Gum Arabic Market — Strategic Briefing for 2026: PW Consulting Intelligence Preview

PW Consulting’s newest Gum Arabic Market report delivers a concentrated, decision-ready briefing to inform corporate strategy and procurement planning for 2026 and beyond. Built on a validated historical series (2020–2025) and a multi-scenario outlook through 2032, the study synthesizes market-sizing, supply-chain risk mapping, regulatory implications, and actionable commercial playbooks. This preview highlights the report’s strategic value: it demonstrates the analytic depth you need to act in 2026 while purposely withholding the granular segmentation tables and line-item figures that are available in full on our platform.

Gum Arabic Market

Market trajectory: growth with structural volatility

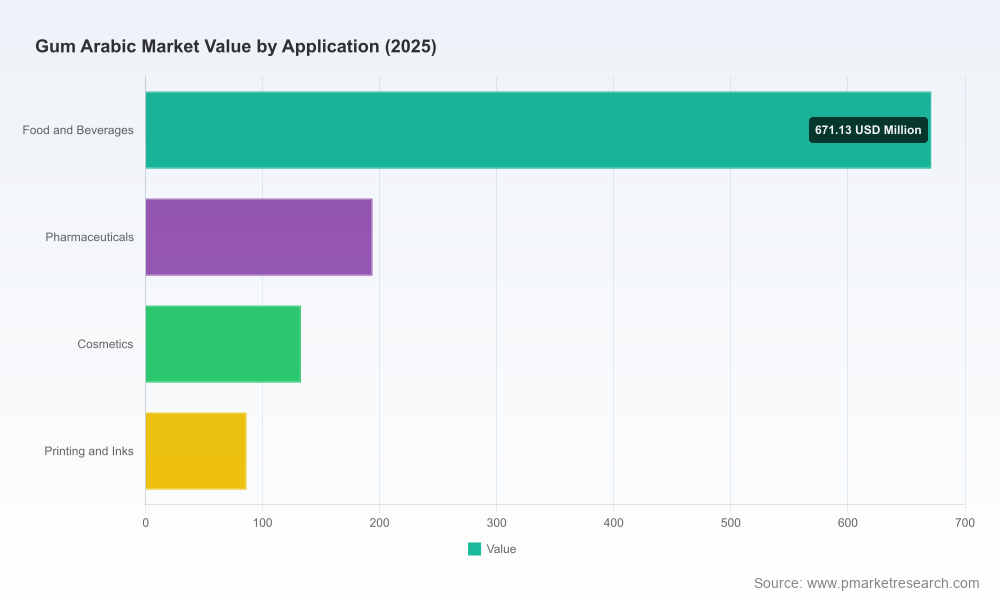

The gum arabic market has expanded from roughly USD 792 million in 2020 to an estimated USD 1,084 million in the report’s base year of 2025, reflecting resilient end-use demand and ongoing product innovation. Our forecast horizon (2026–2032) projects a compound annual growth rate (CAGR) of 6.54%, with the total market trending toward roughly USD 1.69 billion by 2032 under the central scenario. Those headline numbers hide an uneven path: short-term dips and rebounds driven by raw-material shocks and logistics interruptions coexist with long-term expansion driven by food & beverage, pharmaceuticals and specialty industrial applications.

Gum Arabic Market

Market concentration is meaningful but not prohibitive: the three- and five-firm concentration ratios indicate a market where leading processors and integrated suppliers exert influence, yet mid-sized and regional participants maintain viable commercial opportunities. That structure intensifies the value of tailored supplier strategies—both for buyers seeking security and for suppliers aiming to capture premium segments.

Gum Arabic Market

Key dynamics shaping strategic choices in 2026

- Geopolitics and raw-material risk: Conflict in traditional production zones has materially altered supply flows. The disruption has translated into export bottlenecks, muted formal volumes from some historical origins, and accelerated informal routes. The practical implication for 2026: buyers must treat sourcing as a strategic risk function, not a transactional activity.

- Price volatility and contract design: Recent cycles have shown wide price dispersion between commodity-grade and premium certified grades. Procurement teams should move beyond spot purchases to layered contracting approaches (short-term cover + strategic long-term offtakes + indexed clauses tied to verified price markers).

- Regulatory and quality gating: Regulatory frameworks—most notably existing European quality and microbiological standards—remain decisive market access factors. Compliance is a precondition for premium placement; traceability and documented processing controls are table stakes for exporters and processors targeting developed markets.

- Product innovation and substitution risk: Demand for clean-label stabilizers, micro-encapsulation agents, and specialty emulsifiers is driving R&D investment. New product formats (e.g., high-density granules, engineered spray-dried grades) and hybrid blends are emerging as margin-enhancing offers, but they also require formulation validation and supply-chain coordination.

- Sustainability as a commercial differentiator: Leading processors are investing in lower GHG intensity processing and village-level sourcing programs. Sustainability metrics are increasingly embedded in commercial terms—buyers will pay for verified social and environmental claims when they connect to brand value.

Competitive landscape — what the moves mean for your strategy

The competitive field is a mix of fully integrated global processors, specialized European spray-dryers, regional origin aggregators, and distributors focused on end-market access. Several strategic patterns are visible and material to 2026 planning:

- Vertical integration and traceable sourcing: Major processors that control sourcing hubs in the Sahel through to European finishing stages are leveraging vertical models to assure quality and traceability. This reduces counterparty risk for large food and nutrition buyers but can raise market access costs for smaller brands unless they form alliances or purchase cooperatives.

- Capacity expansions and product differentiation: Some legacy processors have announced capacity upgrades and new product formats to capture higher-margin use cases (e.g., high-density granules and certified spray-dried lines). These announcements matter for 2026 contract negotiations—suppliers with targeted capacity can execute on innovation-led price premia.

- Distribution partnerships and market reach: Strategic alliances between origin producers and regional distributors are accelerating market penetration in North American and Asia‑Pacific channels. For buyers, these partnerships mean faster qualification timelines for alternative origins.

- Regional origin players and raw-material aggregation: Origin aggregators and country-level exporters remain essential for supply continuity. Their access to local collectors and port logistics is a determinant of price and availability under stress scenarios.

Representative company positioning—summarized from our competitive audit—highlights the following archetypes: fully integrated global processors controlling the end-to-end chain; European specialists focused on premium spray-dried, certified grades; regional origin aggregators concentrating on raw material throughput; and branded ingredient houses packaging technical support and application know-how for specific end-markets. Each archetype demands a different engagement model from buyers and investors.

What the full report delivers — practical, operational tools

PW Consulting’s full Gum Arabic Market report is built for immediate operationalization. Key deliverables include:

- Validated historical series (2020–2025) and scenario-based forecasts (2026–2032) with sensitivities to geopolitical and demand shocks.

- Actionable procurement playbook: layered contracting templates, supplier qualification scorecards, and sample SLAs tailored for different grade classes.

- Supply‑chain risk heatmap and origin-vulnerability dashboard, with contingency routing and nearshore/alternative origin shortlists.

- Regulatory compliance checklist (including EU quality frameworks) and a ready-to-use quality-spec matrix for technical teams.

- Commercial benchmarking: supplier capability matrix, price banding guidance, and margin levers for ingredient formulators.

- A competitive database and company profiles with strategic implications for procurement, R&D, and M&A teams.

We designed these deliverables to be plug-and-play for 90-day roadmaps and to support mid-term strategic decision points such as contract renewals, RFP design, and bolt-on M&A evaluation.

Recommended actions for executives in 2026

- Initiate a 90‑day supplier risk audit: Map concentration exposure at the SKU level, identify single-source dependencies, and quantify replacement timelines for each material grade.

- Implement layered contracting: Combine short-term spot buffers with medium-term indexed contracts and selective long-term offtake agreements tied to verified sustainability metrics.

- Launch targeted supplier development pilots: Co-invest in traceability and quality upgrades with one or two upstream partners to secure priority access to certified grades.

- Prioritize regulatory readiness: Confirm that supplier documentation meets the EU and other key market regimes; build microbiological testing and certificate-of-analysis checks into the onboarding process.

- Fast-track formulation trials: Validate high-density and hybrid formats with R&D to capture functional advantages and assess cost-in-use versus incumbent solutions.

- Embed sustainability KPIs into procurement scorecards: Make verified village‑sourcing, GHG intensity per kg, and social compliance material to supplier selection.

Why this report matters to your 2026 agenda

2026 will be a year when procurement agility, supplier sophistication, and product innovation determine winners and losers in the gum arabic value chain. PW Consulting’s market model quantifies the macro runway and the sensitivity of that runway to shocks; the diagnostics reveal where real operational leverage sits; and the playbooks convert insight into executable steps. For corporations evaluating supply security, ingredient managers modernizing formulation, or investors sizing opportunities along the value chain, the full report surfaces the specific segmentation data, supplier financials, and price-path analytics needed to finalize commitments.

To access the complete segmentation tables, supplier profiles, and downloadable procurement templates that underpin these strategic recommendations, please visit our full report page. The preview above is intentionally high-level to demonstrate the analytical frame; the full intelligence package contains the granular figures and appendices required for contract-level decisions.

For detailed analysis of this topic, please visit the official page:Gum Arabic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com