PW Consulting Releases Strategic Brief: Nappa Leather Market Outlook and Decision Playbook for 2026

Why this report matters for leaders planning 2026 moves

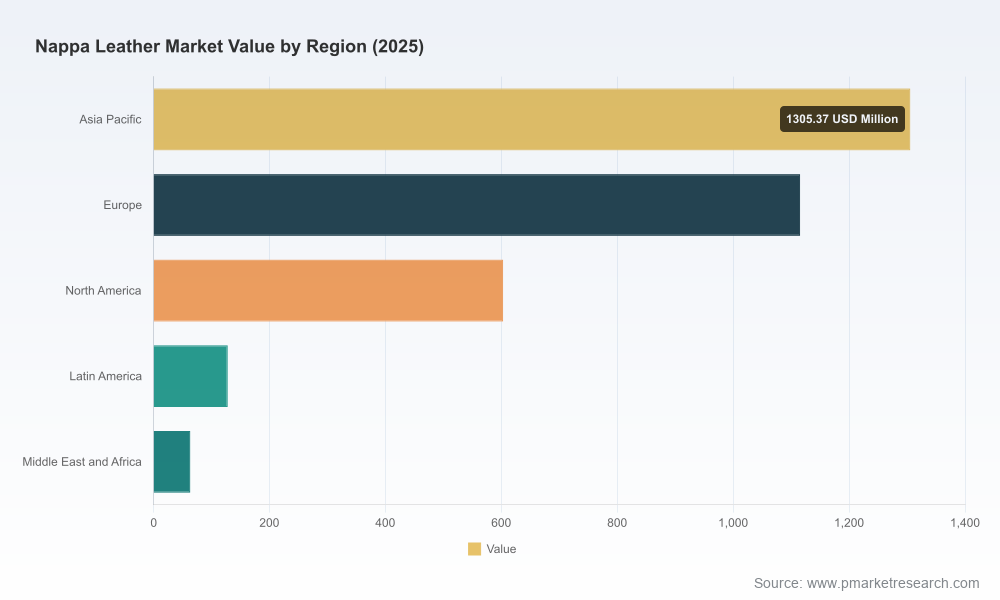

As companies prepare budgets, supply agreements, and product roadmaps for 2026, the Nappa leather value chain faces converging forces — steady end-market demand, evolving raw-material economics, tightening regulation, and rapid differentiation by sustainability and finishing technologies. PW Consulting’s new Nappa Leather Market Report synthesizes a distilled, commercially actionable view of these dynamics. At the macro level, the market is recovering from pandemic-era dislocations and is projected to expand from a 2025 baseline of approximately USD 3,215 million to roughly USD 4,591 million by 2032, representing a forecast-period compound annual growth rate of about 5.22% (forecast period: 2026–2032). That topline trajectory frames near-term investment and procurement choices: growth is real, but it is concentrated in product and service differentiation rather than simple volume wins.

Nappa Leather Market

Headline themes shaping 2026 decisions

- Demand maturation in premium applications: Automotive OEMs and high-end furniture and fashion houses are increasing specification of Nappa leather for premium trims and limited-run models. Recent model announcements and concept integrations — from major OEMs adopting Nappa as a standard or featured option, to concept vehicles using synthetic Nappa-like alternatives — illustrate both sustained traditional demand and openness to material innovation.

- Sustainability as a market divider: Certification, traceability, and lower-impact tanning processes are moving from brand differentiators to procurement prerequisites in high-margin segments. Leading tanneries are investing in traceability platforms and chemical-use monitoring to maintain access to global OEM and luxury-brand buyers.

- Regulatory inflection points: Regulatory measures that restrict specific tanning chemistries or processing additives are on the near-term horizon; companies must embed compliance strategies into capital and sourcing plans now to avoid disruption after enforcement dates in late 2026 and beyond.

- Raw-material and cost structure pressures: Hide-price volatility, logistics cost variability, and energy-intensity in processing keep margins sensitive to supply-chain design and vertical integration choices. Benchmarks in the report help map sensitivity of finished Nappa cost to hide-price changes and processing yields.

- Innovation in synthesis and finishing: Novel synthetic Nappa-like materials are being demonstrated in premium segments, challenging incumbents on performance, cost, and sustainability narratives. Tanneries that can pair advanced finishing with validated sustainability metrics preserve value against synthetic competition.

Strategic implications for corporate decision-makers in 2026

For executives tasked with P&L, procurement, product, and sustainability strategy, the 2026 planning cycle is an opportunity to move from reactive compliance to proactive positioning. Specific implications we emphasize in the report include:

Nappa Leather Market

- Supply security trumps lowest-cost buying: Given hide-price swings and localized capacity constraints, multi-sourcing strategies and long-term offtake arrangements with tiered quality bands reduce risk and protect premium product launches.

- Certification and traceability enable premium pricing: Investments in LWG/OEKO-TEX alignment, supplier audits, and chain-of-custody systems increase access to luxury OEM programs and reduce commercial friction for global distribution.

- CapEx and equipment planning must factor regulatory timelines: Upcoming bans and tighter equipment standards mean retrofit and replacement windows are narrow; capital allocation that anticipates regulation yields lower risk and near-term bargaining power.

- Product portfolio choreography: Brands should map Nappa leather SKUs alongside synthetic alternatives to control margin erosion while preserving brand equity in leather-forward collections.

Competitive landscape — who to watch and why

The sector remains commercially diverse, spanning artisanal tanneries, large-scale bovine processors, and premium suppliers specialized in high-performance automotive grades. The players to monitor fall into four competitive archetypes:

Nappa Leather Market

- Premium, sustainability-led specialists: Companies with advanced traceability, closed-loop processes, and sustainability certifications are capturing high-margin opportunities in luxury, aviation, and top-trim automotive interiors. Their proposition blends craft, environmental credentials, and bespoke finishing.

- Large-scale commodity suppliers: Integrated processors with substantial wet-blue and crust capacity compete on scale, breadth, and global distribution — instrumental for OEMs and footwear brands that require volume continuity.

- Technical/automotive-focused tanneries: Firms that partner closely with vehicle OEMs on durability, colorfastness, and flammability compliance win long-term platform business through engineering alignment.

- Synthetic/material innovators: New entrants and material-science firms push the envelope on Nappa-like synthetics, capturing attention from concept vehicle programs and younger consumer cohorts sensitive to animal-welfare narratives.

Our competitive profiles in the report provide tailored strategic takeaways for each major player segment and examine representative companies across geographies. Examples of companies covered include established European and North American premium tanneries known for craftsmanship and automotive capability, large South American producers with scale benefits, and Asian manufacturers that combine cost competitiveness with localized market access. Each profile highlights core strengths — from tanning technology and traceability to scale and product verticals — and identifies likely strategic moves through 2028.

Regulatory and raw-material dynamics that need board-level attention

- Regulation: Regulatory actions targeting specific processing additives, and new compliance obligations under regional chemical-control regimes, create a clear fence-line of risk that must be integrated into supplier contracts and capital plans. One near-term example is the prohibition on certain isopropylated phosphate compounds in U.S. commerce beginning in late 2026; while this targets articles and parts of the supply chain, its operational impacts cascade into equipment, finishing chemistry procurement, and third-party processing relationships.

- Raw materials: Chrome tanning remains the dominant industrial route for achieving the soft, pliable characteristics of Nappa leather for many applications; leather buyers continue to reference hide-price ranges and grade differentials when structuring sourcing tiers. Understanding the mechanics of tanning yields, splitting losses, and finishing add-ons is essential to model delivered cost at scale.

- Certifications: ISO 14001, OEKO-TEX and Leather Working Group alignment are increasingly treated as commercial prerequisites; buyers exclude non-certified suppliers from premium RFQs and platform bids.

What PW Consulting’s report delivers (practical, ready-to-use content)

The report is built as a decision-support toolkit rather than an academic exercise. Key deliverables include:

- Topline market sizing and seven-year forecast models with scenario sensitivity to hide prices, energy costs, and substitution rates.

- Segment view and actionable segmentation frameworks by application, product type, and region (note: detailed split tables and downloadable datasets are available in the full report).

- Supplier landscaping with strategic profiles, capability matrices, and M&A heatmaps tailored to buyers, private-equity investors and OEM sourcing teams.

- Regulatory impact assessment and compliance playbook for operational and sourcing transitions tied to 2026 enforcement timetables.

- Cost-model templates that translate hide-price and process variables into finished-leather unit economics for bid and sourcing scenarios.

- Go-to-market and product-differentiation playbooks for brands considering blends of natural and synthetic Nappa across price tiers.

- Case studies and procurement clauses that can be adapted for supplier agreements, including sample audit checklists and sustainability KPIs.

How to use the report in your 90/180/360-day plan

- 90 days: Run a supplier risk-mapping exercise using the report’s supplier matrix; prioritize audits for any suppliers that lack traceability or necessary certifications. Begin re-negotiations on offtake clauses to include regulatory remediation provisions.

- 180 days: Finalize CapEx allocation for processing equipment retrofits or partner with certified tanneries to secure platform-level supply; pilot synthetic Nappa options in a limited product run to test consumer resonance and total cost implications.

- 360 days: Lock strategic partnerships for sustainability initiatives, roll out traceability dashboards for end customers, and align product roadmaps to the forecasted demand pockets identified by scenario models.

Why PW Consulting’s perspective is unique

Our analysis combines primary interviews across the leather value chain, proprietary cost and yield modeling, and scenario-driven market forecasts. We overlay technical process knowledge (from raw hide pricing mechanics to chrome-tanning yields and finishing-loss drivers) with commercial channel intelligence (OEM trim cycles, furniture procurement calendars, and fashion-season dynamics). That combination produces not just forecasts, but executable playbooks — including contract language, audit checklists, and near-term scenario actions tailored for 2026 decision windows.

Next steps — where to find the full intelligence

This release is intentionally selective: core segmented tables, granular regional and application splits, and downloadable modeling files are reserved for the full report and accompanying data pack. Executives seeking the datasets needed to run procurement models, M&A diligence, or product-cost simulations should consult the complete report for the detailed annexes and vendor-level disclosures that power our scenario tools.

To access the full Nappa Leather Market Report, strategic tools, and data templates, visit PW Consulting’s market reports page or contact our industry practice lead for a briefing. The 2026 planning cycle is already underway — firms that translate this market intelligence into procurement, compliance, and product decisions will gain measurable advantage.

For detailed analysis of this topic, please visit the official page:Nappa Leather Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com