A Strategic Approach to Consumer Analytics in the Automotive Industry: Insights from Grand View Brainshare

Other |

2026-03-23 18:41:50

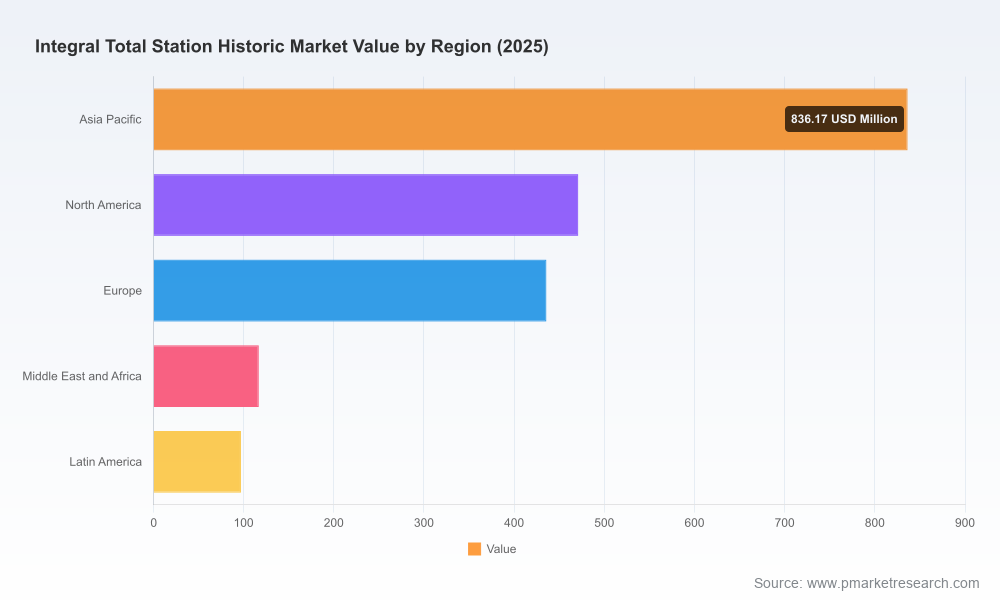

PW Consulting’s latest Integral Total Station Historic Market research synthesizes seven years of market performance and a forward-looking 2026–2032 forecast to equip executives with the intelligence required to make high-consequence decisions in 2026. The global total station market has demonstrated steady expansion, rising from approximately USD 1.44 billion in 2020 to nearly USD 1.96 billion in 2025. Our modelling shows that, under current structural drivers, the market is expected to continue compounding through the forecast window, reaching just over USD 3.09 billion by 2032 at a 6.75% CAGR for 2026–2032. This trajectory confirms the segment’s transition from a specialized surveying tool to a core precision instrument embedded in digitized construction, mining, and infrastructure workflows.

Integral Total Station Historic Market

Timing and capital allocation: The market growth pattern from 2020–2025 and the robust mid-single-digit CAGR projected for 2026–2032 mean 2026 is a pivotal year for reallocating R&D and capex into automation, cloud-enabled services, and lifecycle support models.

Integral Total Station Historic Market

Technology convergence: Total stations are no longer discrete instruments — they are nodes in an integrated positioning ecosystem. Strategic choices made in 2026 about cloud platforms, GNSS-hybrid integration, and edge processing architectures will determine relevance for the next product cycle.

Integral Total Station Historic Market

Competitive posture: Market concentration is material — our concentration analysis shows top three players capture a majority share and the top five approach three quarters of the market. For challengers and regional specialists, 2026 is about choosing differentiated routes-to-market that exploit adjacency plays (e.g., scanning, site-automation) rather than competing on instrument price alone.

Risk management: Supply-side dynamics — notably sensor availability and episodic component tightness observed in 2025 — require near-term procurement and design hedges. Regulatory alignment with calibration and survey accuracy standards must be embedded into product roadmaps and service level agreements.

Validated market sizing and historic performance modelling (2020–2025) plus a transparent forecast methodology for 2026–2032 that supports scenario analysis and sensitivity testing.

An operational supply-chain map identifying critical component nodes (sensors, EDM modules, optics, software stacks) and mitigation levers for scarcity and cost volatility.

Commercial playbooks for OEMs, distributors, and large end-users covering pricing strategy, bundling and subscription models, aftermarket services, and field-support economics.

Technical trend synthesis: robotic automation, GNSS-total-station fusion, cloud-based data management, image-assisted workflows, and asset security features — each assessed for adoption timelines and margin impact.

Competitive intelligence: structured profiles of market leaders and challengers, benchmarking across product capabilities, channel footprints, and strategic moves — with a focus on what matters for 2026 competitive positioning.

Go-to-market playbook and deal screening tool for M&A, JV, and partnership decisions designed to highlight highest-value inorganic and alliance targets while preserving operational upside.

Board-ready executive slides and a 90-day implementation roadmap for commercial and product leaders to capture near-term opportunities.

The sector exhibits meaningful concentration: the top three players command a large share of the market and the top five collectively hold around three-quarters of industry revenue. This structure underpins two enduring dynamics. First, incumbents with scale benefit from integrated software ecosystems, broad service networks, and product portfolios that span entry-level to high-end robotic offerings. Second, nimble regional players and lower-cost manufacturers continue to pressure pricing at the point-of-sale and to capture share through localized service excellence.

Leading OEMs are advancing three differentiating vectors that will define 2026 competitiveness:

Cloud and security. Major players have introduced cloud-based data platforms and instrument protection services to secure high-margin recurring revenue. Recent product enhancements include native cloud synchronization and theft-detection features tailored for high-value robotic instruments.

Automation and workflow integration. Robotic total stations with advanced automation and hybrid GNSS integration now target full-site layout workflows. These solutions reduce labour demand and enable new contracting models tied to productivity outcomes.

Product breadth and affordability. A bifurcated market remains — high-precision automated instruments and cost-effective manual options — allowing incumbents to defend top-line value while challengers expand in volume-sensitive segments.

Selected corporate signals that matter:

Strategic platform releases and security feature rollouts indicate incumbent strategies to lock in enterprise customers via data capture and lifecycle services.

Partnerships with construction integrators underscore the industry’s pivot from component sales to integrated delivery of survey-to-build workflows.

New robotic product introductions reaffirm the emphasis on automation and reduced field headcount, shaping procurement specifications for 2026 infrastructure projects.

For OEMs: accelerate integration of cloud-native services and instrument security into product roadmaps; monetize data through tiered subscriptions and outcome-linked service contracts. Protect gross margins by offering certified refurbishment and calibrated components as higher-margin aftermarket services.

For distributors and service providers: invest in training, remote-support tooling, and SLA-backed calibration services. Differentiate through uptime guarantees and rapid field recovery — valuable where large projects require deterministic delivery.

For contractors and large end-users: redesign procurement to favour lifecycle cost and productivity metrics over unit price. Pilot hybrid models that pair robotic stations with centralized processing and remote stakeout to reduce on-site labor-related variability.

For investors and M&A teams: prioritize targets that strengthen cloud capabilities, data ownership, and aftermarket control. Divest non-core low-margin hardware where scale is insufficient to sustain distribution economics.

Cross-functional operational hedge: diversify component sourcing, engage in multi-year supply agreements for critical sensors, and design modular electronics that permit substitution without full platform redesign.

Component supply and input cost shocks. Sensor availability and episodic price tightness observed in 2025 can compress margins and extend lead times; design-for-supply and dual-sourcing are immediate mitigations.

Regulatory and standards adherence. Surveying accuracy standards and calibration protocols are non-negotiable in many markets; product claims and warranties must align with ISO and project-specific tolerances to avoid commercial disputes.

Platform lock-in trade-offs. While cloud platforms offer stickiness, they also create integration risk and require ongoing investment in cybersecurity and data governance.

Constructive disruption. Continued adoption of site automation and alternative positioning technologies may compress certain manual-product segments faster than anticipated; maintain optionality across product lines.

Our advisory engagement model for 2026 is designed to move from insight to impact in 90 days. PW Consulting offers:

Custom scenario modelling that overlays client-specific product mixes onto our market forecast to produce P&L and cash-flow implications for 2026–2028.

Deal origination and target screening using proprietary scoring that weights data-platform capability, aftermarket potential, and channel synergies.

Commercial transformation workshops that reorient sales compensation, pricing, and service delivery around lifecycle value rather than discrete unit sales.

Rapid risk-audit of supply chains with negotiated remediation playbooks for sensor and electronic component scarcity.

2026 will separate organizations that see total stations as isolated hardware into two camps: those who treat the instrument as the starting point of an integrated, data-driven productivity system; and those who compete on legacy product attributes alone. The market’s steady expansion and the structural concentration among leading players suggest that scale, platform capability, and go-to-market discipline will determine winners. For stakeholders making strategic decisions in 2026 — whether allocating R&D budgets, evaluating acquisitions, or restructuring commercial models — the priority is to secure control over data flows and service economics while hedging supply-side risks that can undermine execution.

To access the full dataset, benchmarking dashboards, and the implementable 90-day playbook that accompany this executive summary, visit PW Consulting’s Integral Total Station Historic Market page or contact our advisory team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Integral Total Station Historic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com