Chip Encapsulation Resin Market 2026: Strategic Imperatives from PW Consulting’s New Industry Brief

Executive snapshot

As semiconductor packaging evolves to meet the throughput, thermal and reliability demands of AI accelerators, power electronics and next‑generation consumer devices, the chip encapsulation resin market is transitioning from a commodity cycle to a strategic materials race. PW Consulting’s latest market brief projects the industry to expand from a 2025 revenue base of USD 3,892.6 Million to an expected USD 6,169.3 Million by 2032 — a compound annual growth rate (CAGR) of 6.81% over the 2026–2032 forecast horizon. For corporate leaders planning 2026 capital allocation, sourcing and product roadmaps, this report translates that headline growth into actionable choices across technology, capacity, procurement and M&A.

Chip Encapsulation Resin Market

Why this brief matters for 2026 decision-makers

- Timing capital and capacity: With structural demand drivers (AI packaging, EV power modules, 5G/6G telecom, and ruggedized industrial electronics) accelerating, the 2026 planning cycle must reconcile near‑term supply dynamics with multi‑year investments in molding, dam‑and‑fill and underfill capabilities.

- Protecting margins in a materials‑sensitive chain: Resin makers and OEMs face margin pressure tied to upstream feedstock moves and regulatory compliance costs; the report quantifies likely scenarios and tactical hedges for procurement teams.

- Differentiation through materials innovation: Thermally‑conductive, ultra‑low alpha and high‑Tg resin systems are no longer niche — they are strategic enablers for premium packaging. Our analysis clarifies which technical bets align with which end‑market paybacks.

- Concentration and competitive dynamics: The market exhibits a high degree of concentration among a handful of global suppliers — an important consideration for risk management, single‑source exposure and partnership strategies.

What’s driving demand — a nuanced view

The sector’s mid‑to‑long term growth is anchored by three structural trends: the proliferation of advanced packaging for AI and high‑performance compute, the electrification of transport requiring more robust power semiconductor encapsulation, and the persistent demand for smaller, more reliable consumer modules. These drivers increase technical requirements — thermal conductivity, moisture resistance, low‑alpha emissions, high glass transition temperature (Tg) — which, in turn, favor suppliers with deep formulation expertise and tight process controls.

Chip Encapsulation Resin Market

At the same time, cyclical forces remain relevant. Raw material dynamics — including feedstock oversupply or price declines — and trade/regulatory measures have created short‑term dislocations in supply and pricing. Our brief models multiple raw‑material scenarios and their probable impact on producer margins and downstream pricing over the 2026 planning window.

Chip Encapsulation Resin Market

Competitive landscape — who matters and why

Market concentration is significant: the top three players account for a dominant portion of global revenues, while the top five command an even larger share — a structural feature that shapes supplier bargaining power and investment behavior. Against that backdrop, our company profiles provide direct insight into capability gaps and strategic intent among market leaders:

- Sumitomo Bakelite Co., Ltd. (Tokyo) — A recognized leader in epoxy molding compounds (EMC) with recent capacity expansions and new plant commissioning to capture AI and automotive packaging demand; notable for supply footprint and volume scale.

- Shin‑Etsu Chemical Co., Ltd. (Tokyo) — Leverages vertical integration in silicon chemistry to deliver low‑alpha, high moisture‑resistance formulations for advanced nodes; a strong player where purity and contamination control are decisive.

- Henkel AG & Co. KGaA (Düsseldorf) — Broad portfolio across glob‑top, dam‑and‑fill and underfill systems; recent introductions include thermally conductive EMC tailored for EV power electronics, signaling a move to capture high‑value automotive segments.

- Resonac Holdings (formerly Showa Denko/Hitachi Chemical) (Tokyo) — Focused on heat‑resistant EMC for power modules, emphasizing high‑Tg formulations validated to rigorous reliability standards for harsh environments.

- Nitto Denko, Mitsubishi Chemical, Kyocera, Samsung SDI, LG Chem, Huntsman and Evonik — Each brings complementary strengths in specialty polymers, material science or captive demand exposure that influence regional supply dynamics and technology availability.

- Chang Chun Group (including Chang Wah Electromaterials) and Panasonic — Regional manufacturers and joint ventures that provide capacity and responsiveness to local backend fabs and EMS clusters.

Recent corporate moves — from Sumitomo Bakelite’s multi‑site capacity additions to Henkel’s thermal EMC launch — are consistent with our view that suppliers are prioritizing differentiated, high‑reliability grades over volume commodity plays. For buyers, this means a dual challenge: ensuring secure supply of advanced grades while avoiding lock‑in to proprietary chemistries without appropriate commercial protections.

Report contents — operational and decision‑ready tools

Our brief is designed as a practical playbook for 2026. Key deliverables include:

- Market sizing and forecast model (2020–2032) with scenario layers for technology adoption rates and regional node investment paths. The model is exportable for bespoke sensitivity testing.

- Supply chain and capacity map capturing existing plants, announced expansions and likely pinch points for advanced EMC grades — with risk ratings for single‑source exposures.

- Raw material outlook and procurement playbook that translates feedstock scenarios into price and margin impacts, suggested hedging windows, and supplier negotiation levers.

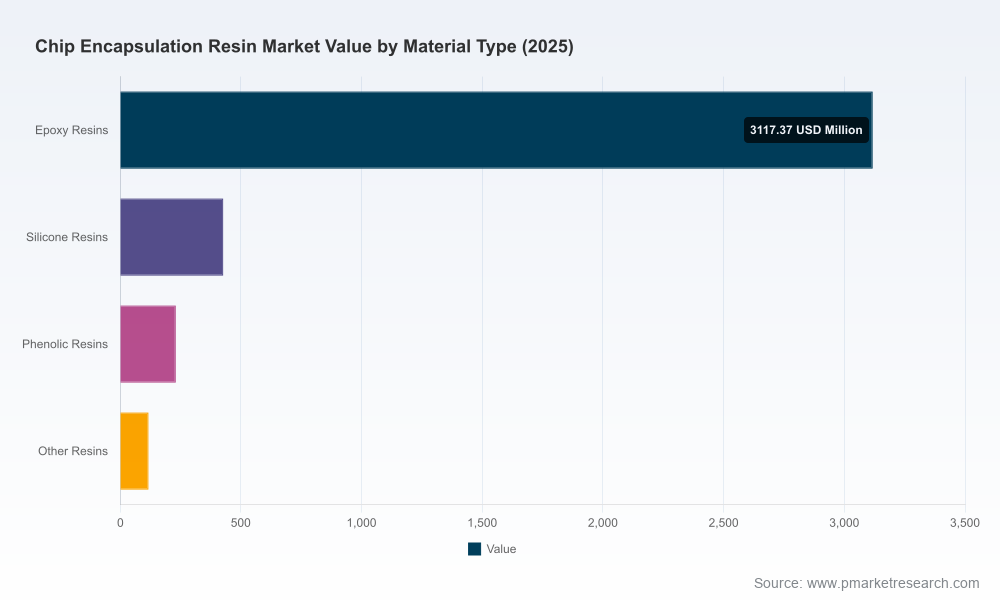

- Technology heat‑map comparing epoxy, silicone, phenolic and novel chemistries across performance vectors (thermal, moisture, alpha, processability) and recommended go‑to‑market roadmaps by application tier.

- Competitive benchmarking dossier with strategic profiles, investment activity timelines and likely next moves for leading suppliers — supporting supplier selection and partnership screening.

- M&A and alliance screening framework prioritizing targets on technology, captive demand, geographic access and manufacturability, including an acquisition valuation template and integration risk checklist.

- Operational templates: CapEx sizing for new lines, ROI calculators under alternate demand curves, and a production‑scale validation checklist to reduce ramp risks for new resin grades.

Strategic implications and recommended actions for 2026

- Prioritize materials that solve end‑customer performance pain points. For EV power modules and AI packaging, thermal conductivity and high‑Tg stability drive willingness to pay. Invest selectively in co‑development agreements that embed OEM requirements into resin formulations.

- De‑risk sourcing early. Given market concentration and the technical nature of advanced grades, adopt a two‑track supplier strategy: secure primary supply with capacity commitments while qualifying alternative regional sources for contingency.

- Time capital to feedstock cycles. Our commodity scenario analysis suggests windows where upstream softness can materially lower capex unit costs; align major investments to these windows unless strategic urgency dictates otherwise.

- Embed regulatory and reliability testing in early design phases. Compliance with regionally distinct rules and lifecycle reliability metrics (e.g., high‑temp storage, moisture sensitivity) should be gating criteria for any new resin adoption.

- Design commercial terms that protect intellectual property while enabling scale. Co‑development should include clear specifications, fallback formulations and supply continuity clauses to avoid proprietary lock‑in risk for large OEMs.

- Scan for inorganic opportunities that accelerate market entry or capability gaps — particularly in thermal interface materials, ultra‑low alpha chemistries and regional production footholds near major assembly clusters.

How PW Consulting’s brief positions you to act

Think of this report as the executable briefing for 2026: not just market forecasts, but the tactical templates procurement, R&D and corporate development teams need to move decisively. The analysis ties the headline CAGR and market scale to supplier behavior, feedstock swings and product innovation — showing where value will accrue and where risk is concentrated. For leaders who must prioritize between expanding legacy epoxy capacity versus investing in specialty thermal resins, the brief provides the financial and operational trade‑offs to support board‑level decisions.

Conclusion and next steps

The chip encapsulation resin market is at an inflection where technical differentiation and supply reliability increasingly eclipse pure price competition. PW Consulting’s 2026‑focused brief synthesizes market size and trajectory with practical, transaction‑ready tools — from procurement playbooks to M&A screening matrices — to help clients convert the sector’s growth into defensible competitive advantage.

To access the full suite of models, supplier maps and scenario tools referenced in this brief, and to obtain the detailed segment and regional splits that inform recommended actions, please consult our full market report on the PW Consulting research portal. The brief presented here is intentionally selective — our full publication contains the granular intelligence that operational teams use to finalize 2026 budgets and supplier contracts.

For detailed analysis of this topic, please visit the official page:Chip Encapsulation Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com