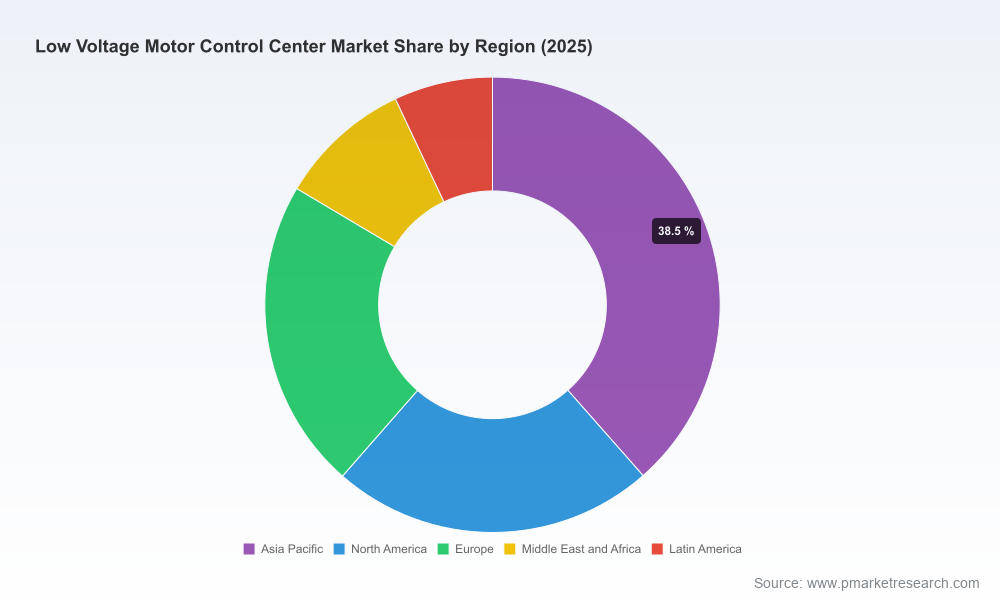

Low Voltage Motor Control Center Market: Strategic Preview for 2026 — PW Consulting Industry Brief

Executive summary

PW Consulting’s new Low Voltage (LV) Motor Control Center (MCC) Market briefing frames the strategic choices facing industrial electrification leaders as 2026 decisions are being made. The market has moved from roughly USD 4.2 billion in 2020 to about USD 5.74 billion in 2025 and is projected to expand to roughly USD 6.04 billion in 2026 and to USD 8.68 billion by 2032, reflecting a compound annual growth rate (CAGR) of approximately 6.1% over the forecast horizon. That steady expansion masks important technology, regulatory and supply-side inflections that will determine winners and losers over the next planning cycle.

Low Voltage Motor Control Center Market

Why this briefing matters to executives in 2026

- Timing: Capital and product roadmaps set in 2026 will influence commercial outcomes across the 2026–2032 forecast period; the choices you make now compound through product lifecycles, aftermarket revenue, and service footprints.

- Complexity: LV MCCs are no longer commodity switchgear; they sit at the confluence of safety engineering, automation, energy management and digital services. That intersection changes procurement criteria, margin pools and partnership strategies.

- Decision clarity: Our report translates macro growth into actionable strategic options—portfolio prioritization, go‑to‑market segmentation, M&A screening criteria, and operational hedges—without exposing the proprietary micro‑slices that provide competitive advantage. Consider this a high‑resolution map that points to the coordinates you will want to examine in the full report.

Market trajectory and what the numbers hide

The LV MCC market’s historical growth and the 6.1% CAGR we model are driven by three interacting vectors: rising energy-efficiency mandates and automation, heightened workplace safety and insurance requirements, and steady industrial investment in power distribution and retrofit projects. While headline growth is resilient, the composition of demand is shifting toward higher‑value offerings—intelligent MCCs, integrated VFD architectures, and arc‑resistant constructions—each with distinct margin and service profiles.

Low Voltage Motor Control Center Market

Historical baseline: our modeling traces market value from the low‑teens of billions of USD annually in the early 2020s to a mid‑single‑digit billion base in 2025, and a trajectory that accelerates as digitalization and retrofit cycles converge. These aggregated numbers conceal micro‑segment dynamics that materially affect product economics—information available in the full report to licensed clients.

Low Voltage Motor Control Center Market

Report content—operationalized for decision makers

This briefing is a window into a larger, execution‑oriented study that delivers:

- Bottom‑up market sizing and demand-modeling (2020–2025 historical, 2026–2032 forecast) with scenario variants tuned to automation adoption and capex cycles.

- Technology and product roadmaps that isolate where value accrues: control intelligence, VFD integration, arc‑resistant design, modularity, and energy‑monitoring functions.

- Regulatory and standards impact analysis (including IEC 61439 family implications and safety feature adoption) and how compliance choices affect total cost of ownership and insurance exposure.

- Supply‑chain assessments highlighting raw material volatility (notably steel) and lead‑time stress points along with procurement hedging strategies.

- Commercial playbooks for OEMs, system integrators and aftermarket specialists—pricing architectures, service bundles, digital subscription constructs, and channel strategies.

- A vendor benchmarking matrix, competitive scenario analysis, and acquisition target screen tuned to CR3/CR5 concentration dynamics and product adjacency.

- Implementation checklists, procurement RFP templates, and a prioritized 18‑month action plan for executives.

Competitive landscape: what the leading vendors are placing their bets on

The LV MCC market is moderately concentrated at the top; the largest vendors capture a meaningful share of incumbent project and retrofit spend, but there remains ample room for niche players and region‑focused specialists. The competitive environment reflects divergent strategies:

- ABB Ltd. (Zurich): Emphasizes safety and digital integration with product families that include arc flash mitigation and intelligent monitoring. ABB’s ReliaGear positioning focuses on safety-first engineering combined with plug‑and‑play starters to shorten integration windows.

- Schneider Electric SE (Rueil‑Malmaison): Markets modular, arc‑resistant architectures and leans heavily into connectivity through EcoStruxure. Their product programs are designed to simplify predictive maintenance rollouts for customers pursuing energy efficiency mandates.

- Eaton Corporation plc (Dublin): Concentrates on safety and reliability with arc‑resistant variants and close integration with variable frequency drives (VFDs), targeting heavy industry requirements for ruggedness and uptime.

- Siemens AG (Munich): Focuses on IoT‑enabled motor and energy management capabilities within MCC platforms, aimed at customers that want enterprise‑grade telemetry and standards compliance.

- Rockwell Automation (Milwaukee): Aggressively pushing modular and data‑rich MCC solutions (e.g., the FLEXLINE 3500 family) designed for real‑time diagnostics, energy monitoring and rapid OEM integration—demonstrated at international exhibitions and product launches.

- Regional and specialized players (WEG, Mitsubishi Electric, GE, Powell Industries, Tesco Controls, Fuji Electric, Larsen & Toubro, Allis Electric, RESA Power): These companies compete on customization, local service, remanufacture/retrofit capabilities and cost‑to‑serve advantages in specific industrial segments or geographies.

Recent activity—product introductions, trade‑show roadmaps and service expansions—confirms that vendors are shifting R&D and GTM spend toward intelligent, safety‑enhanced and retrofit‑friendly MCCs. For example, Rockwell’s FLEXLINE 3500 launch and WEG’s 2026 trade show presence both underscore the market’s tilt toward energy transition and connected systems.

Key dynamics shaping supplier and buyer economics

- Standards and safety: Compliance with international standards (notably the IEC 61439 family) and growing demand for arc‑resistant features change engineering BOMs and testing requirements. Buyers must budget for higher capital intensity in safety‑critical installations.

- Digitalization premium: Integration of VFDs, energy meters, and IoT endpoints creates opportunities for software and services revenue, but it also demands new capabilities in cybersecurity, data management and systems integration.

- Supply‑chain exposure: Steel price elevation and volatility into 2026 materially affects enclosure costs and lead times. Sourcing strategies, long‑lead inventory, and design‑to‑cost programs will be differentiators.

- Aftermarket opportunity: As intelligent MCCs proliferate, aftermarket services—remote monitoring, predictive maintenance contracts and retrofitting legacy MCCs—become a high‑margin growth engine.

Strategic imperatives for 2026

For executive teams deciding near‑term capital and portfolio moves, we recommend a three‑track approach:

- Product and R&D: Prioritize modular architectures that enable both conventional and intelligent configurations from a common platform. Invest selectively in arc‑resistant options and validated integration with VFDs and energy‑monitoring stacks to meet tightening safety and efficiency mandates.

- Go‑to‑market and services: Build recurring revenue engines around remote diagnostics and retrofits. For OEMs and integrators, design service bundles that monetize digital data streams and extend asset life for critical customers.

- Supply‑chain and operations: Implement raw‑material hedges and dual‑sourcing for key enclosure elements. Rework procurement frameworks to include lead‑time clauses and escalation ladders that reflect steel market realities heading into 2026.

Risk matrix and mitigation

- Regulatory shifts: Rapid changes in safety or efficiency regulations can force redesigns. Mitigation: maintain a standards‑watch function and modular electrical design that isolates regulatory exposure.

- Technology obsolescence: Failure to support IoT and VFD integration will relegate products to price competition. Mitigation: partner with control platform vendors and adopt open communications standards.

- Market concentration: A moderate top‑tier concentration exists, but niche competition is robust. Mitigation: target underserved verticals and develop retrofit offerings that bypass incumbent procurement cycles.

How boards and executive teams should use this briefing

This industry preview is designed to shape 2026 strategic planning conversations. Use it to prioritize which questions to scope into the full PW Consulting study that will provide the granular segmentation, financial tables and supplier scorecards required to underwrite investments. Specifically, expect to use the full report to:

- Validate product‑level IRR projections for new intelligent MCC lines.

- Craft M&A screening criteria focused on software, retrofit capabilities and local manufacturing assets.

- Build three‑year service revenue targets and define field‑service coverage investments.

Conclusion and next step

The LV MCC market is no longer a simple infrastructure buy. From 2026 onward, market growth will be shaped less by volume sales and more by how vendors deliver safety, connectivity and lifecycle services. PW Consulting’s full study contains the granular segmentation, vendor scorecards and executable playbooks necessary to convert macro trends into boardroom decisions. This briefing highlights the strategic inflection points; the paid report provides the exact coordinates for operational moves.

To access the detailed models, scenario outputs and vendor matrices that underpin these findings, please visit our report landing page or contact PW Consulting’s industry team for a licensed copy and a guided executive briefing.

For detailed analysis of this topic, please visit the official page:Low Voltage Motor Control Center Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com