Aflibercept Market: Insights, Key Players, and Growth Analysis

Other |

2026-05-27 07:52:11

As PW Consulting releases its latest IoT MCU Market report, executives and product leaders face a pivotal planning horizon. The embedded controller landscape is moving from device-enablement to ecosystem enablement — and companies that align procurement, platform strategy, and compliance roadmaps in 2026 will capture disproportionate value over the next business cycle. Our report projects a sustained market expansion at roughly a 9.0% compound annual growth rate (CAGR) across the 2026–2032 forecast window, with the total addressable market growing from a mid-2020s base to a substantially larger market by the end of the decade. These macro trends set the strategic frame for capital allocation, supplier selection, and product roadmaps for the year ahead.

Iot Mcu Market

Consolidation and concentration: The market exhibits meaningful concentration among the top-tier suppliers — a structural reality that affects bargaining power, roadmap alignment, and supply risk. Our analysis shows the top three and top five firms command a sizable share of industry revenue, making their product and compliance choices determinative for platform-level interoperability and standards adoption.

Iot Mcu Market

Security and regulation are non-negotiable: New regulatory and certification initiatives (from both regional and global bodies) are redefining minimum compliance baselines for wireless, device identity, and lifecycle security. Firms that bake compliance and certification into their 2026 product delivery will avoid costly redesigns and gain first-mover advantage into premium channels.

Iot Mcu Market

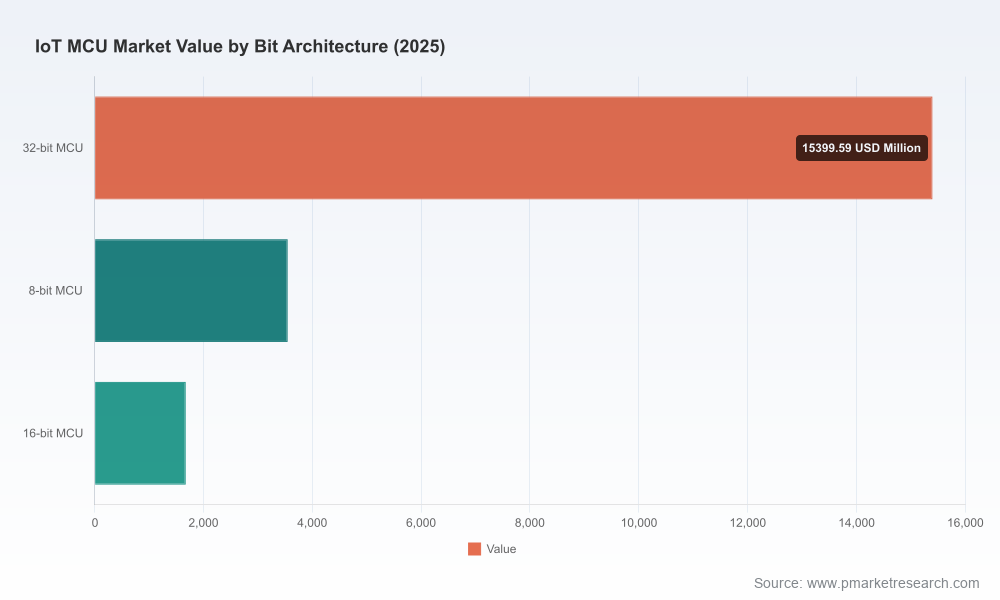

Technology bifurcation accelerates: While low-cost, ultra-low-power 8-bit and 16-bit solutions remain relevant for constrained nodes, the industrialization of edge compute and the rise of integrated connectivity (dual-band Wi‑Fi, multi-protocol wireless, and hardware trust anchors) are driving adoption of higher-performance 32-bit architectures in new use cases.

The published report is purpose-built to be a strategic decision tool for 2026. It combines market sizing and a 2026–2032 forecast, vendor scorecards, regulatory trend analysis, product roadmap implications, and executable go-to-market playbooks. Key practical deliverables include:

Scenario-driven demand models that translate macro adoption curves into SKU-level BOM and margin impact for both OEMs and ODMs;

Supplier risk matrices and contingency plans that map concentration risk to sourcing levers, dual-sourcing feasibility, and near-term inventory actions;

Compliance checklists and engineering requirements tied to Matter, ETSI/ISO baselines, regional labeling programs, and radio directives — enabling cross-functional teams to operationalize certification pathways;

Vendor capability profiles and pragmatic vendor shortlists tailored to use-case archetypes (e.g., battery-powered sensors, industrial edge nodes, consumer smart home gateways);

Time-phased investment and capability roadmaps for hardware, firmware, and platform toolchains that align to product launch windows in 2026–2027.

To preserve the strategic value of this intelligence and encourage direct engagement with the datasets, the report intentionally omits granular subsegment dollar breakdowns in this public summary. Subscribers and clients receive the full regional, application, and architecture splits alongside downloadable Excel models and sensitivity scenarios.

The competitive map is diverse yet structured: global system houses, analog/mixed-signal incumbents, wireless-specialist vendors, and aggressive cost-driven entrants all pursue differentiated plays. PW Consulting’s synthesis of vendor moves yields a concise strategic read for 2026:

NXP Semiconductors — ecosystem and certification-focused. NXP’s strategy centers on crossover MCUs and silicon that accelerate certification paths (e.g., Matter compliance) and integrate robust wireless stacks. For enterprises prioritizing ecosystem interoperability and certified SDKs, NXP represents a low-friction integration partner.

STMicroelectronics — breadth and developer momentum. ST’s STM32 portfolio continues to trade on developer familiarity and extensive middleware ecosystems. Their wireless-enabled lines and LoRaWAN capabilities make them attractive for volume IoT platforms that require predictable supply and broad toolchain support.

Infineon Technologies — security and power integration. Infineon’s emphasis on secure roots-of-trust, power management, and industrial-grade reliability positions it strongly for mission-critical IoT projects where safety, power efficiency, and long lifecycle support are paramount.

Microchip Technology — high performance analog and niche compute. Microchip’s recent high-speed MCU introductions underline its strategy to capture math-intensive, mixed-signal, and edge-AI workloads in industrial and medical IoT segments.

Renesas Electronics — wireless convergence. Renesas’ recent launches of dual-band Wi‑Fi and Wi‑Fi/BLE MCUs underscore a bet on consolidated wireless connectivity in consumer and connected home deployments, simplifying integration for OEMs targeting multi-radio capability.

Texas Instruments — ultra-low-power leadership. TI remains the default for deeply constrained sensor applications that demand extreme power efficiency and long battery life.

Silicon Labs, Espressif, Nordic — wireless specialists. These firms differentiate through multi‑protocol support, innovation in low-power radio stacks, and cost-optimized wireless platforms that enable rapid time-to-market for smart home, wearables, and sensor networks.

Analog Devices, Broadcom, Nuvoton and regional players — vertical specialization. From precision analog integration for sensing to cost-focused MCUs for consumer appliances, these players are executing on vertical-specific value propositions that complement the broader incumbents.

Recent product moves reinforce these dynamics: Renesas’ late‑2025 dual-band Wi‑Fi MCUs and Microchip’s 200 MHz high-performance PIC32A family are emblematic of two concurrent waves — integration of richer connectivity and rising MCU compute capability for edge inferencing. For purchasers and platform teams, these introductions change BOM economics and feature trade-offs for 2026 releases.

Matter and connectivity certification programs: silicon vendors increasingly position their MCUs with validated stacks and certification pathways. Choosing silicon that reduces software integration time for Matter and similar ecosystems is a quantifiable time‑to‑market lever.

Regional security mandates and labeling: emerging programs such as voluntary cyber labeling and stronger device-security mandates (aligned to NIST/ISO baselines) mean engineering teams must allocate budget for secure boot, update infrastructure, and third-party testing earlier in the design cycle.

Radio and privacy directives: new European radio equipment directives and national security frameworks alter the compliance timeline for wireless MCUs, particularly those with dual-band Wi‑Fi and cellular features. Proactive regulatory planning reduces rework risk and protects market access in major geographies.

Fast-track compliance and firmware hygiene: allocate funding in Q1–Q2 2026 for secure firmware development, OTA update architectures, and third-party certification pilots. These are now baseline requirements for meaningful commercial distribution in key markets.

Adopt a two-tier sourcing strategy: combine a primary partner with strong ecosystem and certification support and a secondary supplier that provides cost resilience or regional coverage. Use option contracts to lock lead times for new radio-enabled devices.

Revisit BOM and product segmentation: evaluate whether to migrate premium SKUs to higher-performance 32-bit MCUs to enable edge AI and enhanced security while retaining ultra-low-power variants for constrained nodes. Model margin impact under multiple supply-price scenarios.

Prioritize developer experience: choose silicon partners offering mature SDKs, reference designs, and cloud integration. Time-to-market is often driven less by raw silicon cost and more by software integration velocity.

Incorporate regulatory milestones into product roadmaps: map certification windows alongside hardware design cycles to avoid last-minute changes and shipment delays.

Consider strategic partnerships or tuck-in M&A: for companies seeking to accelerate connectivity or security capabilities, small acquisitions of middleware, secure element providers, or radio-stack teams can materially shorten time-to-competency.

Inventory assessment: audit existing designs for compliance gaps (secure boot, update capability, radio certification readiness).

Vendor engagement: run a rapid RFQ with top-tier vendors emphasizing certified stacks and supply continuity clauses.

Pilot certification: select one SKU and initiate a certification pilot path (Matter, regional cybersecurity labeling) to validate cost and timeline assumptions.

Scenario gating: update product‑level NPV/revenue scenarios using the report’s demand curves to identify which projects to accelerate or postpone based on ROI sensitivity.

PW Consulting’s IoT MCU Market report is designed to be the strategic backbone for these choices. The public summary lays out macro direction and near-term actions; the comprehensive dataset and vendor comparisons in the full report provide the tactical inputs required to execute. For teams planning capital allocation, supplier negotiations, or platform roadmaps in 2026, integrating these insights will materially reduce execution risk and shorten the path to market leadership.

To access the complete breakdowns, supplier scorecards, and downloadable scenario models that underpin the recommendations above, please visit the PW Consulting report landing page and request the subscriber deliverables.

For detailed analysis of this topic, please visit the official page:Iot Mcu Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com