Semiconductor TMAH Developer Market: Strategic Imperatives for 2026 Decision-Makers

Executive preview — why this report matters for 2026 planning

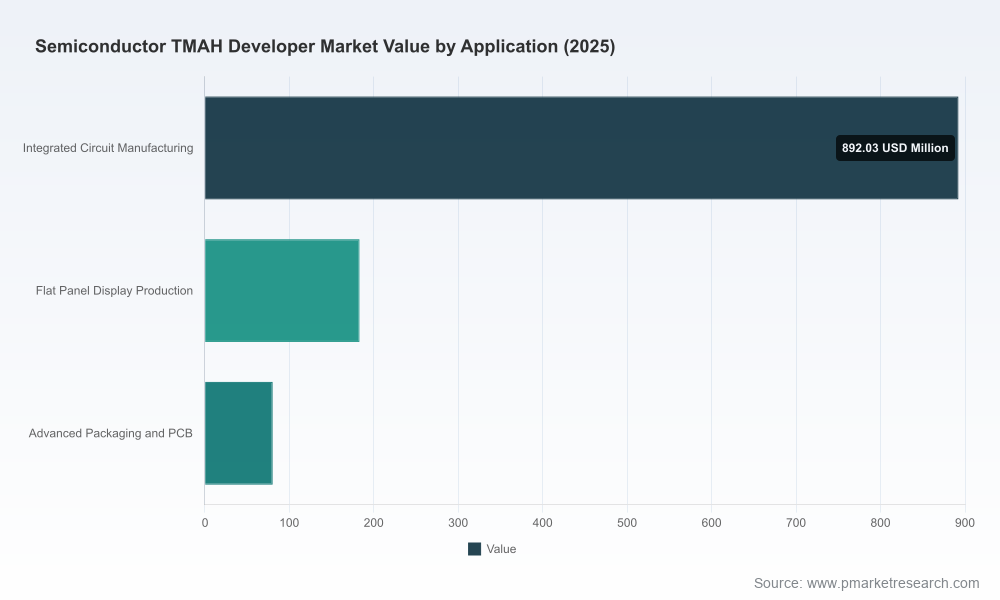

PW Consulting’s new Semiconductor TMAH Developer Market report is designed as a strategic playbook for executives making critical sourcing, manufacturing, sustainability and M&A decisions in 2026. The market for tetramethylammonium hydroxide (TMAH) based developers has demonstrated steady expansion since 2020 and is projected to accelerate through the coming decade. After growing from a sub‑billion dollar market in 2020 to USD 1,155.4 Million in 2025, our model forecasts an increase to USD 1,981.45 Million by 2032 — a compounded annual growth rate of 8.01% across the forecast window. This trajectory reflects strengthening demand across advanced logic, foundry, and display lithography, while changing regulatory and circularity imperatives are reshaping supplier economics and capital priorities.

Semiconductor TMAH Developer Market

What you will get from the report (practical, operational deliverables)

- Actionable supply‑chain diagnostics — supplier scorecards, geopolitical supply‑risk mapping, and sourcing levers calibrated to advanced‑node purity and logistics constraints.

- CapEx and capacity planning framework — a decision matrix to balance brownfield expansions, toll‑manufacturing, and near‑shoring of purification assets under tariff and trade‑policy scenarios.

- Commercial playbook — pricing model templates, contracting strategies (volume, take‑or‑pay, recycling credits), and working‑capital stress tests for 12–36 month procurement cycles.

- Circularity and waste management pathway — technical and commercial guidance to implement closed‑loop TMAH recycling at fab scale, including expected recycling penetration breakpoints and capex/opex sensitivities.

- Regulatory and environmental compliance roadmap — prioritized actions to meet evolving wastewater and chemical handling regulations, including treatment technologies for recalcitrant TMAH streams.

- Scenario models — three investment and sourcing scenarios (Base, Accelerated Recycling, and Supply Shock) with decision triggers and quantified P&L impacts for manufacturers, suppliers and traders.

Market dynamics shaping 2026 decisions

Several structural forces converge in 2026 to create both risk and opportunity in the TMAH developer market:

Semiconductor TMAH Developer Market

- Technology-driven purity demand: Advanced lithography and tighter line-width budgets increase the non‑negotiable purity requirements for wet-process chemistries. Suppliers that have invested in chlorine‑free, sealed production lines and integrated TMAC feedstocks are better positioned to supply high‑purity electronic‑grade solutions.

- Circularity as a cost and risk lever: Leading fabs are piloting and scaling electronic‑grade TMAH recycling to reduce fresh‑chemical purchases, lower waste disposal costs, and mitigate supply volatility. Recycling pathways change unit economics and shift bargaining power between fabs and commodity producers.

- Trade policy and near‑shoring: Recent tariff actions on photoresist inputs and related chemistries have triggered supply‑chain diversification. Expect continued investment in regional purification and blending assets as companies reduce first‑tier import exposure.

- Concentration and supplier power: The market exhibits measurable concentration at the top end of global supply. This creates pockets of supplier leverage — but also opportunities for nimble midsized players to capture niche, high‑value segments via technical differentiation and local presence.

- Sustainability and wastewater treatment: TMAH wastewater is chemically persistent and requires specialized handling; regulatory scrutiny is increasing. Capital investments in treatment and safe recycling infrastructure are moving from discretionary to mandatory in many jurisdictions.

Competitive landscape — how to read supplier strength and strategic fit

Our report includes an empirical competitive assessment and supplier playbook covering legacy producers, specialty chemical houses and regional entrants. At a high level:

Semiconductor TMAH Developer Market

- Incumbent specialty suppliers with established ultrapurity credentials and multiple manufacturing bases maintain advantaged access to leading fabs via long technical relationships and validated quality systems. These firms are preferred partners where qualification cycles and contamination risk are primary concerns.

- Integrated chemical groups that produce electronic‑grade feedstocks and operate sealed, chlorine‑free supply chains can offer cost advantages and vertical control — attractive for customers considering near‑shoring or long‑term offtake arrangements.

- Regional manufacturers and newer entrants are competing on speed‑to‑market, localized inventory and flexible contract terms; they are particularly relevant where tariffs and lead‑time constraints limit reliance on global incumbents.

PW Consulting’s assessment quantifies market concentration metrics and competitive intensity — and explains why concentration matters for price volatility, qualification timelines and contingency planning. (For detailed supplier scorecards and validation‑level comparisons, see the full report.)

Recent developments that materially affect 2026 strategies

- Fab‑scale recycling initiatives are moving from pilots to deployment. Leading semiconductor manufacturers have announced multi‑year programs to recycle electronic‑grade TMAH at scale, which will materially reduce fresh purchases under certain adoption curves. Buyers and suppliers must jointly define recycle‑credit accounting and quality assurance mechanisms.

- Capacity additions in Asia are accelerating to address high‑purity demand for display and semiconductor fabs; this changes near‑term availability and pricing dynamics, and can alter regional trade flows.

- Updated product technical notes from several manufacturers show incremental improvements in developer formulations and performance for pattern resolution — underscoring the importance of co‑development and early access to next‑generation chemistries.

2026 playbook — recommended actions by function

- Procurement: Implement a dual‑track sourcing strategy — secure validated long‑term supplies for critical fabs while maintaining a flexible pool of regional suppliers for buffer capacity. Introduce recycling clauses and performance‑based rebates into master supply agreements.

- Operations/Manufacturing: Invest in modular purification/blending capabilities adjacent to fabs to shorten validation cycles and reduce import exposure. Pilot on‑site recycling with conservative quality gates and traceability protocols before scale roll‑out.

- Finance and Strategy: Model the ROI of recycling investments under three adoption curves and incorporate tariff sensitivities into capital allocation decisions. Consider earn‑outs or minority investments in regional TMAH producers to secure preferential access.

- R&D and Quality: Create cross‑functional qualification teams to accelerate supplier validation and reduce time‑to‑production for alternative developers and blends, including metal‑ion‑free formulations and buffered chemistries.

- ESG and Compliance: Prioritize wastewater handling and worker‑safety investments; align chemical reuse metrics with corporate sustainability targets. Prepare for more stringent discharge limits and community scrutiny.

Scenario thinking — the decision triggers we model

Our forecast includes three actionable scenarios relevant to 2026 decision-makers:

- Base Case: Continued growth in fabs and displays; steady improvement in recycling adoption; supply tightness relieved by incremental capacity additions.

- Accelerated Recycling: Faster fab adoption of closed‑loop systems reduces fresh purchases materially and changes supplier revenue mix toward services and reclamation credits.

- Supply Shock: Trade disruptions or contamination events force rapid near‑shoring and premium pricing; firms without validated second‑source options incur qualification delays.

Each scenario in the report maps to clear operational triggers — inventory days, recycle penetration thresholds, qualification lead times — so executives can convert strategic intent into executable contingency plans.

Why PW Consulting’s insights matter now

2026 is a pivotal year: investments made now in recycling pilots, regional purification assets and supplier integration will determine cost curves and supply resilience into the 2030 horizon. The market’s projected rise from USD 1,155.4 Million in 2025 toward nearly USD 2.0 Billion by 2032 at an 8.01% CAGR is not merely growth in demand; it is a re‑shaping of the value chain — from raw‑material producers and specialty formulators to fab operators who increasingly control reuse and reclamation economics.

Next steps — how to use this intelligence

- Download the full PW Consulting report to access the granular regional and application breakdowns, supplier scorecards, and the interactive scenario models that underpin our forecasts.

- Initiate a 90‑day supplier risk review using our template to identify critical single‑source exposures and prioritize immediate mitigations.

- Run the report’s recycled‑material sensitivity model against your procurement budget to quantify the break‑even horizon for on‑site recycling versus long‑term contracts.

PW Consulting’s Semiconductor TMAH Developer Market report is tailored to provide the empirical foundation and pragmatic tools executives need in 2026 to navigate rising purity requirements, evolving trade dynamics, and the emergence of circular chemical supply models. For detailed tables, supplier rankings, and the full set of forecasts and models — including the granular segmentation that informs strategic supplier selection — access the full report on our website.

For detailed analysis of this topic, please visit the official page:Semiconductor TMAH Developer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com