PW Consulting: Strategic Briefing — Water Treatment Equipment in Power Market (Implications for 2026 Decision-Makers)

PW Consulting today publishes an executive briefing drawn from our forthcoming in-depth market research, Water Treatment Equipment in Power Market. The study synthesizes historical performance (2020–2025), delivers a forward-looking forecast through 2032 and translates technical market intelligence into actionable strategic options for power generators, equipment vendors, investors and procurement teams planning for 2026 and beyond.

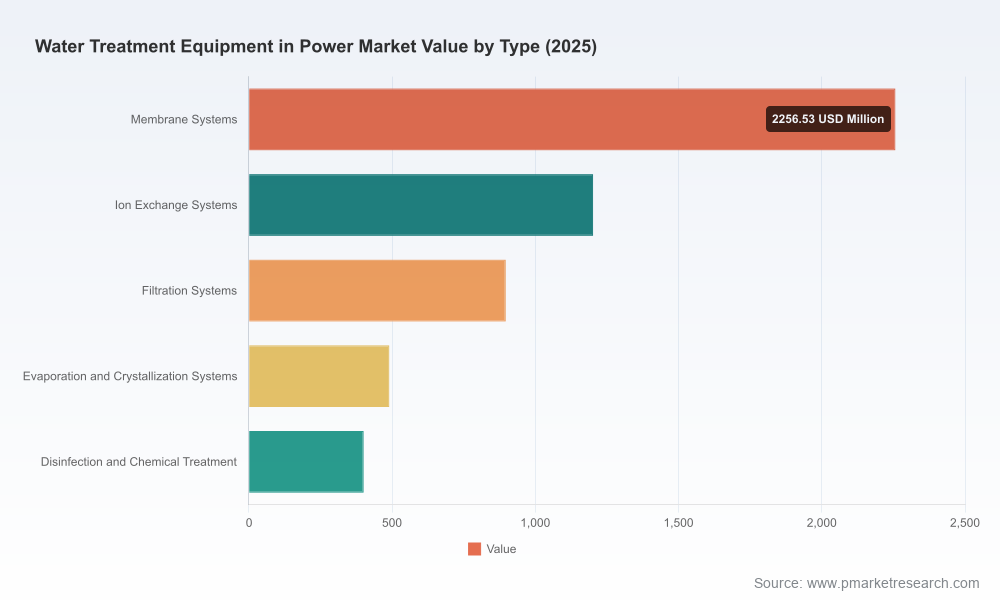

Water Treatment Equipment In Power Market

Why this briefing matters for 2026

Power-sector water treatment is no longer a back-office engineering line item: it sits at the nexus of operational reliability, regulatory compliance, and decarbonization economics. Our analysis values the global water treatment equipment market for power at approximately USD 5,245.8 Million in 2025 and projects it to approach USD 7,784.2 Million by 2032, reflecting a compound annual growth rate (CAGR) of 5.8% across the forecast period. That trajectory captures both base demand for high-purity boiler and cooling water and accelerating spend tied to wastewater reuse, zero liquid discharge (ZLD) projects, and regulatory-driven retrofits.

Water Treatment Equipment In Power Market

For corporate leaders making 2026 capital allocation, procurement, and M&A choices, this report provides a structured way to prioritize investments that reduce outage risk, lower lifecycle costs, and create optionality as generation mixes shift. Below we summarize the operational levers and strategic responses the full report equips you to deploy.

Water Treatment Equipment In Power Market

Executive takeaways: strategic priorities and decision triggers

- Protect asset uptime with targeted high-purity interventions: Boiler feed and condensate polishing remain mission-critical. Our analysis ties reliability improvements to measurable reductions in forced outages and maintenance spend, making case-by-case investments in membrane polishing, ion exchange upgrades or mobile rental assets financially defensible within typical outage cycles.

- Treat water as a strategic resource: Water scarcity and discharge regulation are elevating reuse and ZLD as board-level priorities. Projects that pair membranes, thermal concentration, and crystallization deliver compliance and water security but require early-stage scope and CAPEX planning to be competitive on 2026 procurement timetables.

- Design for regulatory shock: Emerging PFAS rules and tightening discharge limits are already reshaping technology selection—expect increased demand for granular activated carbon (GAC) processing and reactivation capacity, and for robust treatment trains that can be adapted in the field.

- Digitize to reduce OPEX: Remote monitoring and predictive analytics reduce chemical dosing, energy consumption, and unplanned downtime. Our benchmarking shows best-in-class operators capture both steady-state cost reductions and faster fault response through integrated digital platforms.

- Mitigate supply-chain criticality: Ion exchange resins, membranes and activated carbon are concentration points. Sourcing strategies that combine multi-supplier frameworks, local reactivation capacity, and contingency rental solutions materially reduce program risk.

What the full report delivers (practical toolkit for 2026)

This is an operationally-focused study, designed for decision-makers who need to move from strategic intent to executable programs within 12–24 months. The report contains:

- Market sizing and forecast with scenario modeling across 2026–2032 (including a baseline CAGR of 5.8%) and sensitivity analysis for regulatory and commodity shock scenarios.

- Technology roadmaps and deployment playbooks that compare membranes, ion exchange, evaporation/crystallization and chemical/disinfection approaches by lifecycle cost, footprint, and retrofit complexity.

- Procurement and CapEx templates, including typical procurement timelines, vendor selection criteria, and total cost of ownership (TCO) calculators aligned to outage and expansion cycles.

- Vendor benchmarking and competitive positioning matrix covering technology depth, service delivery models, digital capabilities and global project execution capacity.

- Case studies and implementation blueprints for reuse/ZLD projects, mobile rental deployments for urgent capacity, and PFAS-focused retrofits.

- Supply-chain criticality maps and mitigation strategies for resin and carbon supply, with practical steps to secure continuity and price resilience.

Competitive landscape: capabilities and strategic moves to watch

The market sits between fragmentation and consolidation; our CR3 and CR5 analysis highlights a moderate top-player share that leaves room for regional specialists and niche technology vendors to thrive. Below we synthesize the strategic positioning of the core industry players we tracked, and the implications for buyers and partners in 2026.

- Veolia Water Technologies (Paris): Strength lies in full-scope engineered systems—RO, ultrafiltration and electrodeionization—designed for power-plant steam cycles. Veolia’s integrated service offering is attractive for large thermal and nuclear operators seeking single-vendor accountability for performance guarantees.

- Xylem Inc. (Rye Brook) and Evoqua (Pittsburgh, part of Xylem): Combined capabilities bring a broad technology portfolio augmented by digital monitoring—well-suited to utilities prioritizing energy-efficient solutions. Evoqua’s rental and mobile offerings remain an important market access route for urgent capacity and retrofit windows.

- SUEZ Water Technologies & Solutions (Paris/global): Deep experience in membranes and lifecycle services positions SUEZ for long-term O&M contracts in large plants, particularly where wastewater reuse is being stacked into plant water balances.

- Kurita (Tokyo): The company’s blend of chemicals + equipment + monitoring is a compelling integrated model in markets where chemical dosing and corrosion control dominate the reliability equation—especially in heavy-industry-adjacent power fleets.

- Pentair, Ecolab (Nalco), Pall (Danaher): These vendors excel in filtration, process purification and advanced monitoring. They are frequently selected for component-level reliability improvements and as partners in hybrid treatment trains.

- Aquatech, Ovivo, Doosan Enerbility, H2O Innovation: Specialists in thermal concentration, ZLD and EPC offerings—key partners for operators that must close water loops and meet stringent discharge standards while minimizing freshwater intake.

- Birchtech and materials suppliers: Specialist resin and activated carbon suppliers (including nuclear-grade offerings) are increasingly strategic suppliers. Recent product introductions and order wins show that material innovation directly influences plant-level solution selection.

Recent industry developments and implications for 2026 action plans

Two developments in early 2026 illustrate the intersecting forces shaping near-term investment:

- Specialty material launches and order wins: New nuclear-grade ion exchange resins and targeted product introductions demonstrate that material science continues to unlock performance gains—shortening project timelines for upgrades and enabling smaller-footprint retrofits. For procurement teams, this underscores the value of supplier pilots and sample qualification well ahead of scheduled outages.

- Capacity expansion in carbon reactivation: Announced investments to expand activated carbon reactivation capacity respond both to municipal PFAS regulation and to growing industrial demand, including power-sector remediation needs. Operators with PFAS exposure should evaluate local reactivation capacity as a criterion in vendor selection and in assessing lifecycle costs for GAC-use strategies.

Strategic recommendations for 2026 planning

- Prioritize hybrid solutions: Combine membranes with selective thermal concentration or chemical polishing where freshwater limits and discharge rules are tightening. Hybrid designs achieve compliance while optimizing energy use.

- Accelerate digital pilots: Require digital performance guarantees in new procurements; include remote monitoring and predictive maintenance as bid evaluation factors to realize OPEX reductions.

- Secure materials continuity: Negotiate multi-year agreements and explore co-investment in local reactivation or resin regeneration capacity to lock in supply and reduce price volatility risk.

- Design modular procurement: Use rental/mobile systems and modular packaged plants to bridge immediate capacity gaps and defer large CAPEX until regulatory clarity and technology selection stabilize.

- Use the market map for M&A and partnerships: Targeted acquisitions of niche membrane or ZLD specialists can be more accretive than broad-scale roll-ups—look for technology owners with demonstrable field performance and service delivery capability.

About the methodology

PW Consulting’s report synthesizes primary interviews with plant engineers, procurement leads and EPC contractors, proprietary vendor benchmarking, and bottom-up project-level modelling calibrated to macroeconomic and regulatory scenarios. Our forecast uses the 2025 base year and models upside and downside scenarios to stress-test investment decisions across 2026–2032.

How to access the full intelligence

This briefing is an excerpt designed to orient executives and technical leaders. The full report contains interactive dashboards, country- and application-level breakouts, vendor scorecards, procurement templates and a proprietary investment screening tool that translate market intelligence into implementable plans. To obtain the complete study, vendor shortlists and consultancy options for bespoke planning workshops, please visit PW Consulting’s report page or contact our industry team directly. The full dataset will provide the granular segmentation and pricing models necessary to finalize 2026 budgets and procurement timelines.

PW Consulting’s Water Treatment Equipment in Power Market—practical, evidence-based and designed to convert intelligence into decisions that protect assets, comply with tightening regulation, and optimize the cost of water as a strategic input.

For detailed analysis of this topic, please visit the official page:Water Treatment Equipment In Power Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com