PW Consulting: Strategic Brief — Aerospace Aircraft Stainless Steel Market Outlook (2026 Strategic Edition)

Executive Summary

As aerospace programs rebound and defense modernization programs accelerate, stainless steel remains a quietly critical enabler across airframes, engines, landing systems and cabin interiors. PW Consulting’s latest market study — the Aerospace Aircraft Stainless Steel Market report (base year 2025) — synthesizes macro trajectories, supply-chain dynamics, regulatory inflections and competitor positioning to inform high-stakes procurement, sourcing and product-development decisions for 2026 and beyond.

Aerospace Aircraft Stainless Steel Market

Key macro takeaways are straightforward and actionable: the sector is sizable — with a global market value of approximately USD 2,734.08 Million in 2025 — and is projected to expand at a compound annual growth rate (CAGR) of roughly 5.45% through our 2026–2032 forecast horizon. By the terminal year of our outlook (2032) the market is expected to approach just under USD 4.0 Billion, reflecting both structural aviation demand and material-driven price dynamics.

Aerospace Aircraft Stainless Steel Market

Why this matters for 2026 decision-makers

- Timing matters: 2026 is a pivot year — regulatory headwinds and raw-material swings are layering structural change onto cyclical aerospace demand. Commercial and defense buyers must translate directional market growth into procurement cadence and inventory policy.

- Margin management: Nickel and alloy volatility materially affect input-cost volatility; a resilient purchasing strategy that combines hedging, long-term offtake agreements and alloy substitution pilots can protect margins.

- Supply resilience: Elevated tariffs and emerging carbon-cost mechanisms are reshaping sourcing geographies and total landed cost calculations. Firms that re-map supplier portfolios now will avoid disruptive rework later in program lifecycles.

Market trajectory & structural signals

Our analysis integrates historical behavior (2020–2025) and forward scenarios (2026–2032). The 5.45% CAGR masks meaningful intra-period inflection points: near-term price-driven volatility, mid-horizon supply reconfiguration, and longer-term demand uplift tied to fleet renewals and advanced air mobility demonstrators. These dynamics create both risk and opportunity — incumbent suppliers with engineering-grade portfolios and agile distributors can capture outsized share, while OEM procurement teams face the challenge of balancing performance specifications against life-cycle cost.

Aerospace Aircraft Stainless Steel Market

Concentration metrics indicate a market that is neither fragmented nor monopolized: the top three players do not dominate the space entirely, and a modestly broader group of leading suppliers accounts for a meaningful share of industry shipments. This structure enables differentiated competition around service, qualification support and specialty grades rather than pure price alone.

Supply chain, raw materials & regulatory pressure

- Raw material exposure: Nickel remains a key cost driver — analysts estimate it can account for as much as 70% of the variable cost in certain austenitic stainless production routes. Spot and contract nickel pricing spikes translate quickly into margin pressure for mills and downstream fabricators.

- Price environment: Observed unit-price upticks for stainless in North America in early 2026 illustrate how alloy input moves propagate through the value chain. Procurement teams should assume higher base-case landed-costs and stress-test supplier bids under multiple raw-material scenarios.

- Regulatory shifts: Two policy changes deserve immediate attention. The European Union’s Carbon Border Adjustment Mechanism reached its payment phase at the start of 2026, introducing a new form of carbon-based import cost that will affect sourcing from high-carbon-intensity regions. Simultaneously, the persistence of U.S. Section 232 steel and aluminum tariffs continues to alter comparative cost structures for transatlantic and transpacific shipments.

- Geopolitical & industrial policy: National industrial strategies — notably China’s renewed emphasis on high-tech and aerospace sectors in 2026 — will shape capacity deployment for special alloys and premium stainless grades, with downstream implications for qualification timelines and dual-sourcing strategies.

Competitive landscape — what matters beyond logos

The market features a mix of global stainless mills, specialty alloy producers, and dedicated aerospace distributors. We profile a cohort of industry-relevant players — including long-established global mills, specialized domestic producers, and asset-light distributors — to illustrate strategic positioning rather than to offer a simple leaderboard.

- Global mills and material innovators: Firms with integrated melt-to-finish capability and aerospace-certified grades hold a sustainable advantage for high-temperature and corrosion-resistant requirements. Their R&D investments into alloy optimization and fabrication-ready formats shorten qualification cycles for OEMs.

- Specialty producers and converters: Companies focused on aerospace-grade stainless and nickel alloys offer value through customized chemistries, traceability, and certification services — critical in engine and structural workstreams.

- Distributors and service centers: Large aerospace-focused distributors are executing capacity expansions and service-line improvements to reduce lead-times and additive-value services (e.g., kitting, VMI, certification packs). These capabilities are decisive for Tier-1 suppliers and MRO operators who prioritize responsiveness and inventory flexibility.

Highlighted corporate developments in late 2025 underscore this dynamic: select distributors expanded physical footprint to handle aerospace volumes; multiple suppliers used trade exhibitions to showcase manufacturing and alloy capabilities; and new advanced manufacturing centers are being developed to scale componentized production. These moves are tactical responses to lead-time pressures and the need for closer collaboration with OEM supply chains.

Report contents — actionable intelligence (what’s inside)

PW Consulting’s report is structured to serve executives, procurement leads, product managers and strategy teams. The deliverables are operational and decision-focused rather than purely descriptive:

- Top-line market sizing and validated CAGR (base year 2025, forecast through 2032) with scenario variants reflecting raw-material stress, policy shocks and program re-phasing.

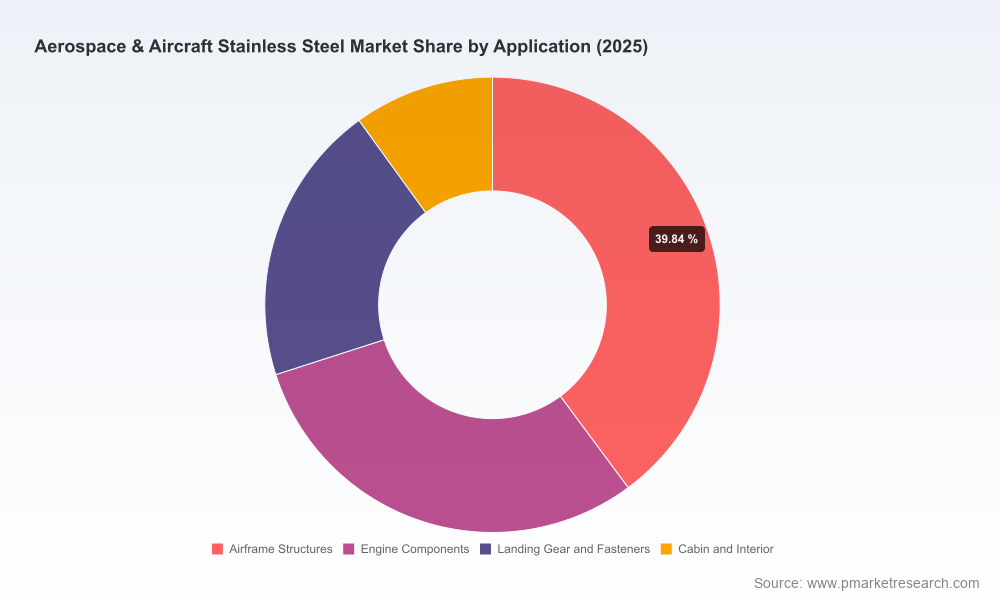

- Segment-level analysis by geography, stainless type and application — including qualification complexity and supplier readiness assessments. (Note: this press brief intentionally omits segment-level figures; access to the full dataset is available on the report page.)

- Supply-chain heat maps and risk matrices that identify single-sourced nodes, critical alloy exposures and near-term inventory pinch points.

- Action-ready supplier scorecards covering technical capability, certification depth, price stability, and on-time delivery performance.

- Procurement playbooks: hedging strategies, contract constructs, and alloy-substitution decision trees that are immediately implementable in 2026 sourcing cycles.

- Scenario-based financial models that translate alloy-price moves and tariff/carbon costs into landed-cost sensitivity for program managers.

How companies should use the research in 2026

We recommend three parallel tracks that synthesize our findings into executable plans for 2026:

- Risk reduction and supplier diversification: Use the report’s supplier scorecards and heat maps to qualify alternate sources for critical alloys and to establish dual-sourcing for program-critical components before lead-time stress intensifies.

- Cost-to-serve redesign: Recalculate total landed cost models that include CBAM-related payments and tariff overlays; shift negotiation focus from nominal mill prices to integrated total-cost arrangements tied to carbon intensity and delivery reliability.

- Innovation and product readiness: Invest selectively in alloy qualification pilots (e.g., lower-nickel austenitic blends or duplex steels where feasible) using the report’s technical assessment and qualification timelines to shorten ramp-up risk.

Competitive positioning & M&A considerations

Market concentration metrics suggest room for consolidation around differentiated capabilities: strategic buyers should prioritize targets that add either aerospace-certified mill capacity, vertically integrated finishing capability, or distributor networks that reduce time-to-program. Conversely, incumbent producers should evaluate bolt-on acquisitions that improve traceability, certification throughput or proximity to key OEM hubs.

What we intentionally withhold here (and why)

In keeping with the “trailer” principle of this announcement, we present the strategic narrative, macro numbers and the operational frameworks you need to act — while reserving the granular segmentation breakdowns, supplier-level pricing matrices, and downloadable financial models for the full report. That level of detail is purposefully gated to ensure data integrity, traceability of sources and the practical confidentiality our clients require when executing sourcing or M&A strategies.

Next steps & how to engage PW Consulting

- Download the full report for complete segment-level datasets, supplier scorecards and financial models (available on our website).

- Commission a rapid 6–8 week advisory sprint if you require tailored supplier due diligence, scenario modeling for a marquee program, or procurement playbook implementation.

- Subscribe to our quarterly bulletin for rolling updates on raw-material pricing, policy changes and new capacity announcements that affect aerospace stainless flows.

Closing perspective

For aerospace stakeholders preparing plans in 2026, the stainless-steel market represents both a familiar material domain and a fast-evolving strategic frontier. The interplay of rising alloy costs, carbon-related import economics, and targeted industrial policies is reshaping where and how aerospace metals are sourced and qualified. PW Consulting’s Aerospace Aircraft Stainless Steel Market report equips leaders with the foresight and practical tools to convert these shifts into defensible procurement strategies, resilient supply architectures, and targeted product-investment decisions.

To access the full intelligence package — including the granular segmentation, supplier scorecards, and executable cost models — visit the PW Consulting report page and request the Aerospace Aircraft Stainless Steel Market full report.

For detailed analysis of this topic, please visit the official page:Aerospace Aircraft Stainless Steel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com