Waist-Level Viewfinder Market: Strategic Imperatives for 2026 — PW Consulting Outlook

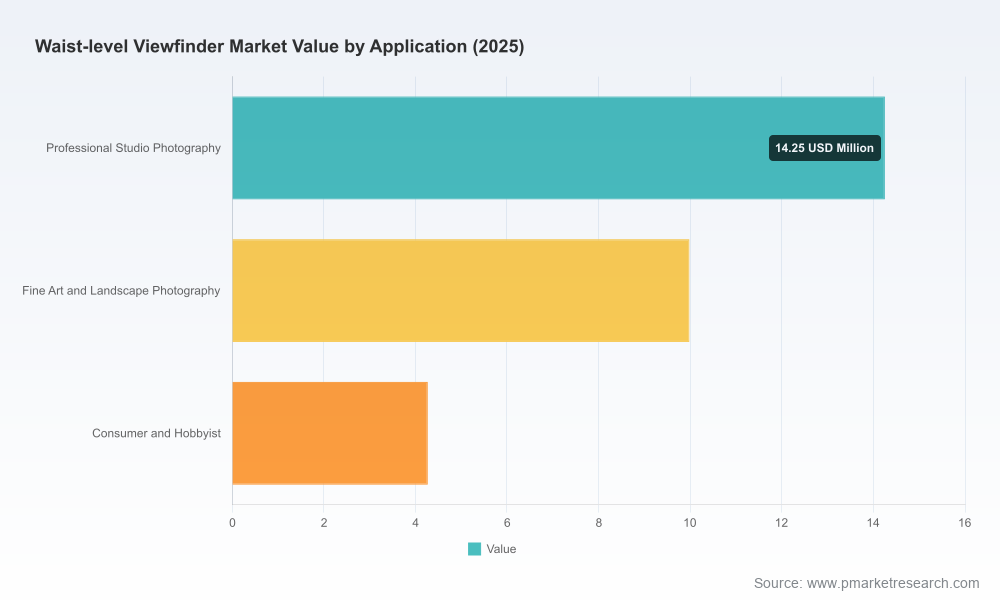

PW Consulting’s latest market study on the Waist-Level Viewfinder (WLV) market — base year 2025, historical window 2020–2025, forecast horizon 2026–2032 — provides executive teams with the high-resolution intelligence required for confident 2026 decision-making. The total market sits in the low‑tens of millions of USD (USD Million basis), with a modest but steady compound annual growth rate of 1.45% across the 2026–2032 forecast period. Our model projects a gradual expansion from a 2025 baseline to a mid‑thirty millions level by 2032, reflecting a market that is niche, resilient, and increasingly shaped by accessory ecosystems and retro-inspired innovation rather than mass consumer cycles.

Waist Level Viewfinder Market

Why this report matters for 2026 corporate strategy

- Clarity on a niche, specialist market: the WLV market is small in absolute terms but strategically disproportionate for medium-format manufacturers, mirrorless system suppliers, accessory OEMs and aftermarket specialists.

- Competitive inflection point: leading established brands and agile third-party suppliers are simultaneously defending heritage value and introducing low-cost, compatible accessories that broaden use cases.

- Timing for action: 2026 will be the year when prototype validation, limited product introductions, and channel experiments determine whether WLV moves from specialist curiosity to a sustainable accessory category.

- Risk calibration: the market’s low CAGR signals steady demand but also underscores exposure to commoditization, component sourcing volatility, and a concentration of aftermarket incumbents.

What PW Consulting’s report delivers (practical, decision-ready content)

Our study is intentionally action-oriented. Beyond market sizing and trend narratives, the deliverables include:

Waist Level Viewfinder Market

- Scenario-based financial models (2026–2032) with sensitivity testing for price, adoption rates, and channel mix — provided as editable spreadsheets designed for board-level stress testing.

- Go-to-market playbooks for three archetypal entrants: premium OEMs, mid-market accessory brands, and low-cost China-based suppliers — each featuring product roadmaps, channel partnerships, sample P&L thresholds, and launch checklists.

- Product development priorities based on primary interviews: mechanical tolerances, optical quality thresholds, ergonomics for studio use, and compatibility matrices for mirrorless mounts.

- Channel and distribution strategies with partner scorecards (retail, online D2C, specialty dealers, used-supply routes) and tailored margin models.

- Supplier and sourcing frameworks highlighting cost buckets, QC checkpoints, and a shortlist of vetted component and manufacturing partners.

- An executable M&A screening list identifying bolt-on accessory assets, IP-rich small makers, and aftermarket service providers — with acquisition heuristics and integration playbooks.

- Executive one-pagers and an investor-ready presentation summarizing levers that most materially affect unit economics and payback timelines.

To preserve competitive value for subscribers, detailed sub-segment tables (regional breakdowns, application splits, and unit-price matrices) are intentionally withheld from this press summary; they are available in full on the report landing page.

Waist Level Viewfinder Market

Market dynamics & industry signals shaping 2026

The WLV market is being redefined by two parallel currents: heritage-driven product revival from established camera makers and rapid productization by third-party accessory manufacturers.

- Primary OEM signaling: Canon’s showcase of two prototype digital cameras with waist-level optical viewfinders at CP+ 2026 — featuring mirror-based optical viewing and manual-focus tactile controls — is a pivotal industry signal. Canon’s prototyping activity validates user interest in tactile, analog-like shooting experiences within modern digital platforms and accelerates category legitimacy.

- Accessory market acceleration: Third-party suppliers have intensified activity. Recent launches from China-based manufacturers (notably two aluminum-bodied optical WLV accessories introduced in late 2025) demonstrate a cost-accessible path for mirrorless owners to adopt waist-level viewing. These products focus on universal cold-shoe compatibility, magnetic/flip hoods, and switchable framelines — features that prioritize ease-of-fit and low BOM cost.

- Aftermarket strength: Legacy medium-format ecosystems (supported by historical brands and a strong used-equipment market) continue to sustain premium WAIST viewfinder demand, while accessory makers expand reach into hobbyist and fine-art segments.

- Macro posture: With modest CAGR, the market rewards focused investment rather than broad diversification. Value capture will depend on differentiation (optical quality, brand, or service) and on the ability to control distribution and aftermarket touchpoints.

Competitive landscape: positioning, strengths and strategic moves

The report evaluates market players across brand equity, channel distribution, product breadth, innovation cadence, and unit economics. Highlights:

- Hasselblad (Gothenburg, Sweden): The archetypal premium incumbent. Hasselblad integrates waist-level viewing into its medium-format lineage and leverages brand premium, dealer relationships, and service economics. Strategic advantage: pricing power and a professional install base. Strategic challenge: scaling volumes outside high-end workflows.

- Ulanzi (China): Fast follower and scale-focused accessory OEM. Ulanzi’s recent VF01 launch exemplifies rapid, low-cost productization targeted at mirrorless users. Strategic advantage: speed-to-market and competitive cost structure. Strategic risk: margin compression and potential knock-on IP disputes as category matures.

- CHI / Chinotechs (China): Design-differentiated accessory builder. Their metal-bodied WLV introduced in late 2025 targets users seeking tactile, retro aesthetics at an accessible price point. Strategic opportunity: capture a mid-premium niche between legacy medium-format users and mass-market hobbyists.

- Reflx Lab (China): Compact universal WLVs with a focus on cross-platform compatibility. Strength lies in engineering simplicity and compatibility breadth — an attractive profile for OEM white-label partnerships and digital camera accessory bundles.

- Mamiya (Japan): Heritage manufacturer with residual traction in used and aftermarket channels. While not a volume driver today, Mamiya’s brand and legacy parts create monetization pathways via licensed accessories, limited reissues, and service packages.

- Canon (Tokyo, Japan): Strategic wildcard. Prototype activity at CP+ indicates potential to expand the total addressable market if Canon moves from concept to production. A production launch would both validate the category and place significant pressure on accessory makers to compete on integration and perceived value.

Market concentration is meaningful: the top three players account for a substantial majority of commercial value, and the top five extend that dominance further. This architecture creates high barriers in premium channels while leaving accessory and retrofit segments relatively open for agile entrants.

Strategic recommendations for 2026 (concise playbook)

- For incumbents (premium OEMs): Protect high-margin segments with bundled service agreements, limited-edition releases, and certified accessory programs. Use brand-led scarcity to deter low-cost substitution.

- For accessory entrants (China-based OEMs or design-focused shops): Prioritize compatibility and user experience over marginal feature proliferation. Win distribution via specialty retailers, influencer partnerships, and D2C kits. Consider white-label partnerships with mid-tier camera brands.

- For investors and corporate development teams: Target tuck-ins that provide IP on optical coupling, small-run manufacturing capacity, or brand equity in niche communities. Valuations should reflect the market’s low absolute size but durable monetizable aftermarket.

Next steps & how to access the full intelligence

PW Consulting’s full report includes the complete segmentation matrices, regional and application breakdowns, line-item revenue forecasts, dealer and OEM interview excerpts, and the downloadable financial model referenced above. These elements are intentionally omitted from this press summary to preserve client value and competitive sensitivity.

For strategy teams preparing budgets and product roadmaps in 2026, the choice is simple: treat the WLV category as a strategic niche with outsized brand and aftermarket value, and prioritize rapid validation of product-market fit, channel experimentation, and selective partnerships. PW Consulting’s full study provides the empirical tables, scenario models, and tactical playbooks to convert that strategy into executable plans.

Contact PW Consulting to license the full report and receive the editable forecasting model, go-to-market templates, and our prioritized list of M&A and partnership targets tailored to your strategic intent.

For detailed analysis of this topic, please visit the official page:Waist Level Viewfinder Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com