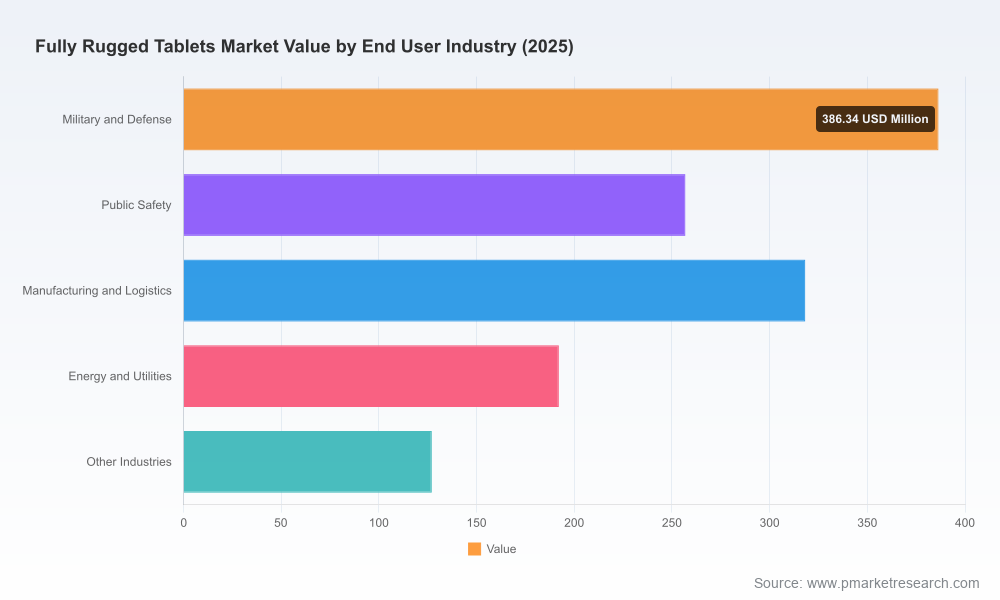

Fully Rugged Tablets Market: PW Consulting’s 2026 Strategic Briefing for Enterprise Decision-Makers

PW Consulting’s newly released market research on Fully Rugged Tablets delivers a focused, decision-ready intelligence package designed to guide procurement, product, and strategy teams as they plan for 2026 and beyond. Built on a base year of 2025 with a historical baseline covering 2020–2025 and a forecast horizon to 2032, the study quantifies a market that expanded steadily over the past half-decade and is set to continue growing at a compound annual growth rate (CAGR) of 7.35% through the forecast period. The brief below synthesizes the report’s strategic value, highlights dynamics that will shape vendor and buyer behavior in 2026, and outlines the practical tools included in the full deliverable—while intentionally reserving the granular segment and regional revenue tables to the full report.

Fully Rugged Tablets Market

Why this report matters for 2026 decisions

2026 is a pivot point for organizations that deploy computing power at the operational edge: emergency services that must balance durability with connectivity, defense programs pressed to meet updated environmental qualifications, and industrial operators optimizing field workflows. PW Consulting’s analysis makes three short-term, actionable assertions that should influence budgeting and vendor selection this year:

Fully Rugged Tablets Market

- Market momentum supports continued vendor investment: aggregate market sizing shows meaningful expansion from the early 2020s into 2026, providing suppliers room to innovate while also attracting new entrants and OEM consolidation.

- Consolidation is material and persistent: the top-tier vendors capture a majority of market revenues, indicating concentrated competitive dynamics that favor proven platforms and scale advantages.

- Supply-chain and regulatory headwinds will be defining constraints: lead-time variability for core components, new test requirements for defense-grade equipment, and export controls will influence availability, specs, and pricing in 2026.

What the PW Consulting report delivers (practical, operational content)

The full report is built to be operationally useful to technology sourcing teams, product managers, and C-suite strategists. Key deliverables include:

Fully Rugged Tablets Market

- Integrated market sizing and trajectories: annualized market totals from 2020 through 2032 with scenario bands that reflect supply, demand, and regulatory variance.

- Competitive scorecards: vendor benchmarking across durability certifications, security certifications, service footprints, total cost of ownership (TCO) constructs, and platform roadmaps.

- Procurement playbooks: RFP templates, risk allocation clauses for long lead-time components, and recommended warranty and support terms for field-deployed fleets.

- Technical decision frameworks: guidance on selecting operating systems, connectivity stacks (including 5G), modular battery and accessory strategies, and lifecycle upgrade paths that minimize downtime.

- Supply-chain risk matrix and mitigation protocols: triangulated analysis of supplier concentration, component lead-time volatility, and actionable mitigation steps such as dual-sourcing and strategic inventory buffers.

- Regulatory-impact analysis: mapping of standards (including recent updates) to procurement and qualification workflows for defense, public safety, and regulated industrial deployments.

- Use-case driven TCO models and deployment case studies: modeled outcomes for patrol fleets, field service teams, and heavy industry operators that illuminate real-world payback horizons.

To respect the “trailer” principle, this briefing demonstrates PW Consulting’s analytical depth while directing readers to the full report for the underlying segment and regional breakouts, which include granular revenue and adoption metrics used to build the TCO and procurement templates.

Competitive landscape: what enterprises must know about vendors

The fully rugged tablet market is populated by established OEMs with distinct strengths. Our assessment highlights how each vendor’s capabilities translate into procurement advantages and potential risks for large-scale deployments in 2026.

- Getac (Taiwan): Continues to lead innovation with large-screen form factors and cutting‑edge processors. Recent product introductions incorporate Intel’s latest mobile silicon and higher ingress resistance, positioning Getac well for defense and industrial applications where performance and survivability both matter.

- Panasonic (Japan): The Toughbook lineage remains a benchmark for field durability. Recent iterations emphasize connectivity and battery life enhancements that appeal to public safety and logistics users who need sustained operations rather than peak compute.

- Dell (USA): Dell’s rugged Latitude line differentiates via enterprise security certifications and tightly integrated support services—attributes that matter to government and regulated enterprises seeking certified architectures for sensitive workloads.

- HP (USA): HP’s approach blends ruggedized hardware with enterprise lifecycle services and financing options, addressing buyers that prefer vendor-managed refresh programs.

- Zebra / Xplore Technologies (USA): Focused on verticalized solutions, this portfolio pairs rugged hardware with industry-specific ruggedization and software integrations, particularly in energy, utilities, and field services.

- DT Research and MobileDemand (USA): Niche-focused OEMs that offer specialized features—hot-swappable batteries, barcode/scanning integration, and compact footprints—that provide pragmatic alternatives for specific operational profiles.

The market’s concentration profile—where the top three and top five vendors command a substantial share of revenues—has practical implications. Buyers gain negotiating leverage from the scale and certification portfolios of leading OEMs, but over-reliance on a small set of suppliers raises exposure to component scarcity and geopolitical constraints discussed below.

Dynamics shaping 2026 supply and specs

Four discrete dynamics will shape procurement outcomes in 2026:

- Component lead times and supply constraints: High demand for industrial-grade processors has extended lead times significantly; procurement cycles must allow for 20–24 week waits for certain Intel mobile chips unless alternate architectures or earlier locking of purchase orders are pursued.

- Standards and certification changes: The 2024 update to environmental qualification standards demands stricter thermal and vibration testing. Organizations deploying in defense and similarly demanding environments must budget for extended qualification time and possible design iterations.

- Geopolitical export controls: Recent controls on high-end semiconductors create conditional supply corridors to certain markets. Buyers with cross-border deployments or manufacturing footprints must integrate compliance checks early in vendor selection.

- Raw-material cost pressure: Input cost increases—such as an elevated price for specialty display glass—are compressing margins and influencing vendor pricing strategies as well as design trade-offs between ruggedity and weight or cost.

Strategic recommendations for 2026

For enterprise leaders planning capital and operational spending in 2026, PW Consulting recommends a two-track approach blending immediate operational resilience with medium-term strategic positioning.

- Immediate (next 6–12 months)

- Harden procurement timelines: build component lead-time buffers into project plans and secure priority allocations via framework agreements.

- Prioritize certified platforms: require vendors to demonstrate compliance with the updated environmental standards and, where applicable, relevant security certifications.

- Diversify vendor mix by role: match highly certified, premium devices to mission‑critical roles while deploying cost-effective, rugged-lite units for lower-risk tasks.

- Medium-term (12–36 months)

- Invest in modularity and upgradeability: favor platforms that allow CPU, modem, and battery upgrades to mitigate obsolescence and component scarcity risk.

- Negotiate service-led deals: leverage vendor consolidation to secure lifecycle management, including remote diagnostics and rapid field swap programs.

- Incorporate geopolitical risk assessments into sourcing decisions: map alternative supplier pathways and certify secondary manufacturing sources.

How the report supports tactical execution

Beyond high-level strategy, PW Consulting provides practical artifacts that teams can drop into project workflows: pre-populated RFP language for durability and security tests, vendor scorecards tailored to use case priorities, example TCO models contrasting leasing versus outright purchase, and a prioritized checklist for procurement approvals under constrained supply. These elements reduce time-to-decision and improve defensibility of capital plans for finance and compliance stakeholders.

Next steps and where to find the deep data

This briefing is designed to be a strategic preview. The full PW Consulting report contains the granular segmentation, regional breakdowns, pricing curves, and vendor-specific revenue estimates used to create the models and templates summarized here. For sourcing teams and executive sponsors preparing 2026 budgets, the complete dataset and interactive scenario tools are essential to convert these strategic recommendations into executable procurement actions.

To obtain the full report, vendor scorecards, and interactive TCO models, contact PW Consulting’s research desk or visit our publications page for access options and tailored briefing sessions.

For detailed analysis of this topic, please visit the official page:Fully Rugged Tablets Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com