C9 Petroleum Resin Market: Strategic Imperatives for 2026 — PW Consulting Announces New In‑Depth Market Intelligence

PW Consulting today releases a strategic preview of our forthcoming C9 Petroleum Resin Market report, designed to equip senior executives, corporate strategy teams, and investment committees with the actionable intelligence required to make high‑stakes decisions in 2026. Our analysis distills a complex value chain — from ethylene cracker operations through resin manufacturing and end‑use formulation — into a decision‑oriented playbook that balances near‑term commercial priorities with medium‑term resilience planning.

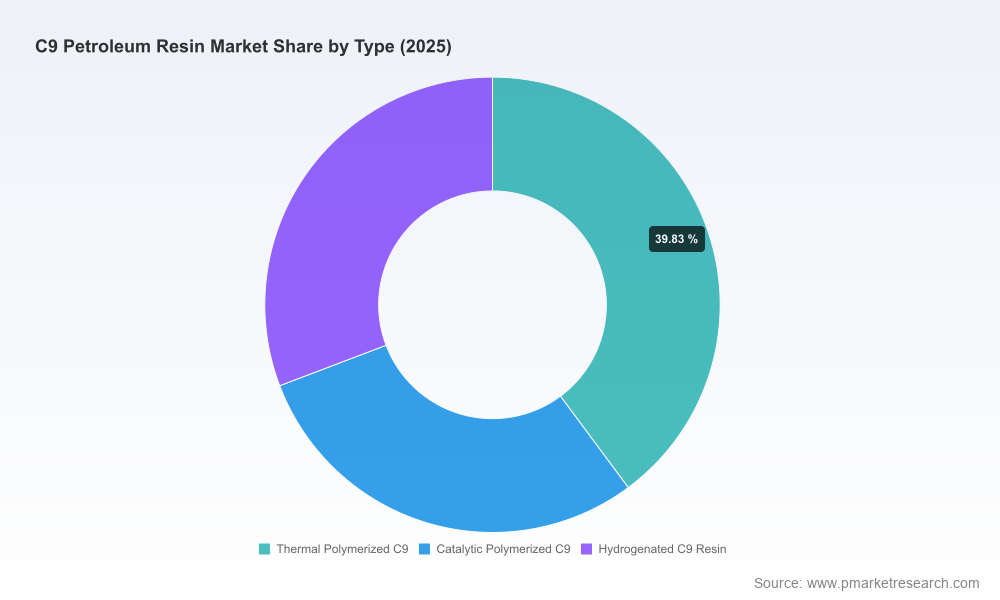

C9 Petroleum Resin Market

Market trajectory at a glance

The C9 petroleum resin market has demonstrated steady expansion over the last half decade, rising from just over USD 1.36 billion in 2020 to approximately USD 1.72 billion in 2025. Our proprietary market model projects continued growth through the forecast window (2026–2032) at a compound annual growth rate (CAGR) of 4.85%, reaching roughly USD 2.40 billion by 2032. These aggregate dynamics frame a market that is mature, cyclical, and yet receptive to product and feedstock‑driven differentiation.

C9 Petroleum Resin Market

Why this matters for 2026 decision‑makers

- Supply security has become a strategic variable: Resin production is intrinsically linked to the availability of the C9 aromatic fraction from steam cracking. Shifts in cracker feedstock choice (notably the move toward ethane cracking) materially reduce C9 byproduct volumes, creating periods of constrained supply and elevated price volatility. Corporates must treat C9 sourcing as a component of their upstream risk management, not just a procurement line item.

- Margin pressure is feedstock‑sensitive: Historical price swings in naphtha and cracker economics translate rapidly to resin margins. For 2026, our scenario work highlights that producers with integrated feedstock access or flexible feedstock contracts retain a decisive advantage in both pricing and allocation during tight markets.

- Regulatory and product risk is low but evolving: Hydrocarbon resins, including C9 types, are broadly assessed as low hazard by contemporary regulatory frameworks and often qualify for polymer reporting relief. While this reduces near‑term compliance drag, emerging sustainability expectations and formulation constraints in specific geographies require proactive product stewardship to defend market access.

What the PW Consulting report delivers — practical, executable intelligence

Our report is intentionally tactical and built for implementation. We provide:

C9 Petroleum Resin Market

- an integrated market model that reconciles historical trade flows, domestic production, and implicit byproduct routing from steam crackers — delivered in an Excel workbook to enable client‑side scenario runs;

- price sensitivity and margin maps that link upstream feedstock scenarios to downstream resin pricing and producer profitability under different operational configurations;

- a supplier scorecard and capacity map that evaluates manufacturers on feedstock security, product breadth, quality consistency, geographic reach, and commercial responsiveness;

- an M&A and partnership screening framework identifying target profiles that deliver strategic value (e.g., regional supply anchors, technology holders, specialty grade capabilities);

- regulatory impact matrices and a compliance readiness checklist aligned to major markets; and

- a tactical 18‑month playbook for procurement, operations, and R&D leaders that sequences actions to protect margins and capture growth in higher‑value applications.

To preserve the strategic value of this work for our clients, the public preview establishes the directional findings while the complete dataset, segment tables and supplier financials remain available in the full report and accompanying model.

Competitive landscape — who matters and why

The C9 resin market exhibits moderate concentration: the top three producers account for a meaningful share of global capacity, while the top five command just over half of the market. This structure produces a dual market dynamic — nimble domestic producers able to serve local formulations quickly, and larger, vertically integrated players that can compete on feedstock assurance and global distribution.

- Vertical integrators and legacy players: Firms with integrated petrochemical operations — including large multinational chemical companies — have strategic advantages in feedstock access and scale. Their ability to reallocate aromatic C9 fractions internally or to downstream customers makes them default partners for large formulators seeking reliability.

- Specialized regional champions: Longstanding domestic producers that focus on C9 grades and specialty formulations retain strong positions in their home markets by combining rapid customer service with deep technical support for adhesives, coatings, and rubber compounding. These players are often the first choice for customers prioritizing security of supply and formulation stability.

- Emerging low‑cost exporters: Several producers in cost‑competitive regions have expanded capacity and product ranges, creating arbitrage opportunities — and competitive pressure — in commodity resin grades globally. These manufacturers are increasingly relevant to buyers seeking blended sourcing strategies.

Strategically, 2026 will be the year to choose between two paths: reinforce supply via partnerships and integration, or pursue differentiation via specialty grades and formulation excellence. Both routes are viable, but require different investments and operating models.

Profiles and implications — selected industry participants

- Kolon Industries (South Korea): A domestic leader in hydrocarbon resins with noted innovation in crosslinkable resins and a strong foothold in adhesives and coatings. Their product development focus makes them an attractive technical partner for formulators pursuing higher‑performance formulations.

- Neville Chemical (USA): A legacy manufacturer with multi‑decade experience supplying C9 aromatics domestically. Their secure domestic supply position is strategically useful to companies seeking to insulate North American operations from export variability.

- Eastman, ExxonMobil & large multinationals: These integrated players leverage feedstock synergies and global logistics networks. Their strategic value lies in supply stability and the ability to scale specialty C9 derivatives with consistent quality.

- Cray Valley (TotalEnergies subsidiary) and regional producers: Active investment and product portfolio expansion from these players signal ongoing consolidation and premiumization trends in adhesives, inks, and specialty coatings segments.

- Chinese producers (multiple mid‑size and large firms): A broad cohort of manufacturers offers competitive pricing and increasing technical depth. For buyers, these firms are important considerations for blended sourcing, but require robust supplier qualification and quality assurance processes.

Feedstock, regulation and the operational levers that matter

- Feedstock availability: C9 resin output is a byproduct of steam cracking operations. Shifts toward ethane as cracker feedstock materially reduce C9 yields relative to naphtha cracking. Procurement teams must therefore incorporate cracker feedstock mix into supply risk assessments and contract negotiations.

- Price volatility: Upstream naphtha and C9 fraction pricing remain primary drivers of resin margins. Active hedging strategies, flexible tolling arrangements, and secured long‑term offtakes are practical mitigants.

- Regulatory posture: Hydrocarbon resins benefit from regulatory classifications that lower immediate compliance burdens in certain jurisdictions, but sustainability scrutiny (e.g., lifecycle carbon, VOCs in formulations) is increasing among large formulators and OEMs. Product innovation that improves environmental profile will become a differentiator.

Strategic actions for 2026 — an executive checklist

- Embed feedstock scenario planning into procurement and product roadmaps — model ethane adoption and episodic naphtha spikes against margin and allocation outcomes.

- Prioritize supplier diversity through a mix of integrated producers for security and regional specialists for responsiveness; qualify at least two alternate suppliers per major production node.

- Invest in product differentiation (hydrogenated and specialty grades) to escape commodity pricing cycles and capture higher margin segments.

- Explore partnerships, tolling, or minority investments in regional producers as low‑risk routes to capacity assurance and market access.

- Implement an early‑warning regulatory dashboard and a sustainability roadmap focused on VOC performance and supply‑chain emissions transparency.

How PW Consulting’s deliverables accelerate decision cycles

Our report is built to shorten analysis lead times and convert insights into executable programs. Subscribers receive the forecast model, supplier scorecards, and a prioritized action matrix that translates strategic choices into measurable KPIs and six‑month milestones. For boards and executive teams, this means faster, less contentious decisions when supply stress or pricing shocks require immediate responses.

Next steps

This release serves as a strategic preview. The full PW Consulting C9 Petroleum Resin Market report contains the granular segment tables, regional and application forecasts, in‑depth supplier profiles, and a downloadable model for scenario testing. If your 2026 plans depend on securing resin supply, optimizing margin, or evaluating M&A and partnership options, the full deliverable is engineered to be the operational backbone of your decision process.

Contact PW Consulting to access the complete report, licensing options for the model, and bespoke advisory engagements that tailor the insights to your company’s portfolio and risk posture.

For detailed analysis of this topic, please visit the official page:C9 Petroleum Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com