Hdd Suspension Market: Strategic Imperatives for 2026 — Executive Preview

PW Consulting’s new Hdd Suspension Market study (base year 2025, forecast 2026–2032) delivers a decision-grade synthesis for executives who must translate component-level dynamics into enterprise strategy. The market has demonstrated steady expansion from the early 2020s and recorded a market value of USD 480.0 Million in 2025. Our model projects the industry to grow at a compound annual growth rate (CAGR) of 4.15% over the 2026–2032 forecast window, reaching an anticipated market size north of USD 630 Million by 2032 under the baseline scenario. This preview summarizes the report’s strategic utility for 2026 planning while intentionally reserving the granular subsegment matrices for the full report.

Hdd Suspension Market

Why this study matters for 2026 decisions

- Sourcing and supplier risk management: With a highly concentrated supplier base and recent supply-chain shocks, procurement teams must move from transactional buying to strategic partnerships. Our analysis quantifies concentration and supplier criticality and prescribes tiered mitigation strategies.

- Product roadmap alignment: HDD OEMs and actuator subsystem suppliers face diverging technology roadmaps (micro-actuators, PZT integration, flex-circuit advances). The study maps technology maturity against commercial adoption timing so product and platform teams can prioritize investments for near-term deployables vs. future-proofing initiatives.

- Operational footprint and reshoring choices: Geopolitical controls and rising labor costs in some Southeast Asian hubs are already reshaping where precision assembly occurs. We provide scenario-based guidance to optimize footprint decisions between cost, risk, and speed-to-market metrics.

- M&A and partnership playbook: Given the market’s high concentration at the top, the report identifies value-creation levers for acquirers and acquirables—capabilities that command a premium and those that are best kept as bolt-on targets.

- Procurement & component timing: Lead-time escalation for certain micro-actuators and rare clean-room-dependent processes requires revised inventory and qualification protocols. Our actionable timelines enable teams to avoid platform delays.

Market snapshot and topline dynamics

From 2020 through 2025 the market expanded overall, albeit with episodic volatility tied to raw material availability and OEM demand cycles. After a mid-decade adjustment, 2024–2025 re-established a growth baseline, culminating in the 2025 market value referenced above. Under our baseline forecast, the industry grows at a steady mid-single-digit CAGR (4.15%) between 2026 and 2032, driven by incremental capacity expansion in enterprise-class drives, continued demand for high-capacity storage, and the gradual adoption of advanced actuator technologies.

Hdd Suspension Market

Two structural features deserve emphasis. First, supplier concentration remains high: the top three and top five suppliers together command an outsized share of the market, creating both supply vulnerability and strategic leverage for leading OEMs. Second, the demand mix is bifurcating: incremental growth is being driven by enterprise storage and technology upgrades on higher-capacity platforms, while mature client and consumer segments remain more price-sensitive and capacity-driven.

Hdd Suspension Market

What the full report contains (practical, actionable modules)

- Market model and scenario suite: A transparent, auditable quantitative model (historical 2020–2025; forecasts 2026–2032) with base, upside, and downside scenarios, plus sensitivity levers for raw material shocks and equipment-export constraints.

- Demand-by-platform framework: An industry-vetted taxonomy linking suspension design choices to drive architecture, actuator types, and end-market economics.

- Supply-chain mapping and risk register: End-to-end supplier maps, critical-path components, lead-time profiles, and mitigation playbooks (dual sourcing, buffer strategies, co-investment approaches).

- Technology roadmaps: Comparative timelines for pico vs. nano suspension evolution, flex-circuit adoption, micro-actuator integration, and implications for test and qualification cycles.

- Competitive benchmark and scorecards: Operational KPIs, capacity footprints, quality certifications, and strategic positioning for the principal suppliers (corporate profiles, capability matrices, and recent moves).

- Commercial playbook: Pricing strategies, NPI engagement templates, qualification gating checklists, and long-term supply agreements optimized for HDD OEM negotiating teams.

- M&A and partnership heat-map: Identification of capability gaps, valuation levers, integration risks, and a prioritized list of target archetypes for strategic buyers and financial sponsors.

- Regulatory and compliance checklist: Practical steps to ensure production conformity with international cleanroom and environmental standards.

Competitive landscape — whom you should track and why

The market is dominated by a small set of highly capable suppliers that combine precision manufacturing, scale, and close OEM relationships. Our report provides a deep-dive on each of the key players and explains the strategic implications of recent moves:

- NHK Spring Co., Ltd. (Yokohama, Japan) — A leading global supplier with multi-country manufacturing reach and a demonstrated track record in next-generation suspensions. NHK’s recent product launch targeting very-high-capacity PMR drives underscores its R&D-led approach to maintain differentiation at the enterprise end of the market.

- Hutchinson Technology Incorporated (HTI) (Hutchinson, MN, USA) — Specialized in both traditional and advanced suspension assemblies, HTI’s supply agreements with major OEM platforms highlight its strategic role in enterprise HDD platforms and the importance of qualification timelines in winning long-duration contracts.

- Tatsuta Electric Wire & Cable Co., Ltd. (Osaka, Japan) — A supplier specializing in flex-circuit suspensions and actuator lead assemblies. Recent flex suspension upgrades demonstrate the interplay between interconnect design and platter-density scaling for client and niche enterprise applications.

- Suzhou Jinfu Precision Industry Co., Ltd. (Suzhou, China) — A high-volume component manufacturer serving OEMs with base plates and load beams; represents the scale-oriented, cost-competitive tier of the ecosystem and is sensitive to equipment export controls and tariff dynamics.

- Nippon Micro Metal Co., Ltd. (Osaka, Japan) — Precision metal supplier supplying critical subcomponents such as swagers and limiters; its role exemplifies the importance of tight tolerances and small-batch specialty manufacturing in the value chain.

Our competitive analysis includes qualitative and quantitative scorecards (quality yield, qualification speed, geographic diversification, intellectual property, and R&D pipeline) that allow OEMs and investors to prioritize engagement and capacity investments. Recent public developments — product launches, supply qualifications, and technology upgrades — are assessed for strategic impact on share dynamics and procurement negotiation posture.

Key risks and operational headwinds to incorporate into 2026 planning

- Raw material pressure: Stainless-steel strip costs for load beams have experienced material-year-on-year increases; procurement teams must revise cost-of-goods assumptions and explore alternative alloys or hedging strategies.

- Regulatory and quality compliance: ISO cleanroom standards (ISO 14644-1) are now explicit prerequisites for controlled manufacturing—noncompliance risks qualification delays and elevated scrap rates.

- Geopolitical constraints: Export controls on advanced manufacturing equipment can materially affect capacity expansion timelines in certain jurisdictions; scenario planning should include equipment re-basing and contingency investments.

- Labor and skills: Skilled assembly labor shortages and wage inflation in regional hubs are raising operating costs and creating capacity bottlenecks for precision assembly lines.

- Component lead-time risk: PZT micro-actuators and other actuator-critical components face extended lead times—orders for long-lead items should be placed earlier in the NPI cadence to avoid platform slippage.

Practical recommendations for 2026 corporate playbooks

- Procurement: Move from single-source spot buys to strategic multi-year commitments for long-lead components; include co-investment clauses for capacity expansion tied to order guarantees.

- R&D and product management: Adopt a “bimodal” development approach—short-cycle improvements for current platforms and parallel forward-looking projects to integrate micro-actuators as they reach maturity.

- Operations and footprint: Execute a phased geographic de-risking plan: retain core precision capacity near centers of excellence while building alternative, geographically diversified lines for high-volume, less-IP-sensitive subcomponents.

- Corporate development: Prioritize tuck-ins that fill capability gaps (micro-actuator integration, flex-circuit bonding expertise, or clean-room assembly capacity) rather than scale-only acquisitions.

- Risk and compliance: Operationalize an exports-and-compliance intelligence function to track equipment controls and certification timelines that affect qualification and ramp-up.

How to use this report

The full PW Consulting Hdd Suspension Market report converts the above insights into executable programs: supplier scorecards, procurement templates, an auditable forecast model, a prioritized M&A target list, and an operational checklist to accelerate supplier qualifications. For teams making mid-year budget allocations and 2026 roadmaps, the study is designed to reduce uncertainty around supplier commitments, to accelerate qualification milestones, and to prioritize investments that preserve optionality.

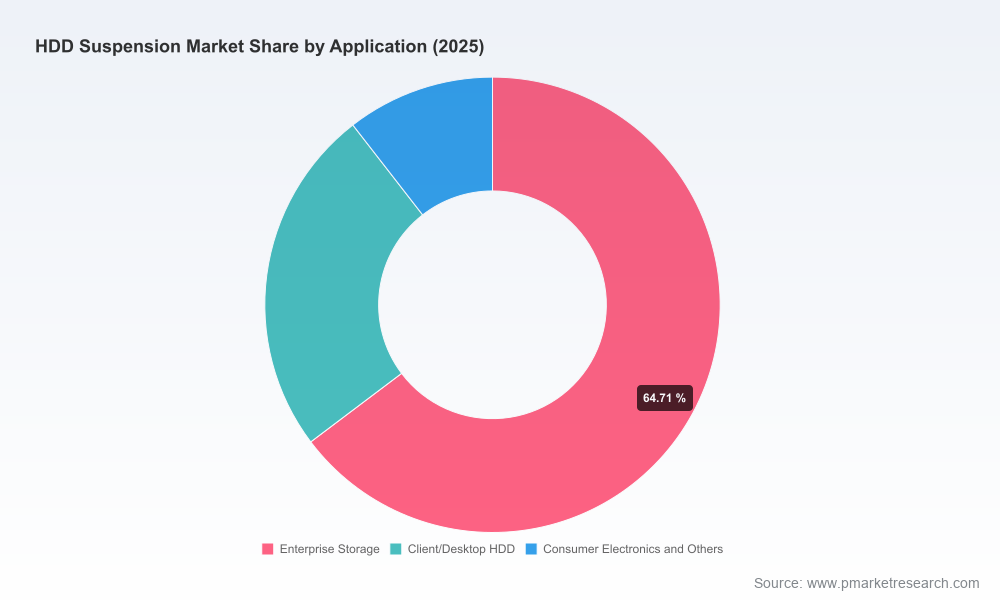

This preview intentionally omits the granular subsegment matrices and regional/application share tables; those detailed slices are central to the value of the full report and are available through our research portal. If you are evaluating supplier strategies, negotiating long-term supply agreements, preparing to acquire upstream capabilities, or revising product roadmaps for higher-capacity HDD platforms in 2026, the full analysis provides the evidence and templates required to act decisively.

Concluding note

For 2026, HDD suspension strategy is less about incremental cost cutting and more about system-level orchestration across technology, supply continuity, and regulatory compliance. With concentrated supplier power, heightened component lead times, and geopolitical pressure on equipment flows, manufacturing agility and forward planning will be the defining competitive advantages. PW Consulting’s Hdd Suspension Market report equips executives to convert component insights into enterprise-level strategy and to use procurement, R&D, and M&A levers in concert to secure durable advantage.

Contact PW Consulting to access the full report and the underlying market model, scenario tools, and supplier scorecards.

For detailed analysis of this topic, please visit the official page:Hdd Suspension Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com