Black Beer Market 2026 Strategic Brief: What Boards and Executives Must Know

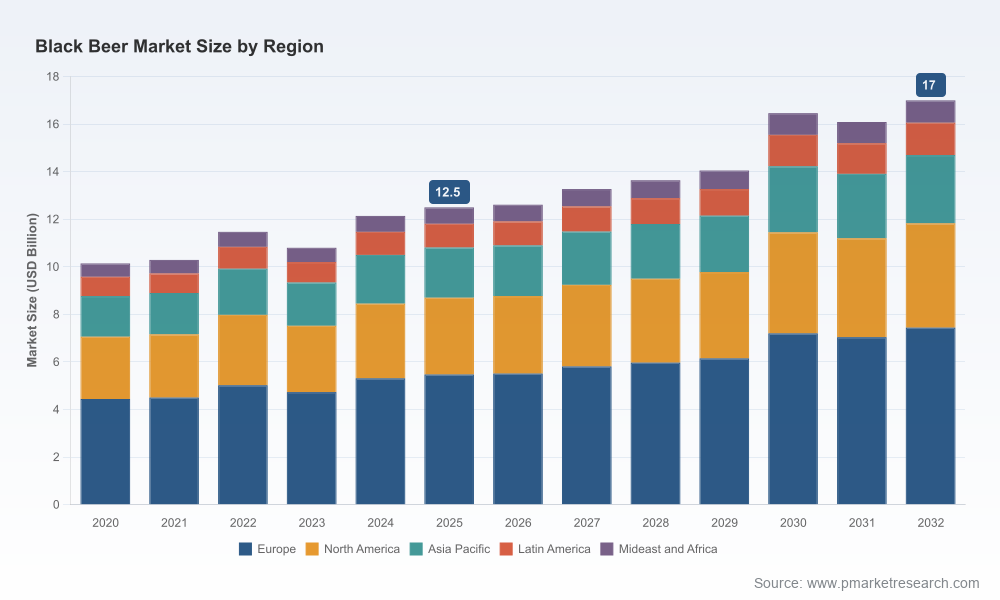

PW Consulting’s latest Black Beer Market report (base year 2025) provides a focused, decision-ready synthesis for leaders preparing strategy, M&A, and commercial plans for 2026. The market reached approximately USD 12.5 Billion in 2025 and—under our central case—continues to grow at a mid-single-digit compound annual growth rate (CAGR) of ~4.5% through the 2026–2032 forecast window. That trajectory masks important asymmetries: pockets of premiumization and craft-led innovation are generating disproportionate margin expansion even as upstream raw material dynamics compress cost flexibility for mainstream SKUs. This briefing highlights the strategic takeaways we believe should shape boardroom choices in the coming 12–18 months; the full report supplies the granular segmentation, scenario matrices, and executable playbooks referenced below.

Black Beer Market

Executive snapshot — six implications for 2026 planning

- Growth remains constructive: the overall market is expanding steadily after a period of volatility; growth is driven by premium variants and episodic innovation rather than uniform volume recovery.

- Premiumization is profitable: value capture in barrel-aged and specialty dark beers materially outperforms commodity dark lager variants on a margin-per-liter basis.

- Consolidation dynamics persist: market concentration is meaningful—top incumbents maintain nearly half the market collectively—creating both partners and competitors for challengers.

- Input-cost sensitivity is acute: malting barley dynamics and softening global barley prices create a narrow window for reinvesting savings into R&D and marketing.

- Channel nuance matters: on-trade and off-trade pathways demand distinct propositions (format, pack size, and experiential positioning) that can materially affect velocity and lifetime value.

- Execution, not insight, will separate winners: companies with fast innovation cycles, flexible supply chains, and premium route-to-market capabilities will capture the bulk of upside.

Why this matters for 2026 decision-makers

For CEOs, CFOs, and commercial heads, the near-term question is not whether the category will grow but where to allocate constrained resources to maximize ROI. Our analysis shows that modest reallocation—shifting marketing and innovation budget toward premium variants, committed barrel programs, and export-ready formulations—can amplify returns materially. For private-equity sponsors and corporate development teams, the combination of persistent concentration and a vibrant craft sub-sector creates attractive arbitrage opportunities: bolt-on acquisitions, capacity investments in barrel aging and co-pack agreements, and selective international roll-outs can accelerate scale and de-risk product-level volatility.

Black Beer Market

Board-level choices in 2026 should therefore revolve around three linked trade-offs: (1) speed of market entry for high-margin innovations versus capital intensity of capacity conversion; (2) investment in vertical sourcing or financial hedges to mitigate barley and malting costs; and (3) concentration of go-to-market efforts in the channels where premiumization is most monetizable. PW Consulting’s report translates these trade-offs into playable options with quantified P&L and balance-sheet implications under multiple macro scenarios.

Black Beer Market

Market drivers and headwinds — what will move margins and volumes?

- Consumer taste bifurcation: Sustained interest in full-bodied stouts, barrel-aged variants, and experimentally flavored dark ales supports premium ASP (average selling price) expansion. These segments also exhibit higher promotional resilience than commodity SKUs.

- Raw material and input dynamics: US barley farm prices and global barley availability remain central to cost pass-through strategies. For context, US barley farm prices in March 2026 averaged roughly USD 5.50 per bushel, while broader global pricing softened through 2025 with analysts tracking mid-single-digit price ranges per kilogram. Simultaneously, malting barley use in the US has shown structural decline, which alters malting capacity utilization and supplier bargaining power.

- Distribution evolution: On-trade experiences (tasting rooms, barrel-aged events) are an engine for premium niche growth, while off-trade channel sophistication (premium packaging, multi-packs) accelerates household trial. Companies that master channel-differentiated assortments will protect margin and velocity.

- Innovation cadence and seasonality: Barrel-aged and limited-edition releases continue to shape consumer calendars and wholesale purchasing cycles; powering a reliable annual cadence is as important as the single hit product.

Competitive landscape — what incumbents and challengers are doing

Industry structure is led by a mix of global incumbent brewers and regionally influential craft specialists. The category’s leaders combine scale-led distribution with iconic brands; smaller players drive flavour innovation and premiumization. Key dynamics we observe across the competitive set include strategic use of craft acquisitions, investment in experiential platforms, and portfolio stretching into barrel- and specialty-led formats.

- Diageo (Guinness): Maintains the archetypal stout franchise through global production and brand stewardship. Their capability in scaling stout-consistent quality across geographies creates defensive value and export optionality.

- Anheuser-Busch InBev (via craft subsidiaries): Deploys craft acquisitions and marquee seasonal lines to access premium dynamics—an illustrative recent move was the 2025 Bourbon County family relaunch from a Goose Island-led unit, signaling continued investment in barrel-aged storytelling.

- Sierra Nevada Brewing Co. and Brooklyn Brewery: These craft leaders combine technical brewing depth with premium packaging and storytelling; their barrel-aging and limited-release strategies set consumer expectations and create premium price benchmarks.

- Heineken N.V. and Carlsberg: Both global brewers are selectively leveraging portfolio diversity and craft partnerships to defend core volumes while participating in the premium segment without materially altering their mainstream footprint.

From a strategic perspective, the incumbents’ playbooks provide three transferable lessons: invest early in scalable barrel-capacity, protect brand heritage while enabling experimental sub-brands, and use seasonal scarcity to sustain pricing power.

Strategic priorities — PW Consulting’s recommended 2026 playbook

- Prioritise premium SKUs with a clear pathway to margin: fast-follower programs that use contract aging or co-packing reduce capital intensity while validating consumer demand.

- Implement proactive raw-material strategies: a combined approach using supplier partnerships, selective on-farm contracts, and targeted financial hedges will stabilize cost of goods sold and free up margin for marketing investments.

- Design channel-specific offerings: develop differentiated packs, pricing, and narratives for on-trade experiences versus off-trade household consumption to maximise lifetime value.

- Accelerate innovation ops: shorten product-development cycles, create barrel-aging pipelines, and formalize limited-release calendars to sustain headline-grabbing drops without disrupting core SKUs.

- Use M&A and partnerships tactically: given the category’s concentration, pursue tuck-ins that add production flexibility or geographic reach rather than headline M&A that merely increases scale without strategic fit.

- Measure what matters: deploy SKU-level economics, elasticity testing, and a rolling 12–18 month scenario plan to keep commercial execution adaptive under input cost volatility.

What the full PW Consulting report delivers (teaser)

Our comprehensive deliverable is designed for hands-on deployment by strategy, commercial, and M&A teams. Highlights include:

- Robust market sizing and rolling forecasts (2026–2032) with scenario-based upside/downside pathways.

- Concentration and competitor mapping with capability and gap analysis for global leaders and select craft challengers.

- Actionable playbooks: go-to-market templates for on-trade and off-trade, SKU rationalization frameworks, trade promotion optimization, and packaging roadmaps.

- Operational tools: capex prioritization model for barrel and fermentation capacity, supplier risk heatmaps, and a raw-material sensitivity dashboard calibrated to recent barley-price movements.

- M&A screening criteria and a prioritized list of archetypal targets (by capability, not disclosed here), including near-term integration checklists and value capture timing.

- Proprietary consumer segmentation, pricing elasticity estimates, and primary interview insights from brewers, distributors, and on-trade operators.

Consistent with the “trailer” principle, the above is deliberately high-level: the primary segmentation tables, SKU-level forecasts, and regional breakdowns are available exclusively in the full report to preserve competitive advantage and to support confidential client workshops.

How to use this intelligence in 90 days

- Quarter 1: Run a rapid portfolio stress test—identify the top 3 SKUs or sub-brands to accelerate into barrel programs or premium relaunches.

- Quarter 2: Lock in supply agreements and implement raw-material hedges; deploy pilot co-pack arrangements to validate demand before capex commitment.

- Quarter 3: Execute channel-differentiated launch campaigns and evaluate tuck-in M&A opportunities against our integration readiness scorecard.

PW Consulting’s Black Beer Market report is built to convert insight into action. If your 2026 planning cycle includes portfolio pivots, M&A options, or a need to re-price and reposition in response to both consumer premiumization and input-cost pressures, this is the intelligence package to inform those decisions. For access to the full dataset, SKU-level forecasts, and downloadable toolkits that support board-level decision-making, please consult the report landing page or contact PW Consulting’s industry desk for a tailored briefing and workshop.

For detailed analysis of this topic, please visit the official page:Black Beer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com