PW Consulting Strategic Brief: Anti‑Asthmatics & COPD Drugs Market — A 2026 Decision‑Making Playbook

Executive summary

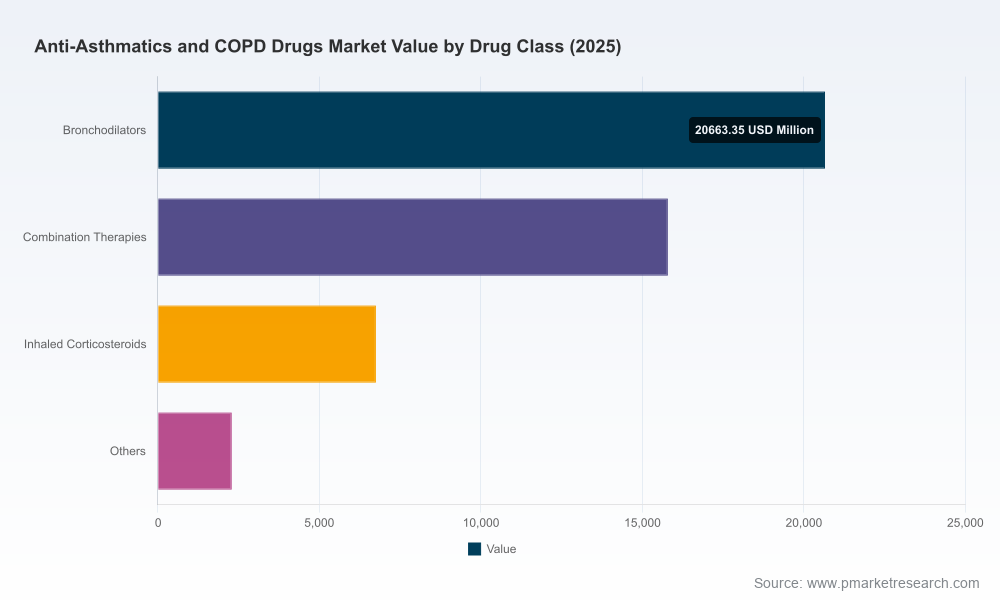

The global anti‑asthmatics and COPD drugs market has entered a phase of steady, product‑led expansion. Our latest market model shows the global market at roughly USD 45.5 billion in 2025, with a projected compound annual growth rate (CAGR) of 4.2% through 2032 — a trajectory that places the market near USD 60.7 billion by the end of the forecast window. For life‑science executives, payers, and investors preparing strategic plans for 2026, this report offers the actionable intelligence required to translate macro momentum into defensible commercial outcomes.

Anti Asthmatics And Copd Drugs Market

Why this report matters for 2026 corporate decisions

2026 is a pivotal year: product life cycles are converging with new therapeutic mechanisms, guideline updates, and sustainability mandates. Decisions taken this year — on portfolio prioritization, manufacturing investments, pricing strategy, and partner selection — will determine which organizations capture disproportionate share of the forecasted growth. Our Anti‑Asthmatics & COPD Drugs Market report is designed as a decision support system, not an academic exercise. It synthesizes epidemiology trends, regulatory inflection points, payer behavior, device and formulation evolution, and competitive positioning into a unified, execution‑ready brief.

Anti Asthmatics And Copd Drugs Market

Core strategic takeaways

- Stable, predictable growth supports selective investment: The mid‑single‑digit CAGR underpinning the market provides a predictable platform for targeted investments in novel mechanisms, biologics, and sustainable device technologies.

- Product differentiation is shifting from molecule to delivery and economics: Inhaler platforms, propellant sustainability, and real‑world evidence are increasingly decisive in formulary placement.

- Payer and guideline dynamics are accelerating segmentation: Recent approvals and guideline updates are creating payer sub‑segments that will reward targeted evidence generation and outcome‑based contracting.

- Mid‑sized innovators can create asymmetric value: Novel inhaled mechanisms and differentiated real‑world performance can create access pathways that circumvent entrenched incumbents.

What the report contains — practical, executable modules

- Market sizing and forward‑looking scenarios: three demand scenarios with sensitivity to guideline updates, reimbursement shocks, and new‑mechanism uptake.

- Clinical and pipeline mapping: a prioritized view of late‑stage molecules, device upgrades, and biologic entrants with commercial risk/reward profiles.

- Competitive playbooks: tactical analysis of incumbent and emergent players, including go‑to‑market strengths, device IP, and likely defensive moves.

- Payer & reimbursement intelligence: decision trees for formulary access, coding/reimbursement levers, and contracting templates oriented to the U.S., EU, and Asia markets.

- Commercial readiness checklists: launch sequencing, sample and hub strategy, field force construct, and digital support models calibrated to respiratory care.

- M&A and partnership screening: valuation heuristics, integration risk matrices, and a shortlist of capability gaps suitable for acquisition or alliance.

- Operational playbook: manufacturing scale‑up considerations, supplier risk mapping (notably for propellants and inhaler components), and sustainability transition timelines.

Competitive dynamics — what to watch in 2026

The market structure is moderately concentrated — the leading three firms command a substantial share and the top five are dominant — yet there remains fertile ground for focused entrants and specialty biotechs. Strategic positioning is becoming multi‑dimensional: molecule, device, sustainability, and economics.

Anti Asthmatics And Copd Drugs Market

- AstraZeneca (Cambridge, UK): Continues to leverage a broad inhaled portfolio and is emphasizing triple therapies, biologics, and next‑generation low‑GWP propellant initiatives. Recent real‑world and clinical presentations underscore its ambition to lead on both clinical outcomes and sustainability credentials.

- Boehringer Ingelheim (Ingelheim, Germany): Retains differentiated capability via its inhaler platforms and maintenance therapies, with an emphasis on device ergonomics and adherence‑oriented interventions.

- GSK plc (London, UK): Maintains a leadership posture with single‑inhaler triple therapies and device ecosystems; its recent pricing agreement with a large national payer illustrates an evolving approach to value sharing and government contracting.

- Novartis AG (Basel, Switzerland): Remains focused on long‑acting bronchodilators and device incremental innovation, competing on durable efficacy and generics defense.

- Verona Pharma plc (London/Raleigh): Demonstrates how a focused novel‑mechanism entrant can alter treatment paradigms: the recent commercial uptake and reimbursement coding support for its inhaled PDE3/4 inhibitor highlight a clear pathway for specialty innovators.

- Sanofi with Regeneron (Paris, France & collaborators): Biologics are now an integral part of respiratory care strategy — with the first biologic approvals for certain COPD phenotypes, the competitive frontier now includes immunomodulators and biomarker‑driven access models.

- Generics and volume players (Teva, Merck, Chiesi, etc.): Will continue to defend base volumes while seeking to capture tender opportunities and to broaden portfolios via device or formulation enhancements.

Regulatory and reimbursement inflection points shaping 2026

Several non‑market events will materially impact commercial outcomes:

- Guideline updates issued in 2025 and 2026 recalibrate diagnosis and management pathways for COPD, which affects eligible patient pools and therapy sequencing.

- Biologic approvals for defined COPD phenotypes have created new access pathways that require precise biomarker and HEOR strategies.

- Product‑specific reimbursement coding and J‑codes for novel inhaled therapies materially lower access friction when coupled with strong economic evidence.

- The industry‑wide transition to next‑generation low‑GWP propellants is accelerating CAPEX and compliance timelines for manufacturers and will become a procurement and tendering differentiator.

Strategic playbook — five actions to prioritize in 2026

- Re‑prioritize portfolios by commercial defensibility, not just clinical novelty: Assess therapies against device stickiness, total cost of care impact, and payer willingness to reimburse.

- Invest in targeted real‑world evidence (RWE): Rapid, pragmatic RWE demonstrating reduction in exacerbations, hospitalizations, or systemic steroid use will unlock access and contracting opportunities faster than expanded RCTs alone.

- Make sustainability a competitive asset: Proactively align product roadmaps to low‑GWP propellants and supply chain carbon reduction to meet procurement criteria used by large payers and health systems.

- Design flexible pricing and contracting templates: Prepare outcome‑based, indication‑based, and indication‑agnostic contracting approaches to be deployable by market and payer segment.

- Targeted M&A and alliances: Seek capabilities that fill device, digital adherence, or biomarker gaps. Valuation discipline should reflect integration risk and speed to commercial impact.

How PW Consulting helps — the 2026 support package

Our report is coupled with advisory modules designed for 90‑ to 180‑day activation cycles: launch readiness sprints, payer value dossiers and contracting templates, M&A screening workshops, and RWE study design support. Deliverables are tailored for commercial, medical, and corporate development teams who need executable plans, not theoretical frameworks.

Next steps and where to get the full intelligence

This release is a strategic preview: it surfaces the critical dynamics that will determine winners and losers in 2026, and it outlines the operational moves that convert market growth into sustained commercial leadership. For readers who require the granular datasets — including our full regional and indication splits, product‑level revenue modeling, and downloadable scenario files — the comprehensive report and supporting analytics platform are available through our research portal. The full package contains the detailed segmentation and financial tables necessary for budgeting, valuation, and tactical launch planning.

Contact PW Consulting to obtain the full Anti‑Asthmatics & COPD Drugs Market report and to schedule a strategy briefing tailored to your organization’s priorities for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Anti Asthmatics And Copd Drugs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com