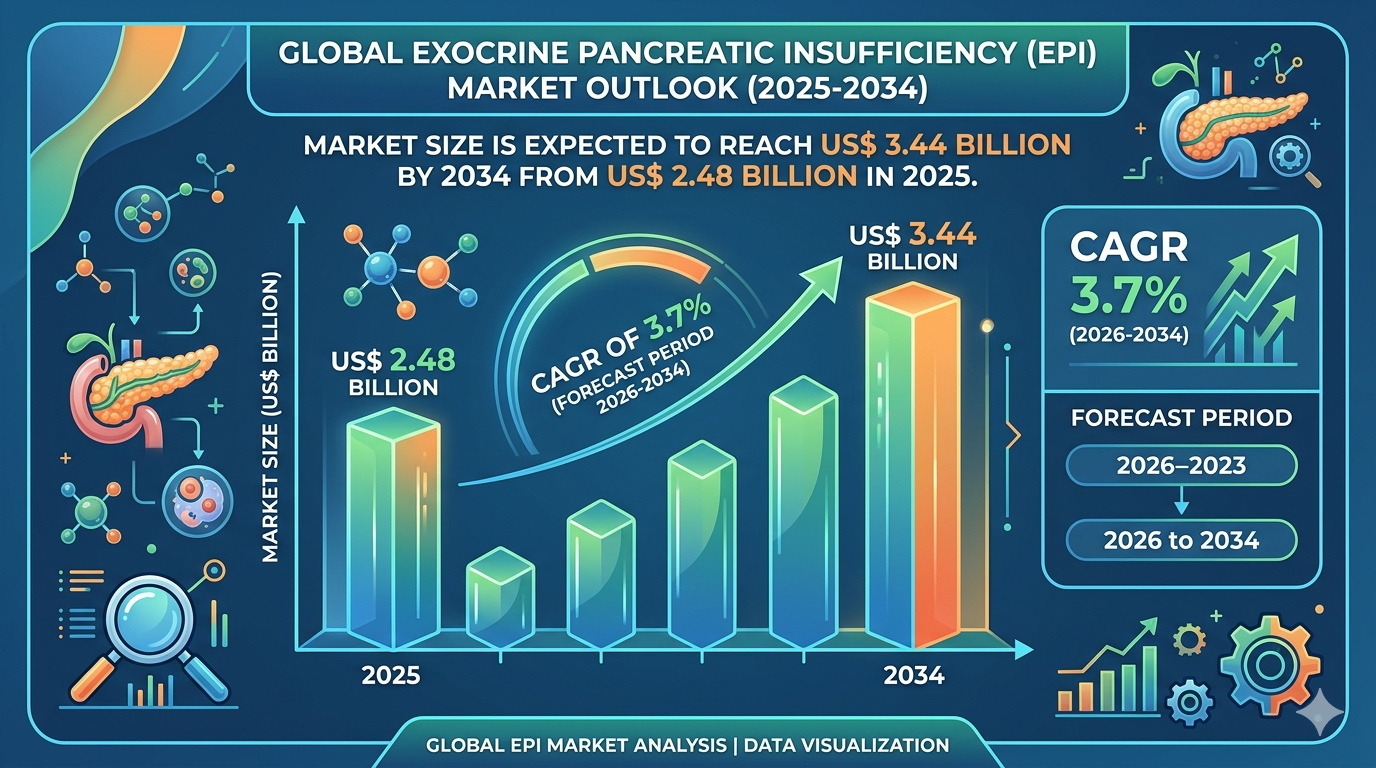

How Innovation is Driving the US Exocrine Pancreatic Insufficiency Market Growth at 3.7% CAGR

Other |

2026-04-24 10:04:30

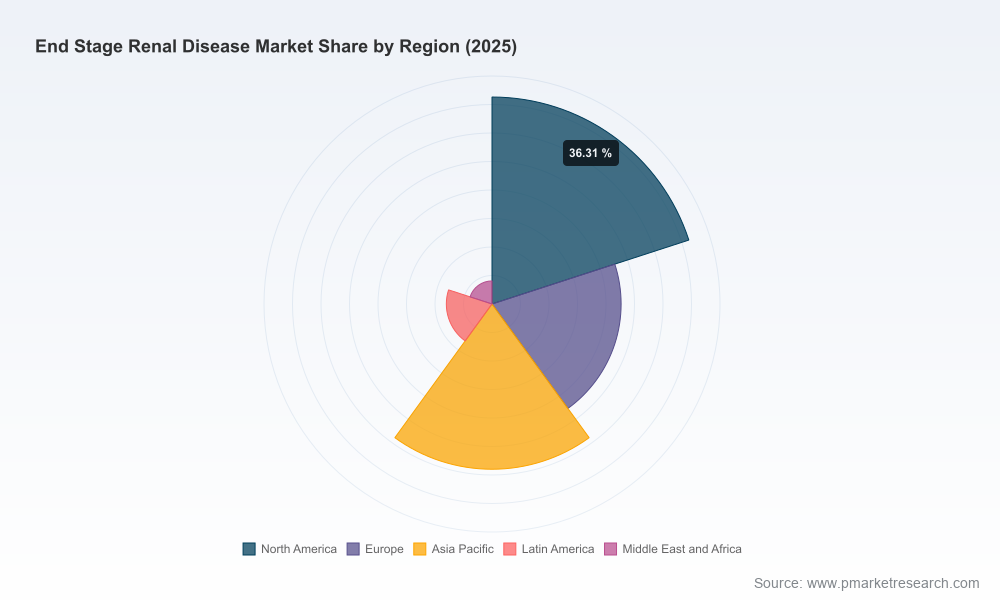

The global End Stage Renal Disease (ESRD) market is at an inflection point. Our PW Consulting End Stage Renal Disease Market Report (base year 2025) synthesizes five years of historical performance and a seven‑year forecast to deliver a pragmatic roadmap for executive teams preparing 2026 strategies. The market expanded from approximately USD 92,450 Million in 2020 to roughly USD 152,306 Million in 2025 and is projected to grow at a compounded annual growth rate (CAGR) of 10.45% over the 2026–2032 forecast window, reaching an estimated USD 305,407 Million by 2032. These headline trajectories underpin a landscape shaped by reimbursement adjustments, accelerated home‑care adoption, device innovation, and continued consolidation among leading providers (CR3: 52.4%, CR5: 64.1%).

End Stage Renal Disease Market

Timing matters: 2026 will be the first full planning cycle after several material policy and product inflection points—most notably implementation of updated ESRD prospective payment system (PPS) rules and the commercial launches of next‑generation dialysis platforms. Our analysis translates these disruptions into clear opportunity and risk vectors for the coming year.

End Stage Renal Disease Market

Decision focus: The report is built to answer the three questions CEOs and product leaders will face in 2026—where to invest, how to defend core revenue streams, and which capabilities to acquire or partner for rapid scale.

End Stage Renal Disease Market

Actionable intelligence: Rather than high‑level commentary, the report provides executable playbooks (M&A screening, commercialization blueprints, reimbursement optimization levers) and scenario tools to stress‑test allocation choices against realistic regulatory and market outcomes.

Market sizing and forward projections: A transparent modeling approach that reconciles historical trends (2020–2025) with a scenario‑based forecast (2026–2032) and quantifies upside and downside paths under alternative adoption and reimbursement scenarios.

Segmentation frameworks and adoption curves: Multi‑dimensional splits across care settings, treatment modalities and component categories—presented with growth multipliers and strategic levers—while detailed tables and regional roll‑ups are reserved for the full report to protect actionable competitive detail.

Provider economics and reimbursement analysis: A dedicated module on payer dynamics, including analysis of the CY 2026 ESRD PPS final rule (base rate set at $281.71 and related wage‑index mechanics), the incorporation of oral dialysis drugs into bundled payments, and implications for facility margins and capital deployment.

Technology and clinical innovation assessment: Diagnostics of incumbent and emerging platforms—hemodialysis systems, peritoneal solutions, vascular access, and digital care orchestration—assessing clinical impact, go‑to‑market readiness, and commercialization risk.

Competitive landscape and deal flow: Profiles of leading incumbents and challenger entrants, an assessment of competitive concentration (CR3/CR5), and an M&A heatmap indicating strategic fit, integration complexity and likely valuation bands.

Playbooks and KPIs: Board‑ready investment thesis templates, three prioritized growth playbooks for 2026, and a set of operational KPIs to monitor execution (patient conversion, asset utilization, ASP trajectories, service attach rates).

The ESRD ecosystem remains concentrated but dynamic. Established dialysis platforms and service providers continue to command scale advantages across distribution and care delivery channels. Leading device and care companies have differentiated portfolios spanning machines, consumables, and service networks; several are executing cross‑border commercialization and value‑based care pilots to protect reimbursement exposure.

At the same time, agile medtech entrants are changing the competitive equation. Systems designed for simplified setup, secure connectivity, and home use are shortening the commercialization cycle and lowering the marginal cost of care delivery. Examples of these dynamics include the upcoming full commercial rollouts of high‑volume hemodiafiltration systems by major OEMs and regulatory clearances for next‑generation modular dialysis platforms that emphasize cybersecurity and enterprise interoperability. Expect intensified competition at the interface of device providers, clinic operators and payers—particularly where integrated care models promise lower total cost of care.

ESRD PPS updates: The CY 2026 final rule—most notably the updated base rate and maintained labor‑related share—creates both immediate and structural impacts on facility economics. Incremental increases in base payment and stability in wage index policy support moderate near‑term revenue resilience but keep pressure on efficiency and service‑mix decisions.

Bundling and drug inclusion: The continuation of oral‑only dialysis drugs within the ESRD PPS bundle means manufacturers must adapt pricing and evidence strategies to demonstrate value beyond unit price—payers are emphasizing outcomes and cost offsets.

Payment parity for acute kidney injury (AKI): Payment alignment for AKI dialysis with ESRD base rates simplifies marginal reimbursement for acute therapy in hospital settings, altering hospital investment calculus for in‑house renal replacement services.

Prioritize platform interoperability and cybersecurity: As regulators and purchasers demand secure, connected systems, vendors should accelerate software maturity and enterprise security certifications to unlock enterprise contracts and post‑acute adoption pathways.

Optimize mix and site strategy: With payer pressure persistent, operators should model the financial impact of shifting treatment mix (home vs. in‑center, dialysis modalities) and rationalize footprint investments using the report’s scenario templates.

Rethink partnerships not just acquisitions: For many firms, strategic alliances—technology licensing, co‑development with digital health players, managed services—offer faster, lower‑risk routes to capture growth in home dialysis and value‑based care programs.

Invest in evidence generation: Manufacturers and providers must align clinical programs to demonstrate outcomes that matter to payers (hospitalization reduction, patient‑reported outcomes) to justify premium pricing and secure favorable contractual terms.

Prepare for consolidation: Given a market concentration where top groups control a meaningful share, expect continued M&A activity—target selection should weigh integration synergies, access to distribution channels, and regulatory hurdles more heavily than pure revenue multiples.

Several high‑profile moves illustrate the trends we identify. Long‑standing dialysis network and device leaders are combining product introductions with service innovations to protect their installed base and win managed‑care contracts. Newer platform entrants are obtaining regulatory clearances that emphasize enterprise security and home readiness, accelerating adoption among hospital systems and large outpatient networks. Payers and regulators are simultaneously adjusting payment rules and quality levers, which in aggregate increase the value of technologies that demonstrably reduce downstream utilization.

Board readiness: Use the executive scenarios to stress‑test capital allocation and M&A proposals before board review.

Commercial planning: Adopt the commercialization blueprints to shorten time to adoption in targeted segments, and deploy the stakeholder mapping tools to align clinical, procurement and payer outreach.

Regulatory strategy: Leverage our regulatory matrix to prioritize filings and evidence generation plans that maximize reimbursement uptake and minimize time to market.

This report blends rigorous, model‑driven forecasting (2020–2025 history; 2026–2032 forecast at a 10.45% CAGR) with practical playbooks and competitor insights tailored to 2026 decision cycles. We surface the levers that matter—reimbursement dynamics, product differentiation, partnership architectures, and operational execution—while deliberately reserving proprietary segment‑level tables and regional breakouts to the full report to preserve competitive value for subscribers.

For executive teams preparing budgets, M&A pipelines, or product launches in 2026, the report delivers both the strategic horizon and the tactical checklists required to convert market growth into sustainable advantage. To access the full dataset, downloadable models, and the complete competitive annex, visit the report landing page and request the PW Consulting End Stage Renal Disease Market Report.

For detailed analysis of this topic, please visit the official page:End Stage Renal Disease Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com