Cell and Tissue Culture Bags Market: Strategic Intelligence for 2026 Decision-Making

PW Consulting’s new market study on Cell and Tissue Culture Bags provides a strategic playbook for leadership teams planning investments, procurement, and product roadmaps in 2026 and beyond. Built on a five‑year historical base (2020–2025) and forward-looking across 2026–2032, the study synthesizes market sizing, demand drivers, manufacturing constraints, regulatory dynamics, and competitive positioning into an actionable set of scenarios. The core market is expanding robustly — clocking a compound annual growth rate (CAGR) of 9.85% from the 2025 base year — and our analysis shows the total market doubled in the last six years, creating both scale opportunities and tactical bottlenecks for established and emerging players alike.

Cell And Tissue Culture Bags Market

Why this study matters to executives in 2026

- Timing: 2026 is a watershed year for the single‑use ecosystem. Capital investment decisions initiated today will determine supply footprints and validation timelines that intersect with peak demand across cell therapy manufacturing and broader bioprocessing applications over the next five years.

- Clarity: Buyers face a wider choice set — from commodity polyethylene films to engineered FEP/EVA offerings — with meaningful differences in extractables, gas transmission, and regulatory validation effort. Our report translates these technical trade‑offs into procurement scorecards.

- Risk mitigation: Supply chain fragility for high‑purity film and assembly capacity is now a boardroom topic. We quantify where constraints are likely to emerge and offer near‑term hedging strategies.

Headline market view (concise)

After steady expansion through 2020–2025, the cell and tissue culture bag market reached a substantial mid‑market size in 2025 (base year of this study). The report models multiple uptake scenarios through 2032, with a central case that reflects a continuation of current commercialization trajectories and a sustained CAGR near 9.85%. Under that central scenario, the market is projected to roughly double from its 2025 level by the end of the forecast window — a growth profile that should prompt reassessment of capacity, supplier terms, and innovation pipelines across the value chain.

Cell And Tissue Culture Bags Market

What the full report delivers (practical, non‑academic)

- Market architecture: a clear map of demand pools (research, biopharma production, cell therapy, diagnostics) and how they interact with single‑use adoption curves.

- Segmentation playbook: decision matrices to prioritize materials (e.g., high‑purity films vs. commodity films) by use case, cost to validate, and supplier risk.

- Supply chain stress tests: scenario models that show where raw‑material bottlenecks or lead‑time shocks appear, with tactical mitigation options (dual sourcing, consignment, strategic stocking thresholds).

- Commercial models: pricing sensitivity analysis and margin compression scenarios for OEMs and toll‑manufacturers under differing demand growth rates.

- Regulatory and quality readiness checklists: practical steps for ISO/cGMP alignment and clinical‑stage validation that reduce time‑to‑market.

- M&A and partnership playbook: target profiles, valuation multiples observed in adjacent single‑use and consumables deals, and integration risks specific to bag manufacturers and film suppliers.

- Case studies: real‑world procurement and scale‑up examples illustrating what worked — and what didn’t — in 2022–2025 manufacturing ramps.

- Stakeholder interviews and primary data: verbatim insights from procurement leads, process engineers, and QA heads across end‑users and suppliers.

Competitive landscape — what to watch

The market shows moderate concentration at the top, with the three largest suppliers together controlling a meaningful share of commercial demand and the top five exerting a clear influence on pricing and standards. This structure creates a dual‑track environment: established vendors are optimizing integration with automation and single‑use bioreactors, while specialized players compete on custom formulations and service models.

Cell And Tissue Culture Bags Market

- OriGen Biomedical (Austin, Texas) — A specialized provider known for PermaLife and Evolve FEP‑based bags tailored to cell expansion, cryopreservation and cell therapy workflows. OriGen’s product profile emphasizes gas permeability and cGMP‑suitable designs. Recent company press through 2026 highlights facility expansions and a stronger focus on regulated manufacturing capability, signaling intent to scale for clinical and commercial cell therapy demand. Their ISO 13485 and MDSAP certifications are important enablers for customers requiring regulated supply chains.

- Charter Medical (Winston‑Salem, North Carolina) — Focused on cell expansion containers (EXP‑Pak, Bio‑Pak) for non‑adherent cell cultures. Charter’s strategic edge is its focus on configurable assemblies and service‑level agreements for process development customers transitioning to manufacturing.

- Thermo Fisher Scientific (Waltham, Massachusetts) — A large ecosystem player offering Gibco branded culture bags that integrate with automated systems and bioreactors, including disposable pre‑filled options. Thermo Fisher’s strength lies in its distribution reach and systems integration capability — an advantage when customers seek single‑source procurement and scale validation across upstream and downstream steps.

- Corning Incorporated (Corning, New York) — Builds cell expansion and rocker bags using gas‑permeable polyolefin films. Corning’s manufacturing and materials legacy supports a performance and quality narrative attractive to bioprocessors prioritizing low extractables and consistent film characteristics.

- Saint‑Gobain (France; life sciences units in USA/Europe) — Positions as a custom supplier optimizing gas transmission and film behavior for T‑cell expansion and other cell therapy use cases. Their go‑to‑market centers on tailored engineering and collaborative development.

- Sartorius (Göttingen, Germany) — Offers Flexsafe RM and STR single‑use bioreactor bags and complementary culture bags for wave and stirred systems. Sartorius competes on integrated single‑use bioprocess systems and product bundles that reduce customer validation scope.

Strategic takeaways: incumbents with systems integration (Thermo Fisher, Sartorius) can capture value downstream by bundling consumables with automation; specialty bag makers (OriGen, Charter) can compete on responsiveness and material expertise; materials and film processors (Corning, Saint‑Gobain) are critical choke points for quality and supply continuity.

Regulatory and technical dynamics that will determine winners

- Quality bar: single‑use bags destined for regulated manufacturing are produced under cGMP and must meet biocompatibility standards such as ISO 10993 and applicable USP guidance. These obligations materially affect lead times and cost, particularly for smaller suppliers scaling into clinical supply.

- Materials: FEP, PE, and EVA films dominate on technical grounds — low extractables, controlled gas permeability, and weldability — but each presents different supply and validation burdens. The report quantifies the validation effort and lifecycle cost differences across major film types.

- Intended use clarity: many commercial bags are labeled for research or manufacturing use and are not direct therapeutic delivery devices without further validation. Buyers must align specifications and change control paths early to avoid rework late in clinical development.

Operational recommendations for 2026

- Fast followers: prioritize dual‑source agreements for high‑purity film and secure long‑lead supply contracts for molded assemblies. Use staged inventory release mechanisms to minimize obsolescence risk.

- OEMs and innovators: invest in pre‑validated system bundles with clear regulatory support packages (validation protocols, extractables datasets) to shorten customer qualification cycles.

- Procurement leaders: implement a supplier scorecard that weights regulatory certifications and validated extractables data more heavily than unit price for clinical manufacturing inputs.

- Investors and M&A teams: look for targets with validated manufacturing for regulated products, proprietary film processing know‑how, or niche clinical stage revenue where consolidation can deliver immediate margin expansion.

What we intentionally hold back (and why)

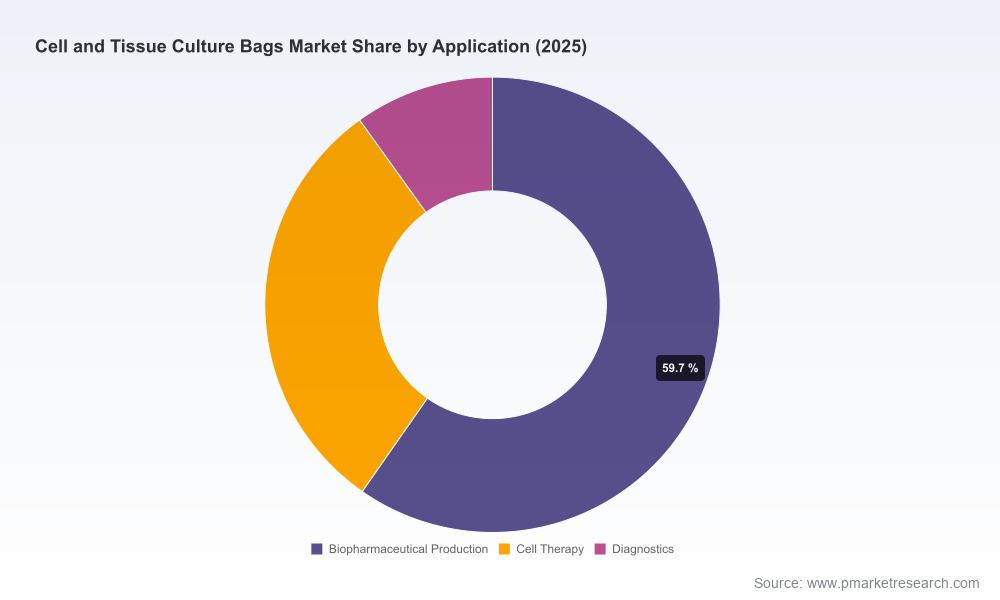

Consistent with the “trailer” design of this release, we present high‑confidence macro sizing, growth trajectory (with a 9.85% CAGR), regulatory context, and company positioning. We do not publish the full regional or application‑level split data, nor the detailed supplier revenue tables, in this brief. Those granular segmentations, supplier share tables, and transaction comps are included in the paid report because they represent the proprietary analysis that buyers rely on to make transaction and procurement decisions.

How to use the full PW Consulting report

When you bring the full report into your planning cycle, use the deliverables as follows:

- Board briefing: extract the scenario model to show capital needs and timing for capacity expansion requests.

- Procurement RFPs: use the supplier scorecards and validation templates to reduce evaluation time and downstream surprises.

- Business development: align product roadmaps to the adoption timelines and clinical inflection points we model by application.

- Risk management: operationalize the supply‑chain stress tests into internal order‑to‑cash and inventory policy updates.

Closing perspective

The cell and tissue culture bag market is maturing from a niche consumables market into a predictable, strategic component of the cell‑therapy and bioprocessing supply chain. For leaders making decisions in 2026, the choice is no longer about whether to engage with single‑use culture systems — it is about how to secure validated supply, differentiate through service and integration, and use materials expertise as a defensible moat. PW Consulting’s report provides the quantitative backbone and executable playbook for those steps; for the granular segmentation tables, supplier revenue models, and potential acquisition targets, the full study remains the authoritative next step.

To request access to the full Cell and Tissue Culture Bags Market Report (base year 2025; forecast 2026–2032), and to receive our proprietary supplier matrices and scenario models, contact PW Consulting’s Research Sales team via the official report page.

For detailed analysis of this topic, please visit the official page:Cell And Tissue Culture Bags Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com