How to Make Custom Donut Boxes That Boost Sales

Other |

2026-04-08 14:32:16

PW Consulting’s new Port Wine Market report (base year 2025; forecast period 2026–2032) equips senior leadership with the analytical foundations and operational playbooks required to navigate a market at the intersection of constrained supply, asymmetric demand recovery, and tightening regulation. The global Port wine market reached approximately USD 950 million in 2025 and, under our central-case forecast, is expected to resume steady growth at a 3.2% CAGR across 2026–2032, crossing the USD 1.18 billion threshold by the end of the forecast window. This press release summarizes the strategic value of the report for 2026 planning while preserving core segment-level outputs for subscribers and clients.

Port Wine Market

Supply-side shock and managed scarcity. The Interprofessional Council for the Douro (IVDP) set Port beneficio for 2025 at 75,000 barrels — the lowest in decades — reflecting high stock levels alongside weakening shipments. Coupled with harvest reports indicating lower yields in 2025 at several key estates, the market environment for 2026 is one where availability, not just demand, will drive margin outcomes and release strategies.

Port Wine Market

Regulatory tightening as a strategic variable. Decree‑Law n.º 106/2025 expanded IVDP’s remit on labeling, aging, vinification and alcohol thresholds effective September 2025. Executives must treat regulatory developments as ongoing operating constraints that affect SKU design, packaging lead times, and go‑to‑market approvals.

Port Wine Market

Premiumization and portfolio bifurcation. Leading houses have signalled renewed focus on high-premium vintage and aged Tawny releases — with multiple 2024 Vintage declarations announced in April 2026 — underscoring a two-track market: scarcity-driven premium releases and a broader base of accessible fortified styles. Brands that manage timing and storytelling will capture disproportionate value.

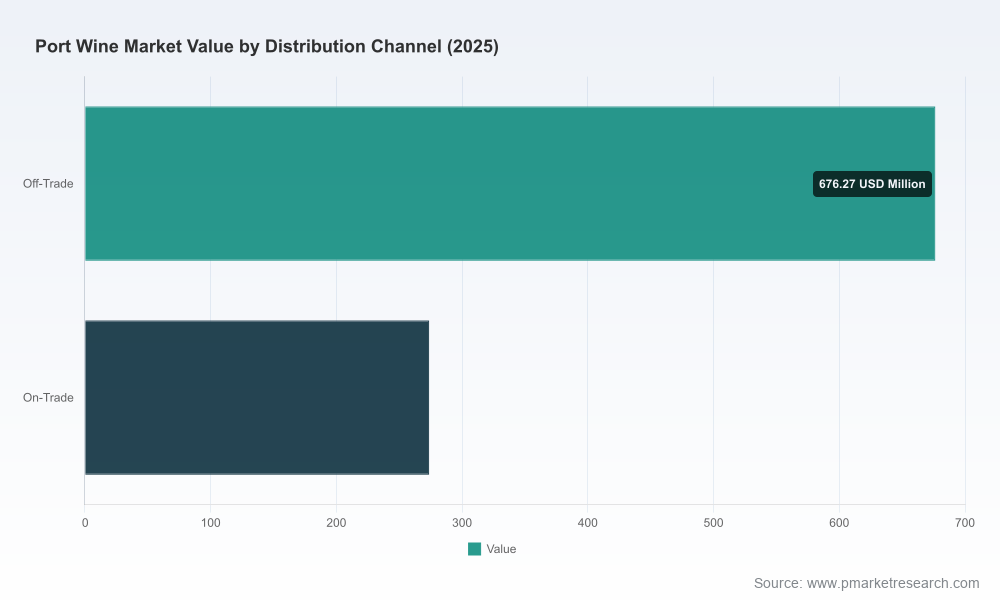

Demand geography and channel shifts. While longer-term structural sales have contracted relative to a 2005 peak (industry analysis indicates approximately a 25% decline in global Port sales since 2005), pockets of export growth and channel reconfiguration (off‑trade strength versus on‑trade recovery patterns) create targeted opportunities for exporters and distributors in 2026.

Scenario-based volume and pricing models calibrated to IVDP quota dynamics, harvest variability, and a range of demand recovery trajectories. These models allow CFOs and supply planners to stress-test outcomes under alternative beneficio, yield, and price elasticity assumptions.

SKU rationalization and release-timing playbooks that reconcile cellar aging constraints with go‑to‑market impact — including decision criteria for vintage declarations, limited releases, and long‑tail Tawny programs.

Channel optimization frameworks for balancing off‑trade, on‑trade and direct‑to‑consumer (DTC) routes, with practical KPIs and trade promotion levers mapped to margin and brand equity outcomes.

Regulatory compliance checklists and labeling decision trees aligned to Decree‑Law n.º 106/2025 and IVDP practice, reducing time‑to‑shelf and legal exposure for export markets.

M&A and partnership screening tools — including concentration analytics (market CR3 ~45%, CR5 ~58%) and acquisition candidate scoring — to support inorganic growth or defensive consolidation strategies.

Ready-to-use executive dashboards, channel-specific margin simulators, inventory and release planning spreadsheets, and a 90/180/360-day activation roadmap for first-mover advantage in 2026.

The Port category remains anchored by historic houses with deep vineyard ownership, cellar capacity and international distribution. Our qualitative and quantitative review highlights three strategic archetypes among incumbent firms:

Integrated premium custodians — houses such as Symington Family Estates and The Fladgate Partnership leverage extensive Douro holdings, long cellar programs and strong vintage track records to command scarcity premiums and orchestrate high-impact declarations. Symington’s April 2026 vintage declaration and its harvest notes indicating lower yields underscore the strategic advantage of estate control when supply tightens.

Global brand distributors — multi-brand groups with broad international footprints (for example, Sogrape Vinhos and Grupo Sogevinus) optimize scale in accessible price bands and leverage global networks to smooth demand volatility, particularly in off‑trade channels.

Innovation and craft specialists — producers like Niepoort, Quinta do Noval and Kopke operate at the intersection of heritage and experimentation, driving consumer interest through single‑plot narratives, rare ungrafted-vine bottlings, and specialized Colheita/Tawny programs.

For potential entrants or investors, market concentration metrics indicate meaningful headroom for differentiated premium plays or scale‑seeking consolidation. For incumbents, the combination of constrained beneficiо volumes and elevated brand equity associated with vintage declarations implies an attractive margin profile for controlled-release strategies.

Lock down upstream supply and build flexible aging plans. Prioritize contracts and vineyard leases, refine cellar-rotation rules, and develop contingency release calendars that accommodate IVDP quota risk. Capital allocation toward selective capacity (botting lines, wood maturation) should be staged according to scenario triggers in the report.

Recalibrate premium vs. core SKUs. Use SKU profitability ladders and SKU rationalization tools to concentrate investment behind highest-return references while maintaining enough breadth to sustain on‑trade and DTC engagement. Consider limited, high‑narrative releases to monetize scarcity without cannibalizing core volumes.

Shift channel economics through targeted commercial agreements. Negotiate guaranteed minimums with key off‑trade partners, develop bespoke on‑trade programs for high-margin venues, and expand DTC capabilities where storytelling and higher ASPs (average selling prices) compensate for logistics complexity.

Proactively manage compliance and reputational risk. Implement labeling and vinification audits against Decree‑Law 106/2025 requirements, and include regulatory scenario outcomes in capital budgeting. Early engagement with IVDP and domestic stakeholders can accelerate approvals and reduce release friction.

Use M&A and strategic partnerships as bolt-on hedges. Pursue small estate or regional co‑ops to secure supply and diversify terroir exposure; explore JV models for targeted market entry in growing export pockets identified in the report.

Executives should track a compact set of leading indicators that the report converts into trigger points for operational responses:

IVDP beneficio announcements and official quota adjustments;

Aggregate harvest yield reports and early vintage declarations from major houses (e.g., recent 2024 declarations from several incumbents);

Regulatory activity in Lisbon affecting labeling and alcohol-level tolerances;

Country-level export flows into targeted markets (we note early 2025 growth into certain markets such as Canada);

On-trade reopening and premium on-premise placement trends in key cities.

The accompanying risk heatmap and decision matrix in the full report translate these inputs into prioritized mitigation actions and budget reallocation sequences for 30/90/180-day horizons.

Our recommended 2026 activation plan is structured as a three-phase roadmap: stabilize, optimize, and capture. Stabilize (0–90 days) focuses on supply‑chain firmness and regulatory clearance; optimize (90–180 days) tunes pricing, assortment and trade agreements; capture (180–360 days) scales DTC programs and executes premium releases timed to market windows. Suggested KPIs include inventory days by vintage cohort, sell‑through of premium limited editions, DTC conversion and lifetime value, average realized price per case, and regulatory cycle times. The report supplies editable KPI dashboards and scorecards to operationalize these metrics.

2026 will be the year in which strategy converts into structural advantage for Port houses and value chain participants. With constrained beneficiо volumes, tighter regulatory oversight, and renewed premium-release activity by leading estates, executives who combine disciplined supply planning with selective premiumization and channel sophistication will capture outsized returns. PW Consulting’s Port Wine Market report provides the quantitative models, tactical checklists, and competitor intelligence necessary to make those calls in 2026 — while also offering bespoke advisory engagements for firms that require implementation support.

Note: This communication highlights key market context, executive actions and competitive dynamics but intentionally omits granular segment-level splits and proprietary model outputs. Subscribers to the full report receive detailed regional, type and channel breakdowns, downloadable scenario models in USD (Million), and an executive workshop package. To access the complete analysis and tools, visit PW Consulting’s report page at www.pwconsulting.com/reports/port-wine-market-2026 or contact our advisory desk for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Port Wine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com