Precursors for Semiconductor Market 2026 Expanding at 8.1% CAGR Amid Advanced Chip Fabrication Growth

Other |

2026-06-19 07:03:13

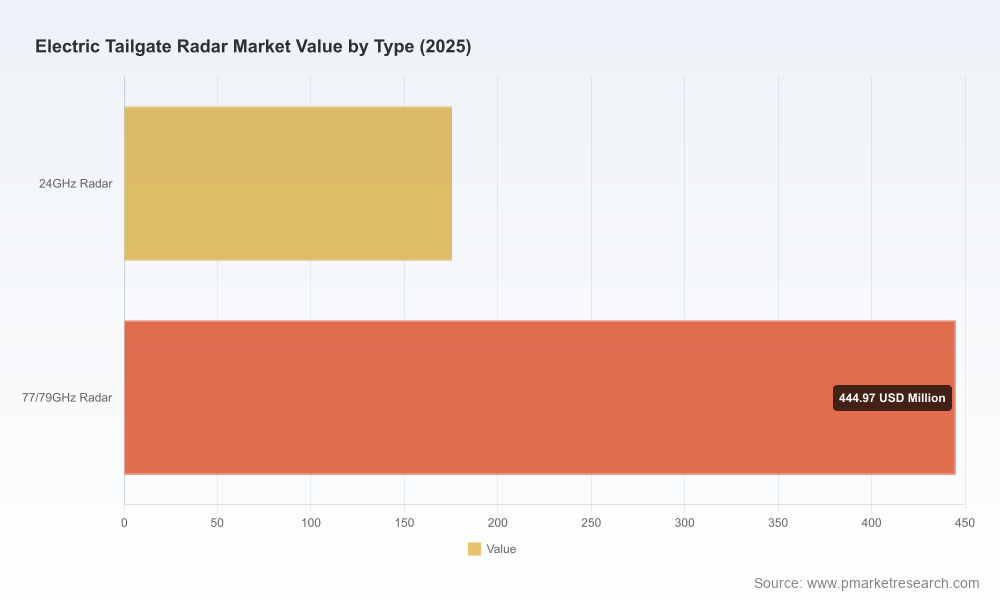

PW Consulting’s latest Electric Tailgate Radar Market report—anchored on a 2025 base year and covering 2026–2032 forecasts—translates market dynamics into actionable insight for OEMs, Tier‑1 suppliers, semiconductor vendors, and private equity investors. The electric tailgate sensor market is on a structurally upward trajectory: global revenue expanded from USD 312.45 Million in 2020 to USD 620.45 Million in 2025, and our forecast anticipates continued growth at a compound annual growth rate (CAGR) of 8.65% across the 2026–2032 horizon. By 2032 the market is expected to exceed USD 1.1 Billion, underscoring a multi‑year commercial runway for sensor and subsystem innovation.

Electric Tailgate Radar Market

Rapid adoption of hands‑free tailgate systems is creating a differentiated comfort and safety play for vehicle brands. Tailgate radar—and increasingly hybrid sensor architectures combining mmWave radar, UWB and ancillary proximity sensors—are migrating from optional features to expected product attributes in certain segments.

Electric Tailgate Radar Market

Technology convergence and regulatory tightening are compressing product development cycles. New frequency and emissions requirements for mmWave operation, plus functional safety standards, demand both engineering rigor and regulatory foresight.

Electric Tailgate Radar Market

Market structure shows moderate vendor concentration: the top three players account for a meaningful share of current revenue, and the top five consolidate over half the market. This creates windows for both incumbents to scale through volume and for challengers to value‑engineer specialty offerings.

Robust market sizing & forecast model (2020–2032) with scenario layers calibrated to macro‑economic sensitivities, EV adoption curves, and OEM feature uptake timelines. The model is provided in a configurable workbook so teams can test bespoke scenarios for price, penetration, and supply constraints.

Technology landscape and techno‑economic assessment that compares sensor modalities (radar frequency bands, UWB, ultrasonic, and hybrid fusion) across cost, reliability, integration complexity, and validation effort. We stress the tradeoffs between precision (e.g., gesture recognition fidelity) and BOM/tuning cost.

Regulatory and functional safety matrix mapping UN ECE R10, FCC/ETSI frequency parameters for mmWave operation, and ISO 26262 expectations (notably ASIL requirements relevant to obstacle detection). The matrix translates standards into concrete design and test checkpoints.

Competitive vendor scorecards and supplier due diligence templates that synthesize product maturity, manufacturing readiness, quality history, and commercial exposure—enabling procurement and strategy teams to shortlist partners within weeks.

Go‑to‑market playbooks for Tier‑1 suppliers and semiconductor vendors including recommended pricing strategies, bundling approaches (sensor + actuator + software), and strategic partnerships with OEM integration teams.

Supply‑chain risk heatmap and mitigation playbook—covering semiconductor lead‑time scenarios, alternate sourcing, and inventory strategies. Importantly, our supply‑chain baseline incorporates recent improvements: semiconductor lead times for mmWave chips showed measurable reduction in early 2026, improving flexibility versus the prior two years.

M&A and partnership scouting list (screened for IP, customer access, and manufacturing synergies) together with a valuation framework for bolt‑on acquisitions and minority investments.

The competitive field blends automotive systems integrators, radar specialists, and component semiconductor houses. Our analysis highlights a mix of incumbents who provide end‑to‑end tailgate systems and focused radar suppliers who enable precise hands‑free activation.

Huf Group (Velbert, Germany) — recognized for 79 GHz radar kick sensors with demonstrated series production wins. Their compact, high‑precision modules are positioned for premium OEM programs where gesture fidelity and low false‑trigger rates are prerequisites.

InnoSenT GmbH (Donnersdorf, Germany) — specialist radar solutions with strong competency in tailgate kick sensor applications; their depth in tuning and automotive validation makes them an attractive partner where rapid integration into existing ECU architectures is required.

Continental AG (Hanover, Germany) — leverages system integration capabilities across radar, sensor fusion, and power tailgate actuation. Continental’s strength is in translating sensor performance into robust customer features including obstacle detection and fail‑safe behaviors.

Brose Fahrzeugteile (Coburg, Germany) — known for drive systems and sensor interfaces; Brose’s recent demonstrations at major trade shows emphasize multi‑protocol approaches (including UWB) and modularization to lower integration friction for OEMs.

Aisin Corporation (Kariya, Japan) — strong presence in Asian OEM programs with tailored power tailgate assemblies that integrate radar and proximity sensing appropriate for regional packaging and validation constraints.

Texas Instruments (Dallas, USA) — a critical upstream supplier, providing mmWave chips and reference modules that underpin many kick‑sensor solutions. Their roadmap and pricing/prioritization materially influence Tier‑1 BOM decisions.

Recent vendor movements validate the trajectory we outline. Notable examples include a 79 GHz series production order won by a radar specialist in mid‑2025, Brose’s public showcase of UWB and sensor integration at a major Asian motor show in early 2025, and advances in UWB SoC functionality that extend hands‑free control robustness into more challenging environments. These events reflect a market transitioning from proofs‑of‑concept to scalable production.

Frequency and emissions regimes: compliance with updated UN ECE R10 and national frequency allocations (FCC/ETSI) for 79 GHz operation is non‑negotiable. Certification timelines should be built into 2026 launch pathways.

Functional safety: ISO 26262 obligations (including ASIL requirements for obstacle detection elements) will shape architecture decisions. Suppliers lacking a clear ASIL delivery record elevate integration risk.

Supply resilience: semiconductor lead times improved meaningfully in Q1 2026 versus the previous year—this provides a window to re‑optimize just‑in‑time strategies and reduce buffer stock without increasing production risk, but volatility remains a credible downside scenario.

Prioritize sensor fusion over single‑technology bets. Firms that combine mmWave radar with UWB and intelligent signal processing will capture a premium on reliability and reduce warranty exposure.

Embed regulatory compliance and ASIL planning into program milestones. Treat certification as a pathfinder, not a gating task at the end of hardware design.

Use supplier scorecards to allocate program risk: dual‑sourcing mmWave ASICs where feasible, and locking Tier‑1 partners with proven production track records for initial series programs.

Leverage the current improvement in semiconductor availability to negotiate favorable lead times and price tiers, but maintain contingency pools for potential supply stressors.

For investors: target differentiated IP in signal processing or UWB SoC platforms and evaluate bolt‑on targets that accelerate time‑to‑market with validated OEM integrations.

The report is intentionally structured as an operational toolkit for 2026 decision cycles: an editable financial model, supplier due‑diligence templates, a regulatory compliance checklist, and tactical go‑to‑market playbooks. We present layered scenarios—baseline, upside (faster OEM adoption), and downside (regulatory delay or supply disruption)—to stress test product roadmaps and investment theses.

This briefing outlines the macro momentum and decision levers. To preserve the “trailer” nature of this release and to ensure that strategic partners derive full value, we have withheld granular regional and application splits, as well as detailed vendor market shares that form the central intelligence of the report. These elements are included in the full PW Consulting Electric Tailgate Radar Market report and accompanying data package, which provide the precise segmentation, time‑series detail, and vendor benchmarking necessary for M&A diligence, procurement negotiations, and program costing.

Contact PW Consulting to request the full report, tailored briefings, and the interactive forecast workbook to support your 2026 strategy and execution planning.

For detailed analysis of this topic, please visit the official page:Electric Tailgate Radar Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com