Data Center Network Market 2026: Strategic Imperatives from PW Consulting’s New Market Research

As enterprises, cloud providers, and infrastructure investors plan capital and technology choices for 2026 and beyond, PW Consulting’s latest Data Center Network Market study delivers the strategic intelligence required to convert uncertainty into advantage. This release synthesizes macro trajectories, competitive tensions, regulatory shocks, and executable operating models—framed to inform board-level decisions while preserving the proprietary, granular forecasts that drive procurement and deployment strategies.

Data Center Network Market

Executive snapshot: momentum and scale

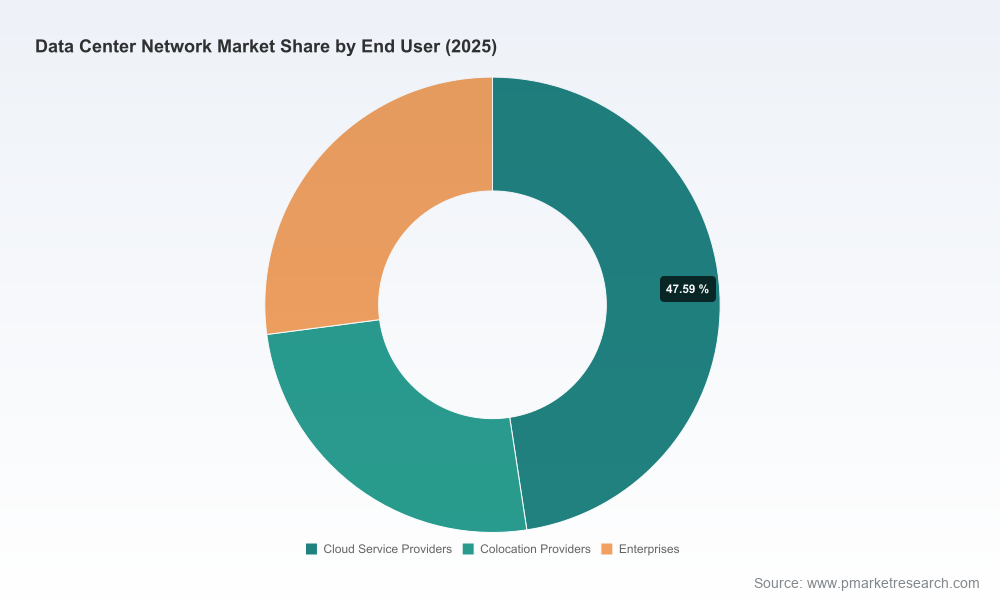

The data center networking market has entered a sustained, high-growth phase driven by AI, hyperscale cloud expansion, and the evolving economics of high-bandwidth fabrics. Our analysis shows the market enlarging from roughly USD 20 billion in 2020 to north of USD 38 billion in 2025, with a projected inflection into 2026 and beyond. Over the forecast window beginning in 2026, the market is expected to expand at a compounded annual growth rate of approximately 15.9%, culminating in a substantially larger market by the end of the forecast horizon.

Data Center Network Market

Two structural observations underpin this growth: first, the unit economics of AI and GPU-scale clusters are forcing network architectures to transition from incremental upgrades to holistic fabric redesigns; second, concentration at the vendor level has intensified, raising strategic procurement and supply-risk considerations for enterprise buyers and cloud operators alike.

Data Center Network Market

Why this report matters for 2026 decision-making

- Actionable capital planning: The study translates macro growth into investment milestones and timing recommendations. Procurement calendars, multi-year CapEx envelopes, and refresh cycles are tied to expected shifts in port density, link speeds, and DPU adoption—allowing CFOs and CIOs to optimize cashflow versus capability trade-offs.

- Risk-aware vendor selection: Our vendor concentration analysis highlights that the top-tier suppliers capture a large and growing share of the market—shaping price negotiation dynamics, warranty and support expectations, and roadmap leverage. The report provides a decision framework to balance market-leading innovations against single-vendor exposure.

- Operational readiness for AI fabrics: Beyond product comparisons, the study includes operational playbooks for deploying AI-optimized fabrics, from cabling and power provisioning to orchestration and lifecycle automation—critical for minimizing downtime as workloads densify.

Key market dynamics shaping 2026 strategies

- AI-driven re-architecture: High-throughput, low-latency interconnects and support for disaggregated architectures (switch/DPU/GPU co-design) are no longer optional for new builds. Decision-makers must evaluate whether to adopt emerging switch silicon and DPUs now or wait for the next generation—an economic and technical trade-off detailed in our TCO scenarios.

- Power and grid realities: Emerging public-private agreements and state-level policies are reshaping the cost of bringing capacity online. Recent industry commitments to cover new generation and grid upgrades, coupled with extended grid connection lead times, mean that behind-the-meter generation and battery-backed solutions are increasingly prominent in site selection and financial models.

- Regulatory and interconnection risk: Several jurisdictions now require large-load customers to assume the cost of interconnection upgrades. These policy shifts materially alter location economics and should be integrated into site selection and build-vs.-colocate decisions.

- Hyperscaler capex behavior: The enormous investment run-rate from the major cloud providers has created both demand pull and supply-side bottlenecks—accelerating innovation in ASICs and fabric software while also stressing manufacturing and procurement timelines.

Competitive landscape: strategic positioning of major vendors

The report provides concentrated, comparative insight into vendor capabilities, ecosystem positioning, and strategic intent. A few directional takeaways:

- Cisco Systems: Continues to push silicon-driven differentiation for hyperscale and enterprise AI data centers. Recent product introductions emphasize scale and programmability for massive link counts, reinforcing Cisco’s role as an anchor supplier for mixed enterprise and cloud deployments.

- Arista Networks: Focuses on high-throughput Ethernet fabrics and efficiency metrics. Arista’s platform-level innovations aim to reduce TCO through power efficiency and integrated software features tailored to cloud-native operating models.

- Juniper / HPE: The integration of Juniper into HPE’s broader portfolio creates a competitive vendor capable of offering end-to-end solutions across edge, campus, and core data center environments—important for organizations seeking single-vendor simplicity coupled with modularity.

- NVIDIA: Is reshaping networking through DPUs and InfiniBand/Ethernet convergence, targeting AI fabrics where GPU interconnectivity and offload accelerate workload performance beyond traditional switching gains.

- Broadcom: Remains a pivotal silicon supplier; ASIC roadmaps from Broadcom influence the capabilities and price-performance of multiple OEMs and are therefore a strategic lever for procurement teams.

- Other notable vendors: Including Dell, HPE, Huawei, Nokia, Extreme, and others, are each carving specialist positions—whether through integrated infrastructure bundles, regional strengths, or optical and interconnect capabilities.

Market concentration metrics underscore the competitive reality: the largest three and five suppliers capture the dominant share of spending, amplifying both bargaining power and systemic supplier risk. Organizations need to model scenarios where a leading supplier tightens volumes or shifts roadmap priorities.

What’s inside the report (practical deliverables)

This study is designed to move organizations from insight to execution. Key operational assets included:

- Scenario-based demand forecasts and high-level market sizing through 2032, with sensitivity to AI adoption curves and hyperscaler CapEx cycles.

- Vendor scorecards and comparative matrices that assess performance, roadmap clarity, ecosystem integration, and support footprint.

- TCO and RoI templates for build vs. buy, buy vs. lease, and colo strategies—customizable for client-specific power, density, and utilization assumptions.

- Network modernization playbooks covering migration sequencing, non-disruptive upgrades, and DPU/switch rollout strategies.

- Regulatory and location risk maps, including the impact of interconnection cost allocation and grid readiness on site economics.

- RFP and contract negotiation checklists focused on software license models, lifecycle support SLAs, and silicon availability clauses.

Consistent with our “trailer” approach, the public summary highlights the strategic levers and key recommendations; the proprietary report contains the granular segmentations, vendor-level market shares by product family, and downloadable financial models available through PW Consulting’s client portal.

Regulatory and infrastructure considerations for 2026

Three infrastructure-policy forces will determine where and how data center networking capacity is procured:

- Power cost allocation and pledges: Recent industry commitments to underwrite grid upgrades mitigate headline political risk but create new contracting and tracking needs for long-term off-take agreements.

- Grid connection lead times: With average waits stretching out significantly in primary markets, capacity forecasts must build in multi-year lead times for interconnection—heightening the importance of early engagement with utilities and creative behind-the-meter design.

- Tier standards and resiliency expectations: International performance frameworks continue to drive network redundancy requirements; operators must reconcile Tier expectations with the capital and operational realities of high-density AI fabrics.

Recommendations: three near-term actions for 2026

- Reframe procurement around architecture risk: Move beyond price-per-port comparisons. Include silicon roadmap alignment, DPU support, and cross-vendor interoperability as mandatory evaluation criteria in procurements issued in 2026.

- Embed power and interconnection contingencies in financial models: Update site-selection tools to incorporate potential direct interconnection charges, grid reinforcement timelines, and behind-the-meter options; stress-test scenarios for 24–36 month vendor delivery variability.

- Adopt phased modernization with interoperability gates: When modernizing fabrics, use phased rollouts that preserve mixed-vendor interoperability, enabling you to capture performance improvements while retaining negotiation leverage.

Conclusion and next steps

The 2026 operating environment elevates networking from a commodity refresh to a strategic inflection point. Organizations that align procurement, site strategy, and operations with the architecture demands of AI and the realities of constrained power and supply chains will convert competitive pressure into durable advantage.

PW Consulting’s full Data Center Network Market report provides the granular segmentation, vendor-specific forecasts, and downloadable models required to operationalize the insights summarized here. Visit our research portal to access the comprehensive datasets, request a tailored briefing, or engage our advisory team for custom scenario modeling and vendor negotiation support.

For detailed analysis of this topic, please visit the official page:Data Center Network Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com