North America Carpets and Rugs market Size, Share, Trends, Key Drivers, Growth and Opportunity Analysis

Other |

2026-05-20 10:05:18

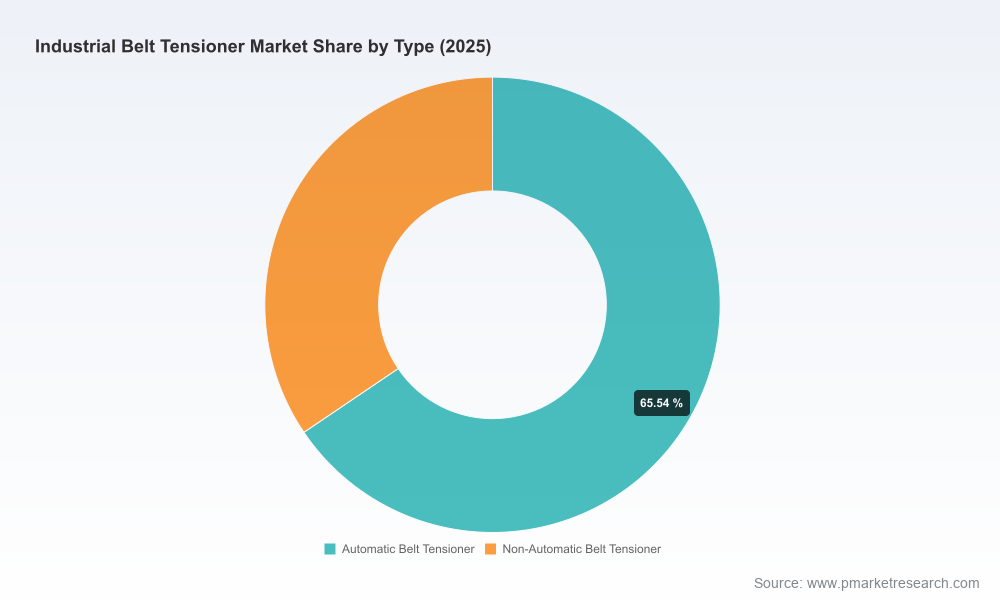

PW Consulting today releases a strategic brief that translates our full Industrial Belt Tensioner Market report into actionable guidance for executives planning 2026 investments and portfolio moves. Building on a five‑year historical baseline (2020–2025) and a seven‑year forecast window (2026–2032), the analysis maps where value is forming across product architectures, distribution channels, and technology adjacencies. The headline: the global market is on a steady expansion path—from a mid‑single‑billion dollar industry in the early 2020s to a multi‑billion dollar market by the end of the decade—driven by steady industrial modernization, aftermarket growth and increasing emphasis on energy efficiency. We forecast compounded expansion at roughly 6.08% CAGR through 2032, underpinning meaningful opportunity for differentiated players.

Industrial Belt Tensioner Market

Near-term capital allocation: With the market firmly in growth mode, 2026 is a pivotal year for translating R&D into scale. Companies that allocate CAPEX to modular tensioner platforms and sensor-enabled service offerings will capture a disproportionate share of aftermarket economics.

Industrial Belt Tensioner Market

Supply‑chain resilience: Volatility in raw material inputs—most notably natural rubber and steel, which have shown large annual swings—means procurement strategies and hedging mechanisms must be reworked now to protect margins in 2026 and beyond.

Industrial Belt Tensioner Market

Regulatory-driven product differentiation: Recent regulatory changes, particularly in the EU, are accelerating demand for energy‑efficient power transmission solutions. Buyers will increasingly prefer tensioners that demonstrably reduce parasitic losses and support decarbonization targets.

Competitive positioning: Market concentration metrics indicate a moderately consolidated top tier (CR3 ~38.5%, CR5 ~52.7%). This creates a two-speed field where tier‑one firms solidify scale advantages while nimble specialists can win with technical differentiation and service models.

Transparent market‑sizing and forecast engine: A downloadable model calibrated to our base year (2025), with demand drivers and revenue sensitivity levers for 2026–2032. The model lets users stress test scenarios (commodity shocks, accelerated electrification, aftermarket consolidation) without exposing granular proprietary splits in this brief.

Go‑to‑market playbooks: Segment‑specific route‑to‑market templates for OEM partnerships, industrial distributors and aftermarket service providers—each with recommended commercial terms, margin ladders, and performance KPIs.

Product roadmap blueprints: Prioritized technology investments (e.g., self‑adjusting mechanisms, integrated tension monitoring sensors, vibration‑damping elastomers) aligned to payback timelines supported by TCO calculations.

Supply‑chain and procurement scorecards: Vendor selection matrices, hedging tactics for rubber and steel exposure, and contingency plans to mitigate 20–35% annual raw material swings observed in recent years.

Competitive benchmarking and M&A screeners: A comparative matrix of engineering breadth, patented features, manufacturing footprint, and aftermarket reach—plus a prioritized list of acquisition targets and partnership archetypes to accelerate capability builds.

Commercial impact tools: Pricing sensitivity analyses, distributor commission frameworks, and service pricing models that convert improved reliability and sensorization into recurring revenue.

Regulatory and sustainability playbook: Compliance checklists and decarbonization levers mapped to product design choices that yield the largest emissions and efficiency gains in industrial settings.

Structural growth with tactical inflections. The industry’s mid‑term trajectory—characterized by a steady CAGR—creates room for both scale plays and targeted specialization. Players should not assume uniform demand: growth pockets will appear around energy‑savings solutions, retrofitting services, and heavy‑duty industrial applications.

Raw material price volatility as an operational lever. The historic swings in rubber and steel prices have moved from episodic to structural. Procurement teams need to pair spot purchasing with strategic long‑term contracts and consider design choices that reduce material sensitivity without compromising performance.

Regulatory tailwinds for efficiency. Policy shifts encouraging lower industrial emissions will accelerate adoption of tensioner systems that reduce drag and enable smarter accessory drives. Compliance is quickly becoming a market differentiator rather than merely a cost of doing business.

Aftermarket as a margin engine. Service and replacement cycles for belt tensioners create high‑margin recurring revenue. Firms that bundle predictive maintenance, sensor upgrades and performance guarantees will expand lifetime revenue per asset.

The competitive field combines global diversified industrial suppliers and focused specialists. The report profiles leading names and distills their strategic postures:

Gates Corporation (Denver, CO) retains strength through breadth—offering an extensive portfolio engineered for heavy‑duty tolerances. Their depth in power transmission and OEM relationships makes them a natural partner for customers seeking one‑stop systems integration.

Fenner Drives (Manheim, PA) remains a leader in self‑adjusting rotary and linear tensioners, winning business where simple, reliable automation of tension is required across industrial and HVAC segments.

BRECOflex (Eatontown, NJ) differentiates on precision for timing and linear drives, targeting use cases where tight tension control underpins process accuracy.

Lovejoy (Timken, Downers Grove, IL) leverages elastomeric suspension designs to reduce vibration—an advantage in high‑sensitivity industrial applications.

Dayco (Roseville, MI) has aggressively expanded its product lineup and introduced heavy‑duty tensioners in 2025 to address fleet and severe‑duty markets—moves that increase competition in both OEM and aftermarket channels.

Continental AG (Hanover) and Bando (Osaka) bring global scale and integrated pulley systems, serving customers that value systems‑level reliability and service coverage.

SKF (Gothenburg) pairs hardware with measurement tools, making them attractive to customers seeking validated maintenance programs and in‑field measurement capabilities.

B&B Manufacturing (La Porte, IN) exemplifies the high‑service, custom‑oriented supplier—fast to respond for bespoke and small‑batch industrial requirements.

Recent industry moves—such as Dayco’s 2025 product expansions and trade‑show showcases from other suppliers—signal that incumbents are accelerating both product and channel plays to defend and extend market positions. Our competitive heatmaps identify where scale, technical IP and aftermarket reach overlap; those intersections are where acquisition and partnership activity is most likely in 2026–2027.

Define a two‑track product strategy: invest in a core modular platform for high‑volume opportunities while funding a parallel engineering stream for sensorized, premium tensioner offerings that unlock aftermarket subscription revenue.

Rewire procurement to manage raw material volatility: use layered contracting (short, medium and long term), localize critical inputs where feasible, and consider material substitution tests to dampen exposure.

Monetize maintenance intelligence: pilot sensor retrofits on installed bases to prove predictive maintenance value and then roll out bundled service agreements that convert one‑off sales into annuity streams.

Pursue targeted M&A: prioritize targets that add either proprietary tensioning mechanisms, regional service networks, or specialist manufacturing capabilities that shorten time‑to‑market for new designs.

Reassess pricing and warranty structures: introduce performance‑based warranties that trade higher upfront prices for demonstrated lifecycle savings—this aligns supplier incentives with customer efficiency goals and regulatory compliance.

Our full report provides the detailed, downloadable models, competitive scorecards and transactional playbooks that boards and corporate development teams need to act. It includes a calibrated revenue forecast engine (USD, revenue unit: Million), market concentration analytics, supplier risk matrices, and a prioritized list of strategic options tailored to different corporate archetypes (global OEM, regional distributor, specialty manufacturer).

This strategic brief is a preview: it demonstrates the analytical depth and tactical orientation of PW Consulting’s Industrial Belt Tensioner Market report while reserving the granular subsegment tables and deal‑level recommendations for the full document. For the complete dataset, scenario models, and bespoke advisory engagements that translate these insights into a 100‑day plan, please visit PW Consulting’s report page to download the executive summary or to request a client briefing.

For detailed analysis of this topic, please visit the official page:Industrial Belt Tensioner Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com