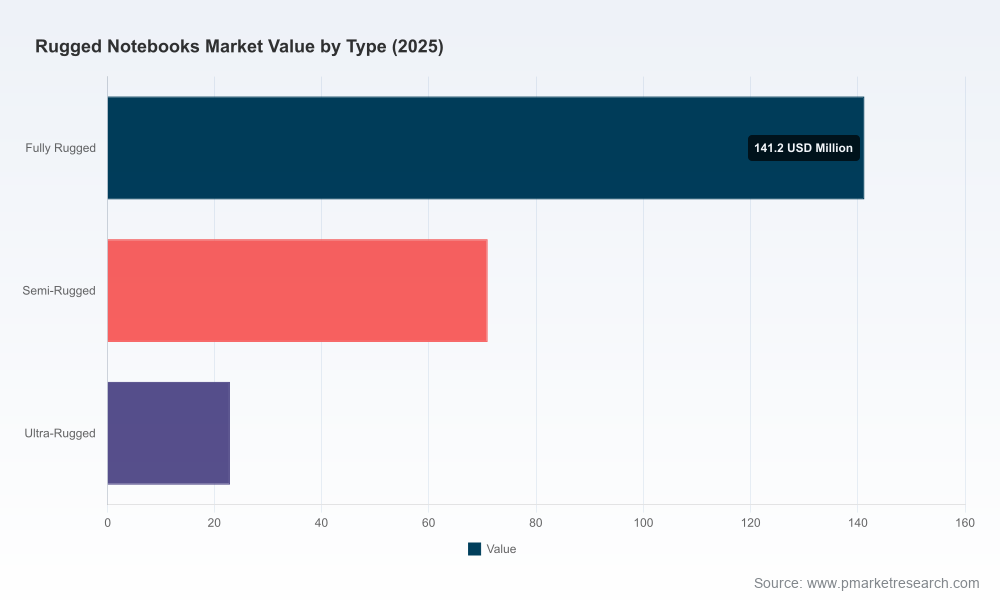

Rugged Notebooks Market 2026: Strategic Perspectives and Actionable Intelligence for Enterprise Leaders

As organizations brace for an operating environment defined by higher compute intensity at the edge, more severe deployment conditions, and accelerating regulatory scrutiny, rugged notebooks are shifting from a niche procurement item to a strategic asset. PW Consulting’s latest Rugged Notebooks Market report — built on a 2020–2025 historical base and projecting through 2032 — synthesizes market-scale trajectories, supplier strategies, technology inflection points and procurement playbooks that enterprise buyers, system integrators and OEM partners will need to act on in 2026.

Rugged Notebooks Market

Why this report matters for 2026 decision-makers

Between 2020 and 2025 the market expanded meaningfully, and our base-year view (2025) anchors a forecast that anticipates sustained growth through 2032 at a compound annual growth rate of 7.5%. In dollar terms, the sector has moved from a small-but-stable installed base into a growth phase driven by AI-ready hardware, increasingly stringent standards enforcement, and cross‑sector digitalization. For executives considering capital refreshes, long‑term supplier partnerships or new product development, the implications are twofold: tactical buying choices made today will materially affect field performance and lifecycle costs over a seven-to-ten year horizon, and vendor selection is as much about roadmap alignment (e.g., GPUs, AI accelerators, connectivity stacks) as it is about price or immediate delivery.

Rugged Notebooks Market

Report scope — practical, transaction-ready intelligence

- Market sizing and outlook: A rigorous top‑down model that traces the market’s expansion from the 2020 base period through 2025 and projects growth to 2032 under multiple macro scenarios.

- Competitive diagnostics: Detailed vendor dossiers and capability matrices (hardware platforms, certifications, software ecosystems, service footprints) with an emphasis on procurement‑relevant KPIs.

- Technology and product roadmaps: Assessment of compute trends (GPU/AI integration, ML inference at the edge), ruggedization techniques, and modular design strategies enabling field upgrades.

- Standards and regulatory tracker: Practical compliance checklists for MIL‑STD and ingress protection, ATEX options for hazardous environments, and procurement language you can insert into RFPs.

- Supply chain and risk heatmap: Component criticality analysis, lead‑time scenarios, single‑sourcing risk mitigation and inventory optimization heuristics.

- Total cost of ownership (TCO) models: Scenario calculators for CapEx vs. OpEx tradeoffs, extended‑warranty impacts, and service‑contract benchmarking.

- M&A and partnership playbook: Evaluations of consolidation drivers and a deal‑value framework for strategic acquirers and investors.

- Operational tools: Field‑deployment checklists, integration blueprints for vehicle/dock mounting, and a supplier short‑list methodology tailored to specific use cases.

We designed the report to be operational: buyers can extract RFP language, supply‑chain mitigations and a procurement scorecard within the same document that explains market dynamics and vendor strategy.

Rugged Notebooks Market

High‑level market signals and what they mean for buyers

- Growth trajectory: The market is on a steady upward path and expected to nearly double in scale from its early‑decade baseline through the forecast horizon, reflecting stronger adoption across defense, industrial automation, public safety and mobile workforces.

- Fragmentation and competitive intensity: Market concentration remains relatively low compared with mainstream PC markets — the leading vendors do not yet dominate the sector. That fragmentation creates opportunities for niche specialists and regional players to win significant share by pairing differentiated certifications, after‑sales services, or vertical integrations.

- AI at the edge is a differentiator, not a feature: Recent product announcements from leading vendors show an industry pivot. Several manufacturers are shipping systems with discrete GPUs and AI‑ready platforms targeted at field inferencing, while others promote AI‑enhanced user workflows (Copilot‑style integrations). Buyers must evaluate thermal budgets, power provisioning, and cooling strategies when specifying AI‑capable rugged units.

- Standards and procurement risk: Certifications such as MIL‑STD variants and ingress protection ratings (IP66/IP67) are increasingly table stakes in procurement — but the practical differences between certifications can materially affect lifecycle costs. Our compliance checklists are designed to prevent false equivalencies during vendor evaluation.

Competitive landscape — strategic read on core vendors

The market’s competitive map is a mix of global OEMs with broad portfolios and specialist manufacturers that leverage domain depth and certification expertise. Key strategic observations:

- Dell Technologies: Leverages scale and enterprise channel strength to push higher‑performance GPUs into rugged form factors. Dell’s approach blends mainstream enterprise manageability with rugged certification, making it attractive for organizations that prefer a single‑vendor ecosystem across office and field devices.

- Getac: Continues to push product innovation focused on MIL‑STD and enterprise durability while moving aggressively into AI‑enabled platforms. Recent launches position Getac as a bellwether for how vendors integrate purpose‑built AI compute into certified chassis without sacrificing ingress and shock resistance.

- Panasonic (Toughbook): Remains synonymous with field durability and military grade deployments. The Toughbook line’s strength is its vertical resonance with defense and first‑responder buyers who prioritize end‑to‑end ruggedness and long service commitments.

- Zebra Technologies: Plays to strengths in logistics and public safety through enterprise‑grade Android/Windows platforms and a deep peripheral ecosystem — ideal for organizations that need device fleets integrated with scanners, printers and asset‑tracking systems.

- Regional and specialist vendors (Roda, Winmate, Durabook, Xplore, RuggON): These suppliers differentiate on rapid customization, location proximity for service, or certifications for niche applications (e.g., ATEX). They are often the fastest to market with verticalized solutions but may present scale and procurement integration tradeoffs.

Recent product activity underscores divergent strategies: on the one hand, Dell’s expansion to include discrete GPUs targets data‑intensive field analytics; on the other, niche vendors continue to optimize for extreme ingress and shock requirements while introducing modular approaches that allow incremental upgrades. We analyze these strategies in the report and map them to enterprise procurement intents.

Key strategic recommendations for 2026

- Create an edge‑compute procurement framework: Standardize evaluation criteria around thermal headroom, modular upgrade paths (for AI accelerators), and manageability features, not just raw ingress or shock specs.

- Insist on lifecycle modeling in RFPs: Require vendors to provide scenario TCOs that include predictive maintenance, spare‑parts availability and service SLAs for harsh environments.

- Design for upgradeability: Where possible, favor platforms that separate compute modules from sealed chassis elements, enabling field upgrades without compromising certifications.

- Mitigate supply chain single points of failure: Maintain secondary sourcing strategies for critical components, and consider vendor consortia or pooled procurement for high‑volume deployments to secure priority allocations.

- Align pilot programs with end‑state operations: Run pilots that replicate the most extreme use cases you expect in full deployment (temperature cycling, EMI exposure, prolonged vibration), and require vendors to validate under those conditions.

What the report purposely withholds — and why

In keeping with our “trailer” approach, this article intentionally highlights market direction, vendor strategy, methodological rigor and actionable recommendations while withholding granular segment‑level datapoints and region/application‑specific breakdowns. The full report contains detailed splits by region, type and application, proprietary vendor scorecards, a contract‑grade procurement template, and downloadable TCO models. Those elements are gated to ensure confidentiality of proprietary modeling and to provide the complete context buyers need to make defensible, auditable decisions.

How to use this insight

For procurement leaders and technical buyers, the immediate use cases are:

- Shortlist vendors for 2026 refreshes using our supplier scorecard and risk model.

- Redesign RFPs to include AI‑workload validation, thermal and power constraints verification, and maintenance SLAs tied to field MTTR/KPIs.

- Structure service agreements that transfer aftermarket risk to manufacturers through guaranteed spare availability and certified repair centers.

Next steps

Enterprise leaders preparing budgets and vendor strategies for 2026 should treat rugged notebooks as a strategic asset class whose total cost and operational impact become more visible when AI, connectivity and regulatory requirements converge. PW Consulting’s full Rugged Notebooks Market report equips teams with the granular data, vendor matrices and operational tools required to make those choices with confidence.

To review the complete dataset, vendor scorecards and downloadable procurement templates referenced here, please consult the report landing page. Our team is available for bespoke briefings and to run tailored scenario workshops that map your use cases to the market’s most defensible supplier and technology strategies.

For detailed analysis of this topic, please visit the official page:Rugged Notebooks Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com