier-level capacity tables, margin and cost-stack analytics, and downloadable scenario models. It also includes detailed strategic profiles and benchmarking for the principal producers, a chronology of recent developments and press-verified sources, and contractual templates for performance-based procurement.

We deliberately preserve the most commercially sensitive cell-level data and granular regional/application breakdowns to ensure decision-makers subscribe for the full model and supporting datasets. If your 2026 strategy depends on precise regional demand, product-type economics, or supplier share tables, the full report will supply the validated inputs and downloadable Excel models your team needs to act with confidence.

Amorphous metal cores are transitioning from niche high-efficiency solutions to mainstream components in grids, power electronics and electrified transport systems. The market’s projected trajectory through 2032 — underpinned by a 7.5% CAGR from 2026 — creates both near-term commercial opportunities and strategic inflection points for manufacturers, OEMs and utilities. In 2026, the winning play combines disciplined procurement, selective vertical integration, and co-development of application-specific material solutions. PW Consulting’s full market study equips executives with the data, scenarios and tactical playbooks to capture value across this evolving market.

For access to the full dataset, supplier scorecards, and downloadable forecast model, visit our report page or contact your PW Consulting account lead to schedule a briefing and model walkthrough.

For detailed analysis of this topic, please visit the official page:Amorphous Metal Cores Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com