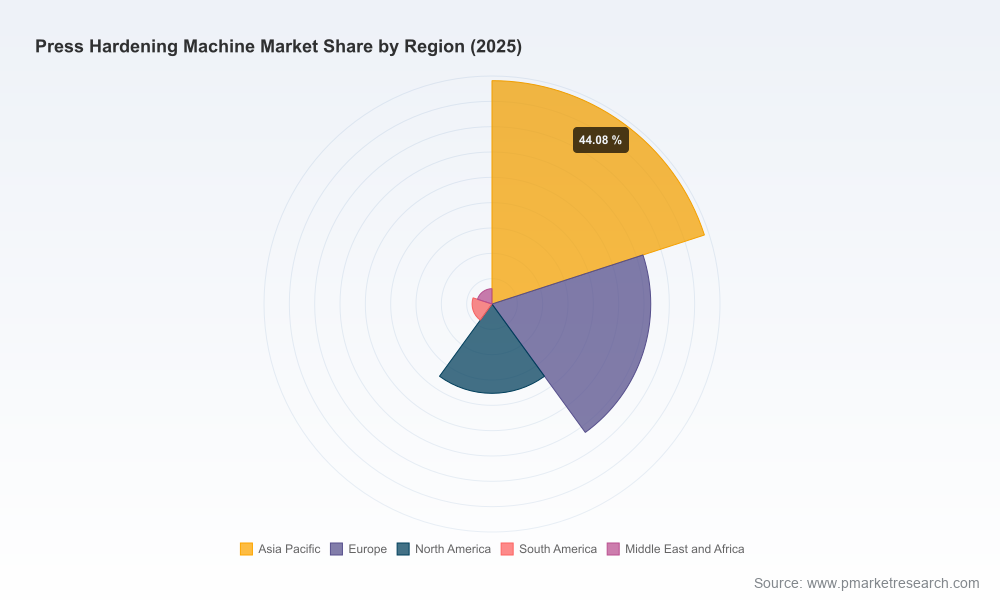

Press Hardening Machine Market — 2026 Strategic Briefing

PW Consulting today releases a strategic briefing drawn from our full Press Hardening Machine Market study (base year 2025, forecast 2026–2032). The report synthesizes rigorous quantitative forecasting with actionable playbooks and competitor intelligence designed to inform capital allocation, supplier strategy, and technology roadmaps through 2026 and beyond. At the macro level, the market is expected to grow from an estimated USD 1,021.32 Million in 2025 to approximately USD 1,102.44 Million in 2026, tracking a compound annual growth rate (CAGR) of 7.32% over the forecast window and approaching an aggregate in excess of USD 1.67 Billion by 2032. These headline figures understate the decision levers inside the report — which combine real-world cost modelling, scenario stress-tests, and supplier benchmarking to convert market forecasts into executable initiatives.

Press Hardening Machine Market

Why 2026 Is a Pivotal Year for Press Hardening Decisions

Automotive programs and adjacent industrial applications are entering a phase of consolidation where material strategy, energy economics, and manufacturing footprint decisions will lock in returns for a decade. Press hardening is no longer a niche heat-treat operation: it is central to vehicle lightweighting, crash performance, and secondary manufacturing cost. Key industry dynamics we highlight in the report:

Press Hardening Machine Market

- Performance materials: Press hardening enables ultra-high strength steels (UHSS) that reach up to roughly 2,000 MPa, making them indispensable for crash-critical structures and helping OEMs meet increasingly stringent safety and efficiency mandates.

- Portfolio impact: In several contemporary vehicle architectures, press-hardened components represent a material share that materially affects body weight and crash performance trade-offs; decisions on where and how to deploy press hardening shape vehicle-level outcomes.

- Energy and process economics: Energy efficiency gains from newer press and furnace architectures are no longer marginal — they materially reconfigure total cost of ownership (TCO) for lines and are therefore a central determinant when comparing retrofit versus greenfield investments.

- Input volatility: Steelmaking and raw material inputs remain the dominant cost driver in the upstream value chain, constituting the majority share of production costs and magnifying the sensitivity of press hardening economics to commodity cycles and sourcing strategy.

What the PW Consulting Report Delivers — Practical, Operational, Strategic

This study was built to be operationally useful for investors, OEM program leaders, Tier‑1s, and plant operations managers. Key deliverables include:

Press Hardening Machine Market

- Robust market sizing and scenario forecasts (2020–2032) with base-year calibration and upside/downside programme adoption scenarios to 2032.

- Investment and TCO models that isolate CapEx, energy, tooling, and maintenance levers — allowing quick “what‑if” work for retrofit vs new-line decisions.

- Supply chain stress tests that quantify exposure to raw material price shocks and rate-of-change risk for furnace/press procurement timelines.

- Comparative supplier scorecards and risk maps built from operational KPIs (availability, cycle-time, energy per cycle, service footprint) and technology readiness assessments.

- M&A and partnership heatmaps identifying where consolidation and vertical integration could capture value across the line: presses, furnaces, automation and post‑process cooling.

- Implementation playbooks and procurement checklists tailored to OEMs and Tier‑1s, including standardized contract clauses for energy guarantees, performance SLAs, and retrofit scopes.

- Regulatory and quality compliance matrices aligning heat‑treat control capabilities (in-line pyrometry, IR cameras, automated logging) with commonly required automotive standards.

To preserve actionable advantage for subscribers, the full report contains the detailed regional and application splits, supplier level pricing matrices, and the raw datasets that power our models. These are intentionally withheld from this briefing to encourage direct engagement and provide clients with exclusive access to the underlying tables and scenario files.

Competitive Landscape — Who Moves the Market and Why

The press hardening equipment market exhibits a mid-to-high degree of concentration. Our concentration metrics indicate the three largest suppliers control a majority share of installed capacity, and the top five approach three‑quarters of the market — a structure that favors integrated, turnkey providers when OEMs seek single-source accountability for high-throughput, high‑quality lines.

- AP&T (Ulricehamn, Sweden): A pioneer in press hardening, AP&T combines turnkey delivery with advanced concepts such as SkyLines and Multi‑Layer Furnace systems. Their emphasis on integrated automation, in-line monitoring and energy efficiency positions them strongly where OEMs demand sustainability and cycle repeatability on complex, large-part programs.

- Fagor Arrasate (Arrasate, Spain): Known for full-line automation and servo-hydraulic press technologies, Fagor is a go-to for customers prioritizing flexible transfer systems and multilevel furnaces that support mixed-product high-automation environments.

- Schuler Group (Göppingen, Germany): Schuler brings high-precision PCH flex concepts and high-throughput presses capable of extremely high parts-per-minute production. Their value proposition centers on combining precision with volume for programs that require aggressive takt times.

- Macrodyne Technologies Inc. (Canada): A specialist in custom hydraulic and servo hot-stamping presses, Macrodyne is notable for its close integration with automation suppliers and field experience in complex components for the automotive supply chain.

- Loire Gestamp (Hernani, Spain): With a long track record in hydraulic hot stamping lines, Loire Gestamp is known for pragmatic, proven lines and strong aftersales in established automotive clusters.

Selected, timely developments underscore how supplier strategies are evolving: AP&T’s mid‑2025 SkyLines presentation emphasized multi-part integration and energy reductions designed for electric vehicle (EV) body structures, while Macrodyne’s presence at MACH 2026 showcased heated platen and hot-stamping advances aimed at complex part geometries and faster changeover times. These tactical moves reflect an industry prioritizing energy, modularity, and lifecycle service assurances.

Technology and Cost Dynamics to Watch

Three technical trends dominate operator and buyer decisions:

- Energy efficiency as a procurement differentiator: Suppliers increasingly advertise step-change energy savings. For example, modern servo presses can reduce drive energy demand markedly versus legacy hydraulics, and Multi‑Layer Furnace architectures deliver significant fuel/energy reductions through heat recovery and reduced reheat losses. These reductions translate directly into lower OPEX and shorter payback horizons for greenfield projects.

- Inline process control and traceability: Integration of pyrometers, infrared imaging and automated logging is moving from “value-add” to baseline expectation—largely because these systems support automotive heat-treat standards and facilitate rapid root-cause analysis for warranty and quality events.

- Automation and modularity: Transfer/feed lines and robotics continue to push cycle times and reduce labor exposure. Modular furnace and press configurations allow OEMs to stage capacity additions and adapt to multi-platform programs without wholesale retooling.

From a cost standpoint, raw materials remain the dominant economic factor in component production. This places a premium on process yield, scrap minimization, and supplier strategies that can de-risk steel sourcing — themes we model extensively in the full report.

Strategic Imperatives for 2026 Decision-Makers

Based on our analysis, executives should prioritize three strategic moves this year:

- Lock in energy-anchored benchmarks early: Require energy and throughput guarantees in procurement RFPs and use the report’s TCO templates to compare suppliers on lifecycle cost rather than headline price.

- Choose integration partners, not only equipment vendors: For high-complexity programs — particularly EV architectures — choose suppliers capable of turnkey delivery, including automation, tooling, and process monitoring. The market concentration characteristics favor such partners for risk transfer and schedule certainty.

- Implement flexible deployment roadmaps: Favor modular furnace/press stacks that allow capacity growth and part-mix changes without major reworks. Our retrofit vs greenfield decision trees in the report are designed to quantify the trade-offs in calendar time, spend, and program risk.

How to Use This Study

The full PW Consulting Press Hardening Machine Market report is structured for immediate use: each chapter contains executive targets, procurement checklists, an interactive scenario workbook, and a supplier suitability matrix keyed to program archetypes (low-volume high-complexity, high-volume high-throughput, and hybrid lines). C-suite leaders will get board-ready implications; plant managers and procurement will find immediate RFP language and performance KPIs to include in tender documents.

For stakeholders preparing 2026 capital plans or evaluating M&A and partnership opportunities, the report’s scenario modelling and supplier concentration mapping provide a decision-grade foundation. To access the full dataset, supplier-level benchmarking, and executable playbooks, visit PW Consulting’s publications page to download the comprehensive report and associated Excel models.

PW Consulting remains available to conduct bespoke workshops and to run client-specific sensitivity analyses that map our market scenarios to your program timelines, scope, and P&L constraints.

For detailed analysis of this topic, please visit the official page:Press Hardening Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com