Mahadev Books - Learn to balance risk and reward in betting decisions

Games |

2026-03-31 18:40:15

PW Consulting is pleased to announce the release of our latest market research report, “Bone Cement for Spine Market: Strategic Outlook 2026–2032.” This briefing summarizes the report’s strategic value for executive teams preparing 2026 plans and highlights the practical, decision-grade insights the full study delivers. The spine augmentation bone cement market continues to expand steadily; our analysis synthesizes macro growth dynamics, competitive strategy implications, regulatory inflection points, and operational risks that will determine winners and laggards as providers invest in product innovation, market access, and manufacturing scale.

Bone Cement for Spine Market

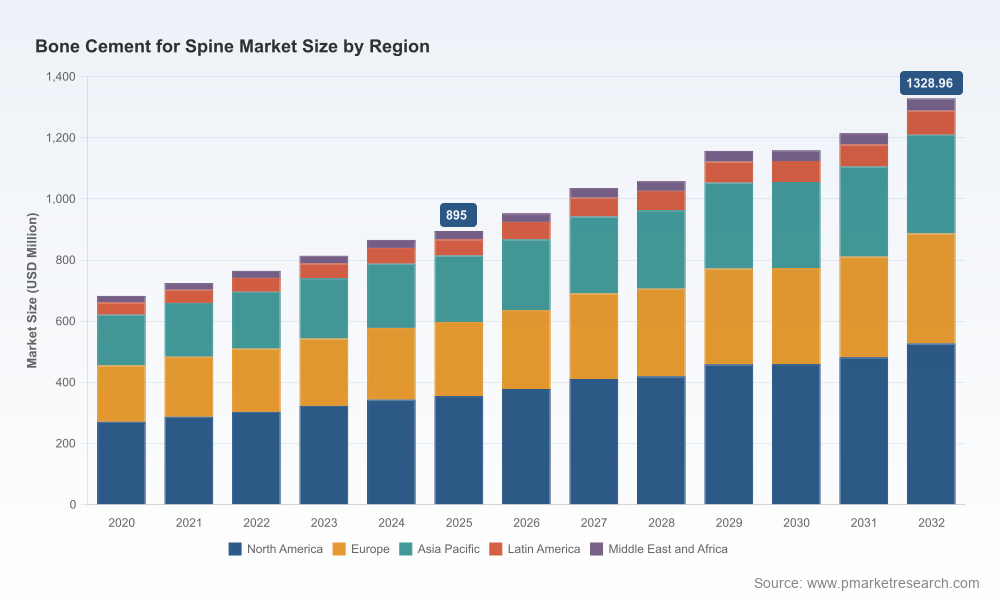

Scale and trajectory: Using 2025 as the analytical base year, our model shows the global bone cement for spine market has grown materially since 2020 and is forecast to continue that expansion through 2032. The report quantifies the market in USD (Million) and projects a compound annual growth rate (CAGR) of 5.81% across the 2026–2032 forecast horizon.

Bone Cement for Spine Market

Near-term construct for planning: The market is large enough to support multiple commercial propositions — from high-volume standard PMMA offerings to premium, differentiated chemistries and systems — while remaining concentrated enough that strategic moves by a handful of established players materially shift competitive dynamics.

Bone Cement for Spine Market

Concentration metrics: Market concentration is meaningful, with the three-largest competitors capturing a majority share and the top five accounting for roughly three quarters of market value. This concentration creates both barriers and opportunities: scale advantages in distribution, regulatory leverage, and pricing power versus niches for innovators addressing clinician demands and unmet clinical needs.

Actionable market model: A transparent, spreadsheet-ready market model calibrated to PW Consulting’s proprietary inputs and public sources, enabling scenario runs across pricing, adoption curves, reimbursement changes, and product launches.

Segmentation framework: High-resolution demand drivers and adoption archetypes by clinical procedure, product chemistry, and route-to-market — presented to inform portfolio prioritization without exposing commercially sensitive granular data in this release.

Go-to-market playbooks: Tailored commercial strategies for incumbent large-cap medtech players, fast-follow mid-sized innovators, and early-stage disruptors — covering direct sales vs. distributor models, key account targeting, and clinical evidence sequencing.

Regulatory and reimbursement navigators: Step-by-step decision aids mapping FDA classifications and relevant CPT billing pathways that materially affect procedure economics and hospital adoption. These include the device classification context and typical reimbursement codes clinicians and hospitals cite for vertebral augmentation procedures.

Manufacturing and quality checklist: Practical guidance on sterilization strategy, supplier qualification, and quality attributes that buyers prioritize — including sterility assurance level (SAL) expectations and common pyrogenicity documentation practices.

M&A and partnership playbook: Valuation heuristics and deal archetypes derived from concentration dynamics, recent clearances, and product launches that have reshaped the competitive map.

The market’s competitive fabric combines large, diversified orthopedics and spine players with specialized bone cement manufacturers and systems companies. Established medical device leaders bring scale in distribution, hospital relationships, and integrated procedure platforms. Specialist firms focus on chemistry differentiation (e.g., high-viscosity PMMA formulations), delivery systems tuned to vertebroplasty/kyphoplasty workflows, and clinical support programs that accelerate adoption.

Large incumbents: Multi-billion-dollar orthopedics groups remain central to commercialization, leveraging existing spine portfolios and account relationships to secure formulary inclusion and bundled procedure positioning.

Specialists and systems players: A cluster of focused companies competes on formulation nuances (e.g., viscosity profiles, radiopacity, antibiotic loading), delivery methods (controlled injection systems, RF-modulated heating), and regulatory pathways such as 510(k) clearances that open U.S. market access.

Recent strategic moves: The industry saw notable 510(k) clearances and product launches in the recent 12–24 months that demonstrate how targeted regulatory wins and tactical product introductions can change competitive momentum. These developments also underscore the practical importance of an integrated regulatory-commercial plan when launching in the U.S. and other advanced markets.

Chemistry dominance and differentiation: PMMA continues to serve as the clinical workhorse owing to well-understood mechanical properties and clinician familiarity. That said, differentiated formulations (viscosity-tailored, long-working-time, radiopaque, and antibiotic-loaded variants) are increasingly critical for segmenting product offerings.

Delivery systems as competitive moats: The pairing of cement formulations with delivery and augmentation systems (including tools that improve handling, reduce leakage risk, or integrate with imaging systems) is a high-impact area for product strategy and bundling.

Clinical evidence sequencing: For many hospital systems, incremental clinical data on safety (e.g., leakage rates), handling, and outcomes matter more than lab metrics. Faster, pragmatic trial designs and registry participation are effective, lower-cost ways to build the necessary data package for adoption.

Regulatory classification: PMMA bone cement used in vertebral augmentation is regulated within established device classifications and subject to special controls in several key markets. Successful market entry requires foresight on permissible claims, sterility validation, and design controls that map to official guidance documents.

Reimbursement levers: Procedure-level CPT pathways exist that cover percutaneous vertebral augmentation. Strategic engagement with payers and hospital coding specialists to ensure appropriate coding and capture of ancillary fees (e.g., imaging guidance, device billing practices) materially affects revenue realization and hospital willingness to adopt new products.

Quality and sterility expectations: Sterilization method selection and documentation (e.g., EtO vs. radiation), pyrogen testing, and demonstrating an SAL aligned with regulatory expectations are non-negotiable. These elements influence both time-to-market and buyer confidence.

Raw material performance: Standard PMMA formulations exhibit compressive strength well above commonly referenced regulatory minima, but batch consistency and supplier qualification remain essential. Material sourcing strategies should balance cost, quality, and single-source risk.

Capacity and scale: Given the market’s growth trajectory and concentration, manufacturers should assess whether to invest in expanded production capacity or to pursue contract manufacturing relationships to meet demand spikes tied to successful launches or seasonal procedure volumes.

Quality systems as a differentiator: Robust quality management, accelerated complaint resolution, and clear sterilization validation not only support regulatory compliance but also reduce hospital adoption friction.

With the top tier of competitors holding a sizable share of the market, M&A and licensing remain powerful routes to scale. Strategic buyers should consider three deal archetypes: bolt-on acquisitions to add complementary delivery systems or chemistries; geographic expansion deals that accelerate local market entry; and conditional licensing arrangements that pair novel formulations with established distribution networks. Timing matters: regulatory clearances and initial clinical adoption materially affect valuation multiples.

Prioritize portfolio clarity: Identify one or two product propositions (e.g., high-viscosity PMMA for oncologic vertebral fractures; antibiotic-loaded variants for infection-prone indications) to move from concept to regulatory submission within a 12–18 month window.

Accelerate regulatory readiness: Finalize sterility approach, pyrogen testing plans, and risk files upfront to compress 510(k)-type timelines where applicable.

Engage commercial proof points early: Secure registry partnerships and pragmatic clinical studies aimed at the hospital purchasing committee and interventionalist early adopters to shorten adoption cycles.

Stress-test supply chain: Qualify alternate suppliers for critical monomers and radiopacifiers; evaluate contract manufacturing partners with proven SAL documentation capabilities.

Evaluate inorganic options: Use concentration metrics and our scenario tools to identify adjacencies where acquisition or licensing unlocks immediate commercial scale or improves margin profile.

PW Consulting’s study combines proprietary primary interviews, device clearance databases, procedure-volume estimates, and supplier price dynamics. The base year for calibration is 2025, with historical data spanning 2020–2025 and a detailed forecast for 2026–2032. The model and recommendations are designed for use by strategy teams, corporate development units, and R&D leaders who require quantitative scenarios tied to practical go-to-market sequencing.

In keeping with our “trailer” principle — demonstrating analytical depth while reserving the most actionable granular segment and regional figures for report subscribers — this briefing intentionally omits detailed regional and application-level splits. The full report provides those breakouts, including downloadable models and sensitivity analyses that are essential for detailed budgeting, valuation, and deal structuring.

As hospital systems seek efficiency and clinicians demand safer, easier-to-handle materials, the bone cement for spine market is positioned for steady, predictable growth. For organizations planning their 2026 investments, the right mix of regulatory foresight, focused clinical evidence, and supply-chain rigor will determine whether a product secures rapid adoption or languishes on hospital shelves. PW Consulting’s report offers the quantitative models and tactical playbooks to convert market tailwinds into commercial outcomes.

Access the full report to unlock the detailed segmentation, downloadable financial model, and playbooks described here. PW Consulting clients can request a briefing with our lead analysts to walk through scenario runs tailored to their portfolio.

Contact PW Consulting’s Spine & Orthopedics practice to schedule a strategic workshop aimed at converting the report’s insights into a 12–24 month execution roadmap.

For detailed analysis of this topic, please visit the official page:Bone Cement for Spine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com