Cone Beam Imaging (CBCT) Market — Strategic Outlook for 2026: Actionable Intelligence for Decision-Makers

Executive summary

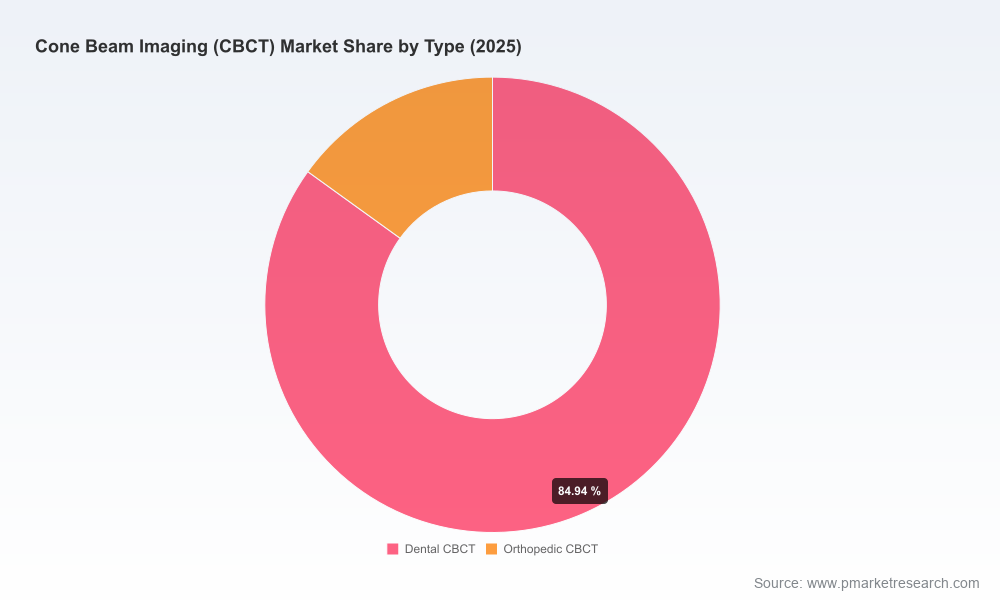

The global Cone Beam Imaging (CBCT) market has moved from a specialized diagnostic adjunct to a core imaging modality across dental, orthodontic and selected orthopedic pathways. Our base-year analysis (2025) places the total market at USD 1,850.0 Million (USD, Million unit), reflecting rapid adoption since 2020 when the market measured approximately USD 1,244.6 Million. PW Consulting’s forecast projects a sustained expansion through 2032, culminating at approximately USD 3,222.4 Million and representing a compound annual growth rate (CAGR) of 8.25% for the 2026–2032 period.

Cone Beam Imaging Cbct Market

For corporate leaders setting strategy in 2026, the implications are clear: CBCT is no longer a niche investment — it is a growth engine that blends hardware upgrades, AI-enabled software, and new clinical workflows. However, value will accrue to firms that can navigate reimbursement ambiguity, deliver regulatory-grade AI solutions, and align with capital-constrained buyers such as dental group chains and hospital imaging departments.

Cone Beam Imaging Cbct Market

Why this report matters for 2026 decisions

- Proven market momentum: The market’s recovery and acceleration post-2020 demonstrates durable demand. Our modeling reconciles historical volumes (2020–2025) with detailed scenario projections to 2032, enabling confident resource allocation for product launches, capacity expansion, and M&A.

- Regulatory inflection: Multiple AI-enabled CBCT tools received FDA 510(k) clearances in 2025–2026, creating a regulatory pathway for image-analysis software and shifting competitive dynamics toward software-hardware bundles.

- Capital expenditure pressure: Hospitals and large dental groups remain primary adopters. They are increasingly selective — prioritizing multi-use platforms, low-dose imaging, and integrated diagnostics that reduce downstream procedural risk and chair-time.

- Consolidation opportunity: Market concentration is high — the top three vendors account for roughly 58% of market activity and the top five for nearly 79% — creating both barriers and acquisition targets for challengers and investors.

Core report deliverables — practical content for execution

The PW Consulting Cone Beam Imaging CBCT Market report is designed as a practitioner’s toolkit rather than an academic monograph. Highlights include:

Cone Beam Imaging Cbct Market

- Verified market sizing and a transparent forecasting model (2026–2032) with scenario stress-tests for price erosion, reimbursement shifts, and accelerated AI adoption.

- Commercial playbooks for three buyer segments (hospital imaging departments, dental group practices, and specialized orthopedic/weight-bearing clinics) including procurement criteria, expected purchasing cycles, and financing options.

- Vendor benchmarking: product feature matrices, clinical use-case fit, go-to-market channels, pricing strategies, and after-sales service models.

- Regulatory & reimbursement guide: pathway maps for Class II devices and software-as-a-medical-device (SaMD) submissions, plus a lobbying and evidence-generation roadmap to improve reimbursement prospects.

- Investment and M&A module: target screening criteria, valuation sensitivity analyses, and integration playbooks for bolt-on acquisitions or capability partnerships (e.g., AI firms).

- Primary-research appendices: customer interviews, procurement decision trees, and anonymized purchasing data to validate commercial assumptions.

Note: To preserve the utility of this preview and protect premium research assets, the detailed regional and application-level splits, unit economics and vendor share tables are withheld here and available only in the full report package.

Competitive landscape — positioning and implications

The CBCT market is shaped by a mix of legacy imaging OEMs, specialized dental device companies, and emerging AI software vendors. Representative strategic positions we profile include:

- Dentsply Sirona (Charlotte, NC, USA) — a strong integrated-dental-systems player whose CBCT portfolio emphasizes workflow integration and treatment-planning software. Their competitive advantage lies in installed base and clinic-level software ecosystems; the tactical imperative is to accelerate cloud-based services and subscription models to monetize clinical workflow data.

- Planmeca Oy (Helsinki, Finland) — notable for low-dose imaging and 3D/face-scan integration. Their product launches for North America reinforce a deliberate premium positioning; continued focus on clinician ergonomics and cross-modality integration will defend premium pricing.

- VATECH Co., Ltd. (South Korea) — a cost-competitive innovator with auto-switching and image quality credentials. Opportunity exists to pair their hardware with Western AI partners to penetrate higher-reimbursement markets.

- Carestream Dental (Atlanta, GA, USA) — multi-FOV and AI-enhanced systems make them attractive to groups seeking versatile platforms. Their path forward requires demonstrating measurable workflow and diagnostic ROI to buyers that prioritize fast payback periods.

- J. Morita MFG., Cefla/NewTom, Asahi Roentgen, PreXion — each maintains niche strengths in high-resolution imaging, clinical specialization (endodontics, maxillofacial), or geographic distribution. These firms are logical partners or targets depending on strategic priorities: product depth vs. distribution breadth.

- CurveBeam AI and other extremity-focused vendors — carve out valuable orthopedic and weight-bearing use cases that are less crowded and could command differentiated reimbursement or pricing.

Complementing hardware incumbents, AI players such as Overjet, Pearl, and Orca Dental AI have advanced regulatory progress: Overjet and Pearl secured FDA clearances in 2025 for CBCT/3D analysis, with Orca/CephX following in early 2026. These approvals materially change competitive dynamics by making diagnostic AI a purchasable feature rather than an experimental differentiator.

Market dynamics, tailwinds and headwinds

- Demand drivers: increasing procedural volume in implantology and orthodontics, clinician preference for 3D planning to reduce complication rates, and broader acceptance of low-dose devices in private-practice settings.

- Technology drivers: tighter integration of facial scanning, multi-FOV options, and AI-led diagnostics will convert CBCT from an imaging product into a decision-support platform.

- Regulatory & reimbursement constraints: while regulatory pathways for AI-enabled CBCT modules are maturing, reimbursement remains patchy. Limited comprehensive reimbursement for CBCT versus conventional imaging constrains adoption velocity in some markets.

- Buyer sophistication: hospitals continue to be major end-users given their capital budgets and need for high-capacity, multi-patient systems. Dental chains and specialist clinics are increasingly professionalized and demand evidence-based ROI and financing flexibility.

- Supply considerations: capital intensity and long replacement cycles blunt price competition but increase the value of bundled services (training, maintenance, software updates).

Strategic playbook for 2026 (for OEMs, CE Partners, and Investors)

- Prioritize regulated AI partnerships: secure FDA-cleared integrations to support near-term commercial conversations; regulatory clearance is now a hygiene factor in many buyers’ RFPs.

- Design financing-led offers: leasing, pay-per-scan and revenue-share models lower buyer barriers and accelerate installed-base expansion.

- Focus go-to-market by buyer segment: hospitals prioritize throughput and multi-use capability; dental groups prioritize training and predictable maintenance; orthopedic adopters prioritize weight-bearing and extremity workflows.

- Invest in clinical evidence: publish real-world impact studies showing reduced procedure times, improved implant placement accuracy, or diagnostic yield improvements to unlock purchasing committees and drive reimbursement engagement.

- Prepare for consolidation: target tuck-in acquisitions that add AI, software-as-a-service, or distribution reach rather than duplicative hardware lines.

- Mitigate regulatory and reimbursement risk by building modular product architectures that allow software updates and separate software monetization streams.

Why PW Consulting’s CBCT report is different

- Operational focus — our output includes executable GTM playbooks, contract language templates, and a financial model that maps product changes to EBITDA impact.

- Proprietary synthesis — we combine primary interviews with procurement data and regulatory filings to triangulate realistic adoption curves rather than optimistic vendor forecasts.

- Decision-ready outputs — scenario-based capital-budget templates, M&A screening criteria, and a prioritized action list for 100/200/500-day implementations.

Next steps — how to use this intelligence in 2026

Executives planning 2026 roadmaps should use the report to: validate R&D priorities against market ROI; structure partnerships with AI vendors and cloud platforms; and adopt commercial models that reduce buyer capital friction. For private equity and corporate development teams, the report identifies acquisition archetypes and valuation sensitivities that reflect real-world adoption barriers and upside from AI-enabled services.

To preserve the actionable advantage for subscribers, this preview omits the full regional and application-level detail, unit economics and vendor share tables that underpin our recommendations. For the complete dataset (including country-by-country splits, application-level forecasts, product-level pricing benchmarks, and downloadable financial models), visit the PW Consulting report page or contact our industry team for a tailored briefing and sample dataset.

For detailed analysis of this topic, please visit the official page:Cone Beam Imaging Cbct Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com