Airport Transfers – Comfortable, Reliable & Stress-Free Travel Solutions

Other |

2026-04-22 16:20:20

PW Consulting’s latest Cartridge Systems Market report (base year 2025) delivers a forward-looking, practitioner-oriented intelligence package designed to inform procurement, product, manufacturing and corporate strategy decisions across the next investment cycle. The global market for cartridge systems reached approximately USD 1.92 billion in 2025 and, under our central scenario, is projected to expand at a compound annual growth rate (CAGR) of about 5.04% through the 2026–2032 forecast window, approaching roughly USD 2.73 billion by 2032. Our analysis synthesizes historical performance (2020–2025), near-term industry dynamics and seven-year scenario modelling to convert macro trends into executable playbooks.

Cartridge Systems Market

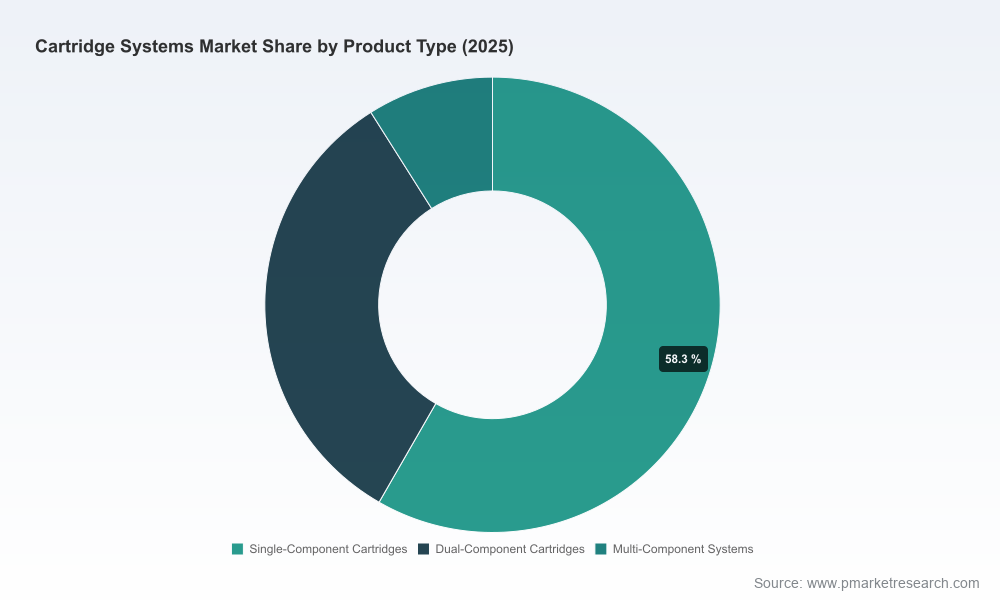

Actionable linkage between market growth and business levers. We translate headline market trajectories into concrete revenue and margin implications for product lines (single-component versus multi-component systems), end-market exposures (pharmaceuticals, industrial adhesives, electronics, and others) and manufacturing footprints.

Cartridge Systems Market

Risk-aware procurement guidance. The report identifies structural supply-chain vulnerabilities — from polymer feedstock volatility to regional processing bottlenecks — and provides hedging and sourcing strategies that can be implemented within 6–12 months.

Cartridge Systems Market

Sustainability and regulatory readiness. With customer and regulator pressure rising, we map viable pathways for incorporating recycled and biobased materials, aligning packaging solutions with upcoming pharma and packaging standards without compromising containment or performance.

M&A and portfolio optimization intelligence. The market shows moderate concentration at the top; our M&A playbook and target-scoring model prioritize acquisitions and divestitures that materially enhance capabilities, distribution reach, or technical differentiation.

Market model calibrated to 2020–2025 historicals and stress-tested across multiple macro scenarios for 2026–2032, enabling CFOs to run revenue, margin and payback simulations directly against their product portfolios.

Segment-level adoption curves and technology-readiness indices for dispensing formats (single-component cartridges, dual-component/2K systems, and multi-component solutions), together with investment thresholds for automation and integrated filling lines.

Supply-chain risk matrix and mitigation playbooks that quantify supplier concentration, criticality of polymer grades, and fill/finish capacity constraints—paired with tactical sourcing actions and supplier scorecards.

Pricing and margin sensitivity tools that link raw-material movements and mix shifts to bottom-line outcomes, with recommended commercial tactics for passing through costs while protecting volume.

Sustainability roadmap and case studies—covering PCR/PIR adoption, closed-loop recycling pilots and paper-based cartridge innovations—showing estimated CAPEX/OPEX trade-offs and customer acceptance pathways.

Competitive benchmarking and capability heatmaps for leading vendors, plus a regulatory and compliance checklist tailored to pharmaceutical primary packaging and industrial dispensing markets.

The cartridge systems market in 2026 sits at the intersection of three forces: steady end-market demand growth, accelerating sustainability requirements, and raw-material and processing cost dynamics that vary significantly by region. Demand drivers differ by end-use — pharmaceuticals continue to command premium requirements for sterility and containment, industrial adhesives and sealants prioritize dispensing precision and two-component systems, and electronics/automotive segments increasingly demand micro-dispensing accuracy and automated integration.

On the supply side, feedstock price volatility and regional divergence in polymer availability are exerting pressure on margins and forcing creative sourcing and design-for-material strategies. Meanwhile, an intensifying sustainability imperative is prompting both incumbents and challengers to pilot recycled-content cartridges, paper-based formats and design changes that reduce carbon and waste intensity without compromising critical performance attributes.

The market exhibits moderate top-end concentration, reflecting several global leaders that combine material science, precision manufacturing and regulatory know-how. The competitive map contains a mix of pharmaceutical-focused glass and primary-packaging specialists, industrial dispensing equipment providers, and system integrators that bridge filling, dispensing and downstream application.

Stevanato Group (Piombino Dese, Italy): Recognized for deep expertise in pharmaceutical glass cartridge systems and parenteral applications, Stevanato’s strengths include glass production scale and device integration for auto-injectors and on-body delivery. Their roadmap emphasizes containment performance and secondary-packaging sustainability pilots.

SCHOTT AG (SCHOTT Pharma, Mainz, Germany): A principal supplier of high-integrity glass primary packaging, SCHOTT’s focus on sterility and drug containment continues to make it a preferred partner for injectable drug manufacturers facing stringent regulatory scrutiny.

West Pharmaceutical Services (Exton, PA, USA): A leader in containment components and elastomeric solutions, West couples cartridge interfaces with sealing technologies and services that reduce extraction and compatibility risks for pharmaceutical clients.

Gerresheimer AG (Düsseldorf, Germany): With competency across glass and engineered plastics, Gerresheimer offers a flexible product mix for pharma customers looking to balance cost, performance and supply diversification.

Nordson EFD (East Providence, RI, USA): A specialist in industrial fluid dispensing, Nordson’s Optimum® cartridge platforms and dispensing systems are central to adhesives and electronics assembly segments that prioritize throughput and precision.

Sulzer Ltd / medmix (Mixpac): Notable for its 2K cartridge systems and a deliberate push on recycled-plastic options, medmix’s greenLine demonstrates an industrial pathway to reduce lifecycle emissions while retaining application performance.

Fischbach GmbH, AptarGroup, Nipro Corporation and Syntegon: Each plays a defined role—plastic cartridge components and filling systems, dispensing & sealing technology, regional pharmaceutical packaging supply, and ready-to-use filling equipment respectively—creating an ecosystem where partnerships and vertical integration are strategic advantages.

These profiles point to a market where engineering nuance, regulatory depth and supply-chain resilience are key differentiators. Consolidation remains selectively attractive: our concentration metrics indicate room for scale-driven moves while leaving space for vertical specialists and sustainability-focused new entrants to capture premium niches.

Material innovation is accelerating: industry players are publicly piloting recycled-content and paper-based cartridge formats and testing biopolymers in secondary packaging—moves that will shift supplier selection criteria for both industrial and pharmaceutical customers.

Commercial and trade show activity continue to spotlight sustainable inks and non-traditional printing technologies that enable graphic differentiation of cartridge packaging and further lifecycle gains.

Equipment suppliers are leaning into RTU (ready-to-use) filling and integrated dispensing automation, compressing the lead time from raw material to customer-ready systems and lowering contamination risk for pharma clients.

Procurement: short-listing criteria, dual-sourcing templates, and hedging options for polymer feedstocks.

R&D/Product: material substitution decision trees, test-protocol outlines for compatibilty and extractables/leachables, and rapid prototyping guidance for switching between glass, plastic and hybrid cartridges.

Manufacturing: automation ROI calculators for cartridge filling lines, recommended CapEx phasing, and floor-layout examples that reduce changeover time for multi-component operations.

Commercial: pricing playbooks for passing through raw-material inflation while maintaining competitive positioning, and channel strategies to support conversions to sustainable formats.

M&A and Corporate Strategy: target-screening matrix, integration checklists, and modeled synergies for five archetypal transactions.

Chief Procurement Officers: run supplier stress-tests using our supply-chain matrix this quarter; implement immediate dual-sourcing for critical polymers and engage in shared recycling initiatives with preferred suppliers.

Heads of Product and R&D: initiate at least one pilot for recycled-content cartridges or paper-based formats with a strategic customer within 12 months, leveraging our test-protocol templates to de-risk scale-up.

Operations and Supply-Chain Leaders: prioritize investments in RTU filling and modular automation where throughput bottlenecks map to high-margin product lines; use our CAPEX model to justify staged automation deployments.

Corporate Development Teams: use the report’s M&A target-scoring tool to identify acquisitions that either extend into high-value pharma containment or add differentiated dispensing IP for industrial applications.

PW Consulting’s Cartridge Systems Market report is designed as a catalytic tool for 2026 planning cycles—bridging market forecasting with pragmatic playbooks that move teams from insight to implementation. The full report contains the detailed segment tables, supplier scorecards, quantitative scenario outputs and downloadable Excel toolkits that we deliberately withhold from this preview to preserve the integrity of the proprietary models. For access to the complete dataset, segmented forecasts and the operational toolkits referenced here, please visit PW Consulting’s report page or contact our industry desk to arrange a briefing with one of our senior analysts.

For detailed analysis of this topic, please visit the official page:Cartridge Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com