Integrated Optical Delay Line Market — Strategic Preview for 2026 Decisions

PW Consulting’s new market research on Integrated Optical Delay Lines (IODLs) synthesizes the technology, commercial, and regulatory inflection points that will shape executive choices in 2026. Built on a rigorous historical baseline (2020–2025) and a forward-looking forecast horizon (2026–2032), the study maps where value is forming across materials platforms, product architectures, and end-markets. This briefing highlights the report’s strategic value, the headline macro trajectory (to inform budgeting and M&A sizing), and the actionable playbook executives should apply when making capital, partnership, and product decisions next year. Core segmentation tables and vendor-level financial breakdowns are intentionally reserved for the full report to enable this piece to act as a high-value “trailer” while driving readers to the published study for complete, transaction-grade detail.

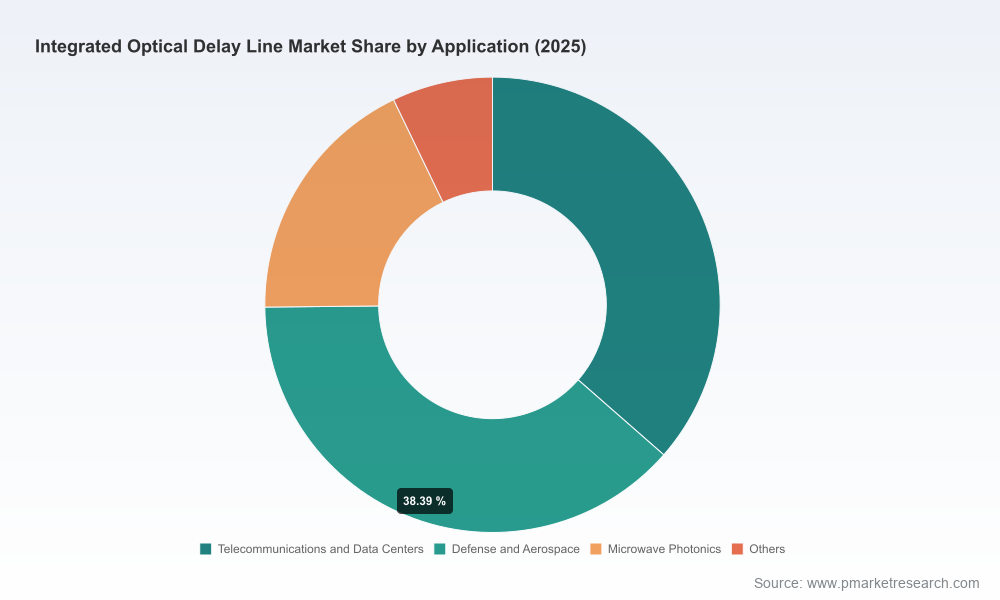

Integrated Optical Delay Line Market

Market Snapshot: Macro Trajectory You Need to Budget For

The integrated optical delay line market has recorded steady growth through the 2020–2025 period and continues its expansion into the forecast window. On a total-market basis, our compiled figures indicate the market expanded from an earlier base in 2020 and reached a 2025 baseline of approximately USD 420.5 Million. Looking to 2026, the market is poised to grow further, and over the 2026–2032 forecast period our conservative scenario models a compound annual growth rate (CAGR) of 7.5%, taking the market toward roughly USD 697.6 Million by 2032 under the base forecast.

Integrated Optical Delay Line Market

Two observations flow directly from this macro trajectory and should inform 2026 planning cycles:

Integrated Optical Delay Line Market

- Scale and timing: the near-term uplift in 2026 supports investments in pilot production capacity and low-risk integration programs (foundry runs, assembly automation, and packaging validation) rather than immediate large-scale capex for mass production.

- Opportunity window: the market size and growth rate are sufficiently attractive to justify selective M&A and strategic partnerships, particularly for players seeking differentiated IP in materials (e.g., silicon photonics, lithium niobate) or system-level integration capabilities for RF and quantum interfaces.

Why This Report Matters for 2026 Corporate Decisions

Executives face four linked uncertainties when allocating 2026 budgets in photonics: technology choice, supply-chain resilience, regulatory exposure, and addressable-commercial demand timing. Our report converts those uncertainties into decision-ready guidance by combining:

- Quantitative market sizing and scenario modelling across 2026–2032 (to set realistic revenue and ROI estimates for product roadmaps and M&A diligence);

- Technology readiness and manufacturability assessments that pinpoint where unit economics will improve materially (e.g., substrates, waveguide loss targets, and foundry process maturity);

- Competitive landscaping at the component and system level, including patent positioning and recent strategic moves; and

- Regulatory and export-control risk matrices to factor into go-to-market and partner selection strategies.

For CFOs and strategy teams, the most direct value is immediate: use the 2026 forecast band and sensitivity scenarios in the report to stress-test business plans, vendor commitments, and integration timelines before committing to high-cost R&D or capacity expansions.

Report Contents — Practical & Transaction-Ready

The full study is structured for usage by commercial, product, and corporate development teams. Highlights of the actionable content include:

- Executive summary with investment implications and go/no-go thresholds for new programs;

- Macro market model (historical 2020–2025, base year 2025) with bottom-up and top-down reconciliations and multiple forecast scenarios to accommodate conservative, base, and accelerated adoption pathways;

- Technology deep dives covering silicon photonics, lithium niobate, fiber-integrated approaches, and emerging hybrid platforms — each evaluated for insertion loss, footprint, thermal stability, and manufacturability;

- Supply-chain and foundry landscape analysis, including MPW access strategies and recommended process nodes and mask-scheduling approaches for rapid prototyping;

- Commercial segmentation and willingness-to-pay studies (note: granular segmentation tables are available only in the full report);

- Competitive profiles, IP mapping, and M&A targets prioritized by strategic fit and integration complexity;

- Regulatory and standards appendix covering export-control impacts, IEEE standardization developments, and compliance checklists for dual-use applications;

- Strategic playbooks for product managers, business development leads, and corporate development teams, including 12–24 month roadmaps, partnership frameworks, and a scorecard for supplier selection.

Competitive Landscape — Who’s Moving and Why It Matters

Understanding vendor capabilities and their recent strategic moves is essential for supplier selection, co-development decisions, and integration risk assessments. The market shows moderate concentration, with top-tier vendors holding a meaningful share of customer relationships and system-level expertise (our concentration analysis indicates a three-firm concentration index and a five-firm index that together reflect a market where scale and IP matter). Key vendor archetypes include:

- Specialized PLC and long-delay innovators — vendors offering ultra-long integrated delay lines in compact form factors, well-suited to LiDAR, telecom, and sensing pilots; notable for their ability to trade delay density for footprint efficiency.

- Large diversified research-led players — multinational research labs and corporations pushing electro-optic transducers and integrated delay solutions for high-precision applications such as quantum transduction and microwave-to-optical conversions.

- RF and radar system integrators — companies delivering packaged photonic delay systems optimized for RF/microwave bandwidths, with integration capabilities that reduce system provider time-to-market.

- Module and assembly specialists — suppliers focused on high-reliability optical assemblies, small-form-factor variable delay modules, and GUI-controlled systems for rapid adoption in mixed optical-RF environments.

Recent, illustrative developments we analyzed include:

- A strategic partnership announced in March 2025 between a PLC specialist and an optics systems provider to supply long-delay PLC chips for next-generation FMCW LiDAR — an example of product-to-system co-development that shortens the OEM validation cycle;

- A patent grant in early 2025 to a large research-driven corporation covering electro-optic transduction architectures with integrated delay lines — signaling continued defensive IP buildup around quantum and microwave-photonic interfaces;

- An academic-industry demonstration of multimode-enabled silicon photonic delay lines that pushes delay-density limits for broadband tunable operation — demonstrating the type of bench-to-fab transition that can rapidly change cost and performance assumptions.

Regulation, Foundry Access, and Material Constraints — Non-Product Risks to Manage

Executives must plan around three non-product risks that frequently derail commercialization timetables:

- Standards and performance requirements: emerging IEEE guidance emphasizes low-loss, thermally stable waveguides — compliance here materially affects product architecture and cost target decisions.

- Export-control exposure: advanced delay precision for radar and quantum systems may attract export restrictions; treat market expansion into dual-use geographies as a legal and strategic decision that must be incorporated into commercial planning.

- Foundry and materials availability: silicon-on-insulator and silicon nitride remain the primary substrates for low-loss waveguides; access to MPW runs and the right process nodes determines whether a roadmap can meet the 2026 pilot schedules.

Strategic Playbook — Practical Moves for 2026

Based on the macro outlook and vendor dynamics, PW Consulting recommends the following prioritized actions for corporate leadership teams planning 2026 allocations:

- Prioritize flexible pilot investments over large capex: fund multiple small-scale prototyping runs with preferred foundries to de-risk process variability and accelerate qualification cycles.

- Lock strategically complementary partnerships: pursue co-development with packaging and RF-integration specialists to reduce system risk and shorten integration timelines for telecom and LiDAR customers.

- Protect critical IP and navigate export risk early: conduct IP landscaping and export-control impact assessments before opening cross-border engagements in sensitive technology areas.

- Design modular product roadmaps: favor architectures that allow swapping substrate or delay-density modules so you can pivot as the cost/benefit of material platforms evolves.

- Target bolt-on acquisitions and minority investments: use the 2026 funding window to secure niche capabilities (long-delay PLC expertise, high-resolution switching, or electro-optic transduction) that complement your roadmap.

How to Use This Research in Your 2026 Planning Cycle

Use PW Consulting’s full report as the single source for aligning product line P&Ls, M&A scorecards, and supplier SLAs against validated market scenarios. The executive teams that pair tactical moves (foundry MPW scheduling, packaging co-development) with strategic hedges (IP protection, export-control compliance) will capture the earliest adopter segments while insulating long-term scale plays.

To preserve the strategic advantage for our clients, detailed regional and application-level breakdowns, vendor financials, and downloadable model workbooks are available exclusively in the full report. That content includes the granular segmentation tables, price and ASP trend assumptions, and unit shipment forecasts necessary for transaction-level modelling.

Next Steps

If your 2026 plans involve new product introductions, supplier commitments, or M&A in photonics, PW Consulting’s full Integrated Optical Delay Line Market report supplies the scenario models, vendor heat maps, and regulatory checklists you will need to execute with confidence. Contact our advisory team to schedule a briefing and obtain the downloadable model pack and executive summary.

For detailed analysis of this topic, please visit the official page:Integrated Optical Delay Line Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com