Furniture Manufacturing Software Market Forecast Report

Other |

2026-06-10 12:45:05

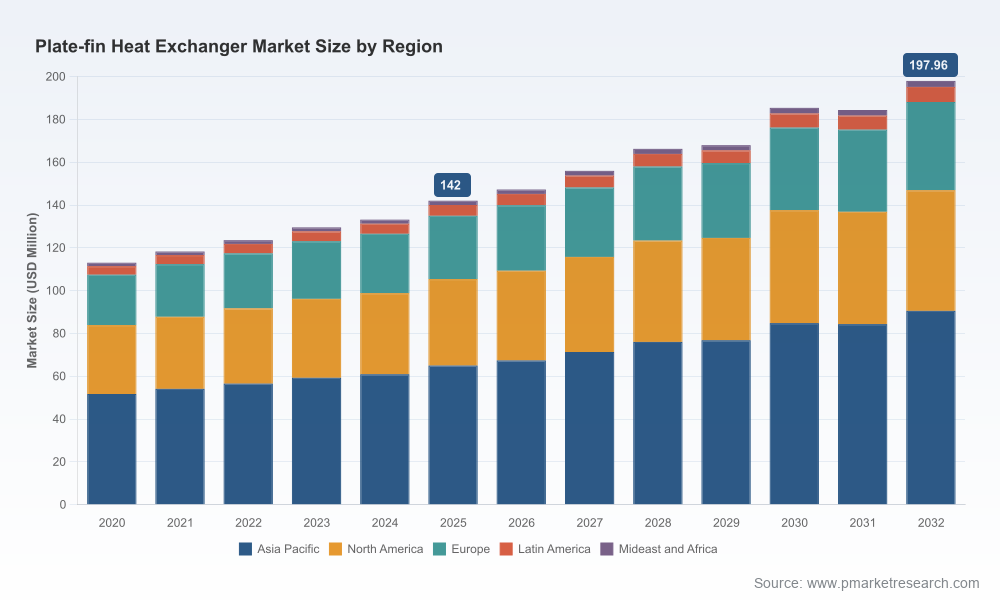

PW Consulting’s new Plate-fin Heat Exchanger Market study provides a compact, decision-focused intelligence package designed for executive teams that must convert thermal-management complexity into competitive advantage in 2026. Built on a 2025 base year and a seven-year forecast horizon (2026–2032), the report quantifies the sector’s recent trajectory — growing from a market base in 2020 to USD 142.0 Million in 2025 — and models a steady expansion through 2032 at a compound annual growth rate (CAGR) of 4.9%. Our analysis blends quantitative forecasting with practical playbooks: procurement levers, product roadmaps, compliance checklists and vendor scorecards that directly support capital allocation, sourcing and product development choices.

Plate-fin Heat Exchanger Market

The plate-fin segment has moved beyond niche engineering curiosity into a scaled, capital-intensive market with predictable, discipline-friendly growth. After a five-year historical assessment (2020–2025) that shows clear upward momentum, our forecast anticipates incremental scale across 2026–2032 as global industrial restructuring — LNG expansions, petrochemical turnaround projects, and cryogenic capacity additions — drive demand for compact, high-efficiency heat-transfer solutions. By 2032 we model a market approaching the high‑hundreds of millions (forecasting toward USD 197.96 Million), supporting a planning envelope in which mid-size and large OEMs can justify targeted investments in factory automation, localization and product modularization.

Plate-fin Heat Exchanger Market

Two points matter for 2026 decisions: first, the market’s steady CAGR (4.9%) indicates opportunity for sustained revenue capture without the volatility associated with speculative segments; second, market concentration is moderate — the top three players account for roughly 30% of market share while the top five account for about 35% — meaning suppliers are influential but there is still room for differentiated entrants and consolidation plays.

Plate-fin Heat Exchanger Market

Our competitive analysis profiles the established OEMs that set performance and quality benchmarks in plate-fin technology. Linde Engineering (Munich) stands out for its long history and scale in brazed aluminum plate‑fin deployments; Chart Energy & Chemicals brings a strong footprint in vacuum-brazed systems for cryogenic and industrial process use; Kobe Steel and Sumitomo deliver Japanese engineering depth focused on high-performance and specialty applications; Alfa Laval plays a broad role across HVAC, refrigeration and food processing with compact plate-fin designs; Eaton’s portfolio targets liquid-to-liquid and liquid-to-air thermal management with strong systems integration capabilities. Each of these players brings distinct commercialization levers — engineering pedigree, geographic reach, aftermarket networks and standards leadership — that buyers and investors must weigh differently depending on their strategic objective.

Our vendor scorecards distill these strengths into procurement-ready guidance: which suppliers are best for large-procurement cryogenic projects, which excel in rapid-turn retrofit kits, and which vendors are suitable partners for co-development of hydrogen-ready heat exchangers. The full scorecards and sourcing matrices are available in the comprehensive dataset.

Executives tell us they need three things to move decisively in 2026: clarity on demand trajectories; a short, prioritized set of actions that reduce execution risk; and vendor-level intelligence that can be operationalized in procurement and M&A. PW Consulting’s Plate-fin Heat Exchanger Market study delivers all three. We marry a transparent forecasting methodology (base year 2025, historical 2020–2025, forecast 2026–2032, CAGR 4.9%) with business-ready tools — scorecards, scenario models and compliance playbooks — so teams can act on day one while continuing to refine strategy as projects scale.

This briefing intentionally highlights the strategic contours and actionable recommendations without reproducing the granular segmentation tables and vendor scorecards that corporate planning teams require to operationalize decisions. For the full dataset, split-by-type and application analytics, downloadable vendor scorecards, and ready-to-use ROI calculators, visit the PW Consulting report page and download the complete Plate-fin Heat Exchanger Market report. The complete package includes proprietary models and an appendix mapping standards changes to engineering checklists — essential materials for any organization committing capital or changing sourcing strategies in 2026.

For detailed analysis of this topic, please visit the official page:Plate-fin Heat Exchanger Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com