Lock Market 2026: Strategic Imperatives from PW Consulting’s New Market Research Brief

PW Consulting’s Lock Market report for 2026 is a tailored strategic briefing for senior executives, corporate strategy teams, private equity sponsors, and procurement leaders who must make high-stakes decisions in an industry at the intersection of physical hardware and digital access. Anchored on a 2020–2025 historical baseline and forward-looking to 2026–2032, our analysis quantifies the market’s recent recovery and frames tactical choices against supply-chain shocks, rising materials costs, and accelerating smart-lock adoption.

Lock Market

Headline figures you need to know

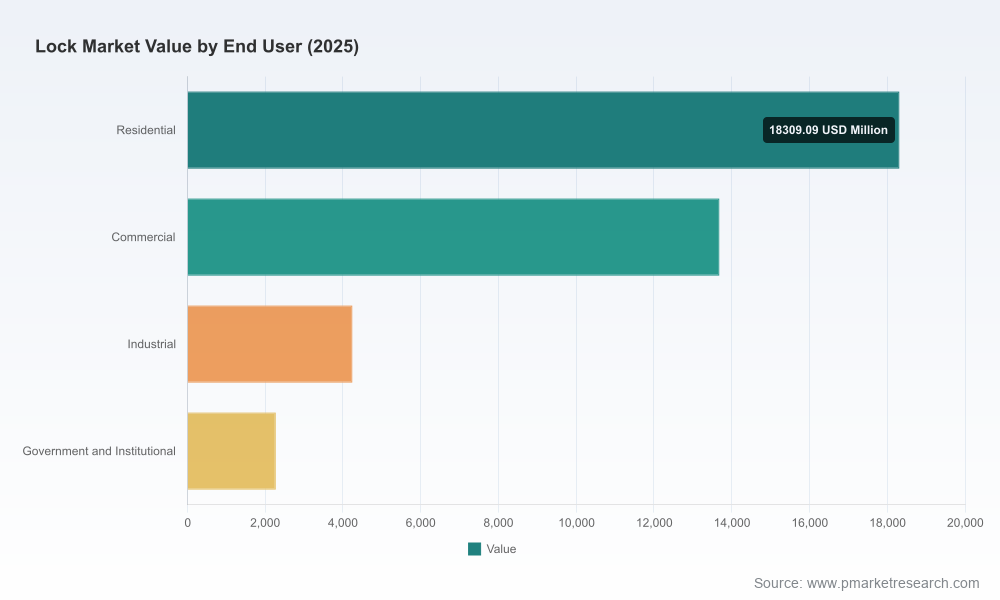

- The global lock market reached approximately USD 38,500 Million in our base year 2025, up materially from the 2020 baseline.

- Our forecast period (2026–2032) is modeled around a compound annual growth rate (CAGR) of 6.15%, reflecting both resilient demand in traditional mechanical segments and faster growth pockets in electronic and electromechanical access solutions.

- By the end of the forecast horizon the market is projected to surpass the mid‑ten‑thousands (USD Million), driven by technology migration, building retrofit cycles, and institutional security upgrades.

Why this matters for 2026 decisions

2026 is a decisive year for market players and buyers. Macro and industry-specific forces — from trade policy shifts to component price volatility — are compressing planning horizons and amplifying execution risk. Our report translates these uncertainties into actionable levers:

Lock Market

- Cost-to-serve and procurement: With elevated tariffs on steel and aluminum introduced in 2025 and ongoing raw-material volatility, margin management requires new sourcing playbooks. We provide scenario-tested cost pass-through models and supplier risk scorecards to help procurement teams quantify tradeoffs between reshoring, nearshoring, and diversified supplier pools.

- Product portfolio and R&D prioritization: The convergence of mechanical endurance and digital authentication creates product hybridization opportunities. The report’s product heatmaps and technology-roadmap overlays help R&D and portfolio managers prioritize development spend between incremental mechanical innovation and higher-margin smart-lock features.

- Channel and go-to-market: As consumer and commercial channels fragment, optimized channel mixes will determine price realization. We lay out tactical GTM experiments — from channel rebates to integrated managed-access subscriptions — with modeled ROI for 12–36 month horizons.

- M&A and partnerships: Fragmentation persists, creating opportunities for bolt-on acquisitions and strategic alliances. Our M&A playbook identifies target archetypes, accretion simulations, and integration risk checklists tuned to 2026 market realities.

What the report contains (practical, operational content)

We designed the report as more than a market summary; it is a hands-on implementation toolkit. Highlights include:

Lock Market

- Methodology appendix: transparent bottom‑up revenue triangulation, primary interviews with OEMs and distributors, and supply‑chain footprint mapping to validate projections.

- Scenario planning: three rigorously stress‑tested industry scenarios — baseline, protectionist, and accelerated-digital — each with quantified P&L and cash-flow implications for representative company archetypes.

- Commercial playbooks: channel segmentation strategies, pricing elasticity models, and commercial contract clauses to protect margins under tariff regimes.

- Operational tools: supplier concentration matrices, inventory hedging strategies for key components, and a step-by-step guide to evaluate reshoring versus nearshoring investments.

- Technology and cyber-physical risk framework: threat models for connected locks, supplier security diligence checklists, and recommended cybersecurity SLAs for product and service contracts.

- Investment and ROI models: capital allocation templates for production upgrades, smart-lock software stacks, and aftermarket service programs, with sensitivity to material-cost shocks and demand shifts.

Competitive dynamics and what they mean for market participants

The competitive landscape combines legacy incumbents with digital-native challengers. The market remains relatively fragmented: top-tier players supply a meaningful share, but a broad base of regional manufacturers and niche specialists sustains competitive intensity. This structure creates distinct strategic paths:

- Scale players: Global incumbents leverage distribution breadth and integrated product suites. Their advantages include end-to-end access portfolios spanning mechanical, electromechanical, and smart systems, plus scale in supply-chain management and global aftermarket channels.

- Specialists and regional champions: Companies focused on high-security cylinders, niche industrial applications, or cost‑sensitive mass-market products continue to carve defensible positions through product differentiation or local manufacturing agility.

- Integration and consolidation catalysts: Recent acquisitive moves reflect a trend toward capability aggregation — combining high‑security mechanical expertise with electronic and software capabilities to capture higher-margin service streams.

Notable company developments underscore these structural dynamics. For example, the integration of a high-security safe-lock specialist into a global access platform has accelerated the incumbent’s capability set in government and critical-infrastructure segments. Such moves change competitive calculus for firms evaluating organic build versus buy strategies in 2026.

Regulatory, materials, and supply‑chain headwinds

Our analysis incorporates a wave of policy and materials shocks that materially affect cost structures and sourcing strategy:

- Trade policy shocks: Recent tariff escalations on key metals have increased procurement costs for manufacturers that rely on steel and aluminum in lock hardware. These measures are not transient in our base scenarios and require strategic hedging in long‑term supplier contracts.

- Materials volatility: Steel price swings and constrained mill capacity have created asymmetric cost exposure across product types. The report provides sensitivity models that translate metal-price movements into margin impact across product archetypes.

- Cross-border supply disruptions: Tariff measures affecting neighboring trade partners have incentivized supply-chain redesigns; the report supplies a decision framework for when to reconfigure production footprints versus absorb short-term cost increases.

Practical recommendations for 2026

Based on our scenario work and company benchmarking, we recommend the following immediate actions for leadership teams:

- Stress-test your supplier book: Implement quarterly supplier risk reviews using the report’s supplier concentration indices and make contingency contracts (dual-sourcing or committed capacity) part of your standard procurement playbook.

- Prioritize hybrid product investments: Allocate R&D budget toward electromechanical and secure-cloud integration features that open recurring-revenue pathways while preserving low-cost mechanical product lines through manufacturing efficiency programs.

- Revisit channel economics: Experiment with subscription pricing and managed-services bundles in select markets to test customer willingness to pay for convenience and security assurance.

- Prepare M&A scorecards today: Use the provided target archetype templates to pre-screen acquisition targets that offer capability fills (e.g., high-security patents, cloud-native access platforms) and run integration pilots within 6–12 months.

- Raise cyber-physical standards: Institute minimum cybersecurity and firmware-update SLAs with suppliers and partners, and adopt incident-response playbooks aligned to customers in critical infrastructure sectors.

Why download the full report

This press briefing is intentionally selective. To protect commercial confidentiality and preserve the strategic value of detailed segmentation, we have omitted granular regional, application and line-item revenue splits from this summary. The full Lock Market report provides:

- Complete regional and end‑use segmentation with market sizing and growth trajectories at a level appropriate for market-entry and capex planning;

- Vendor-level benchmarking with product-by-product margin and distribution analyses;

- Deal models and integration playbooks for bolt-on acquisitions, including target valuation ranges and sensitivity to tariff and raw-material shocks;

- An extensive appendix of primary research interviews, supplier maps, and raw data tables to support client diligence and investor memoranda.

For decision-makers preparing budgets, revising three- to five-year product roadmaps, or evaluating strategic M&A, the full report converts our models into executable actions and quantifiable tradeoffs.

Next steps for executives

- Download the full Lock Market report to access comprehensive regional and application breakouts and the data tables that underwrite our forecasts.

- Engage PW Consulting for a tailored deep-dive workshop: we will run scenario planning with your P&L and simulate acquisition/investment outcomes using client-specific inputs.

- Subscribe to our quarterly Lock Market tracker for rolling updates on tariffs, material costs, and vendor consolidation moves that will affect tactical decisions throughout 2026.

PW Consulting’s Lock Market report translates a complex, evolving market into pragmatic actions. As the industry bridges hardware durability and digital services, the firms that align procurement resilience, product strategy, and go‑to‑market innovation will capture disproportionate value. Our full report provides the data, models, and playbooks you need to lead that transition in 2026.

For detailed analysis of this topic, please visit the official page:Lock Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com