Healthcare IT Market: Size, Share, and Future Growth

Other |

2026-05-25 10:22:00

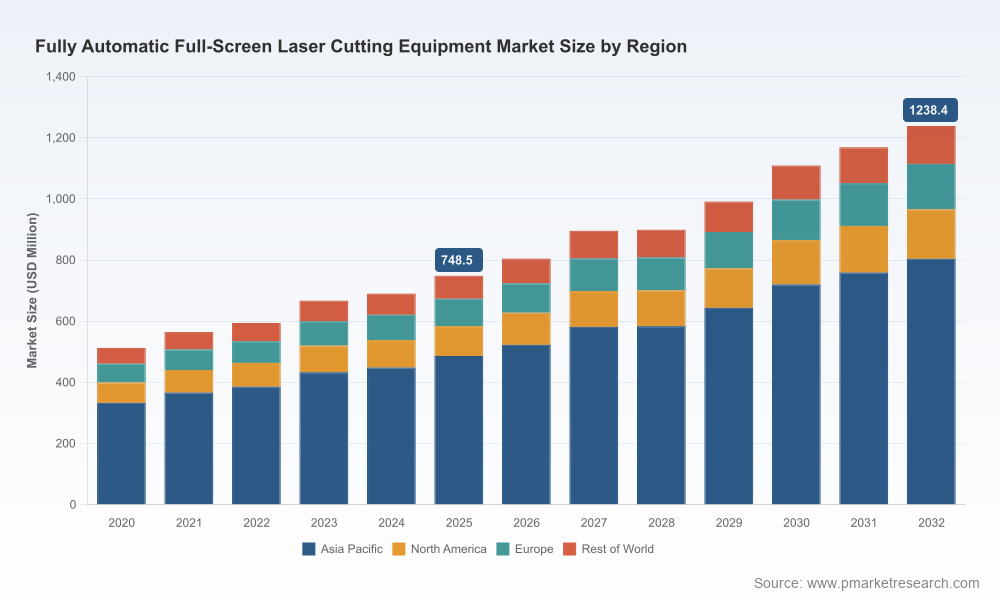

PW Consulting today publishes a focused industry briefing drawn from our forthcoming market research report on the Fully Automatic Full Screen Laser Cutting Equipment market. Anchored on a base year of 2025 and built from a five‑year historical series (2020–2025), the study projects the market to expand at a compound annual growth rate (CAGR) of 7.46% through the 2026–2032 forecast window. For executives planning capital allocation and technology roadmaps in 2026, the report synthesizes market sizing, competitive mapping, technology tradeoffs and pragmatic playbooks that convert insights into defensible actions.

Fully Automatic Full Screen Laser Cutting Equipment Market

2026 represents an inflection in purchasing, regulation and product design cycles across electronics, automotive displays and wearables. Three structural drivers are converging: continued industrial automation adoption, regulatory focus on energy efficiency that favors fiber and solid‑state lasers, and recurring raw material cost volatility that affects CAPEX timing and total cost of ownership calculations. These forces mean that procurement in 2026 will determine not just near‑term throughput but the next decade of unit economics and product differentiation.

Fully Automatic Full Screen Laser Cutting Equipment Market

Timing matters: investments rushed into legacy architectures risk early obsolescence as energy‑efficient laser technologies become standard and as integrated automation architectures proliferate.

Fully Automatic Full Screen Laser Cutting Equipment Market

Operational impact: the optimal procurement decision balances throughput, precision and lifecycle energy consumption — metrics that must be modeled against production mix and product roadmaps.

Strategic flexibility: firms that adopt staged deployment—pilot, validation, scale—secure higher ROI and minimize disruption to existing production lines.

Clients will find the study deliberately operational. Highlights include:

Market sizing and forecast model spanning 2020–2032, with scenario variants that stress test demand under different technology adoption and macroeconomic trajectories.

Technology valuation matrices comparing ultrafast, UV and fiber/solid‑state laser platforms across throughput, precision, thermal impact, energy intensity and maintenance profiles.

Supplier benchmarking: qualitative and quantitative scorecards designed to inform RFP shortlists, including capability maps, service footprint, automation integration and typical TCO profiles.

Operational playbooks for procurement, pilot programs, and commissioning, with checklists and contract clauses to protect buyers against common pitfalls (warranty scope, uplifts, software/IP terms).

Commercial frameworks for OEMs, EMS providers and contract manufacturers including go‑to‑market levers and partner models (licensing, co‑development, distribution).

Excel‑based tools that allow clients to plug in their production parameters to see localized TCO, payback and utilization scenarios.

Note: The report deliberately omits detailed sub‑segment line items in this briefing to preserve commercial value; full regional, application and vendor share tables are provided to subscribing clients via the source portal.

The market exhibits a moderate level of concentration. The top three vendors account for an appreciable portion of global revenues, while the top five command a clear majority share — a structure that creates both stability and opportunity for challengers. Key players analyzed in the report include a mix of specialized laser OEMs and broader automation system suppliers:

Farley Laserlab (HG Farley LaserLab Co / HGTECH subsidiary) — leveraging high‑power fiber platforms and advanced automation to address large‑format, high‑precision industrial cutting. Their geographic footprint and product scope position them as a competitive anchor for heavy industrial users.

GD Han’s Yueming Laser — a broad portfolio across precision applications that balances cost competitiveness with local service advantages in large manufacturing economies.

Kunshan Dapeng Precision Machinery & Beijing Torch SMT — regional players focused on integrating full‑screen automation into mass‑manufacturing workflows, often competing on customization and rapid delivery.

Global system integrators and precision OEMs (e.g., Mitsubishi Electric, Control Micro Systems, EBSO GmbH, Aurotek Corporation, ASYS Group) — these firms often win on proven reliability, deep automation integration and service networks that matter in high‑mix, high‑value manufacturing.

Strategic takeaways for buyers and investors:

Supplier selection must weigh three axes: core laser source capability, automation/software integration, and service/parts ecosystem. Vendors strong in only one axis are tactical suppliers; firms performing across all three are strategic partners.

M&A and partnership activity is likely among mid‑tier vendors seeking to broaden automation portfolios or geographic reach — a theme the report explores with candidate profiles and valuation sensitivities.

New entrants focused on ultrafast and UV niches can capture differentiated applications, but scaling to broader industrial volumes requires investment in automation and after‑sales service infrastructure.

From an engineering and business perspective, selecting a laser system is never purely technical — it is a portfolio decision. Ultrafast lasers bring advantages where thermal damage must be minimized; UV platforms enable fine feature work; fiber and other solid‑state lasers deliver operational efficiency and power‑density for throughput‑centric tasks. Energy efficiency mandates and lifecycle energy costs are shifting the economics decisively towards fiber and solid‑state options in many applications.

For 2026 procurement plans, we recommend a three‑step evaluation:

Map products to critical quality and throughput requirements; run a technology fit gap analysis rather than defaulting to the lowest capital cost.

Quantify lifecycle energy and maintenance costs over a realistic equipment horizon (7–10 years); small differences in energy efficiency compound materially at scale.

Ensure automation and software compatibility with existing MES/ERP; retrofit costs for controls or vision systems can erode projected ROI.

Raw material price swings (notably in steel and aluminum inputs to machine frames and fixturing) continue to introduce capital cost uncertainty. Coupled with periodic semiconductor and optics supply constraints, procurement teams should adopt layered tactics: forward purchase agreements for critical subsystems, modular upgrade pathways, and contingency suppliers for spares and optics. The report provides a practical vendor due diligence checklist and contract clause templates to manage these risks.

For leaders who must move from analysis to execution in 2026, PW Consulting offers a compact, prioritized playbook:

Prioritize pilots: Validate 1–2 systems on the most complex SKU families before committing to line‑wide replacement.

Insist on TCO‑based RFPs: Require vendors to provide modeled energy, spare parts, and downtime assumptions over the contract term.

Negotiate strong service SLAs and parts cascades: For mission‑critical production, pay more for guaranteed uptime rather than lower capital price.

Plan for modular upgrades: Favor systems that allow laser‑source swaps or control upgrades to protect against obsolescence.

Embed digital readiness in contracts: Ensure APIs, data access and cybersecurity terms are clear to support predictive maintenance and yield analytics.

Monitor consolidation signals: Use supplier scorecards from the report to inform M&A targets or strategic alliances that close capability gaps quickly.

Beyond headline forecasts and vendor lists, the report was built to be a transactionally useful tool: downloadable model workbooks, supplier scorecards, risk checklists and negotiation playbooks. It translates market growth assumptions — quantified across an established historical run and a multi‑year forecast — into procurement, technology and corporate development actions that can be implemented in the coming budget cycle.

We deliberately keep the detailed regional and application split tables, individual vendor share numbers and certain price curves gated; these are core deliverables available to subscribers and consulting clients. That structure allows us to provide the robust, proprietary analyses that materially change supplier selection and CAPEX outcomes.

If you are responsible for capital planning, manufacturing strategy or M&A in 2026, use this briefing to test internal assumptions and prioritize areas for immediate diagnostic work: run a TCO comparison on your current install base versus best‑in‑class systems; identify one pilot SKU for ultrafast or UV evaluation; and commission a vendor diligence pack focused on service capability and automation integration.

PW Consulting stands ready to help clients translate the report’s models into bespoke decision‑support tools — from tailored TCO scenarios to confidential supplier due diligence. Our market study provides the strategic perspective; our advisory engagements convert that perspective into executable plans that protect margins, accelerate product development cycles, and reduce operational risk.

For detailed analysis of this topic, please visit the official page:Fully Automatic Full Screen Laser Cutting Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com