Carbonate Ore Market 2026: Strategic Intelligence for Decisions That Matter — PW Consulting Launches In-Depth Market Study

PW Consulting today releases a strategic briefing accompanying its full Carbonate Ore Market report, designed to equip C-suite leaders, procurement chiefs, and strategic investors for the critical decision-making window opening in 2026. Built on a comprehensive historical review (2020–2025) and forward-looking modelling through 2032, the study benchmarks the industry’s current scale — which reached roughly USD 35,350 million (revenue, USD Million) in the base year of 2025 — and projects a disciplined expansion across the forecast horizon. Our models show the global carbonate ore market growing at a compound annual growth rate (CAGR) of approximately 5.12% (2026–2032), with the market trajectory taking the total to the low‑fifties (USD Million) by 2032 under the central scenario.

Carbonate Ore Market

Why 2026 Is a Strategic Inflection Point

Three converging forces make 2026 the year that strategic plays must be defined and executed. First, demand composition and end‑use transformation — from traditional construction and metallurgy to higher‑performance polymers, specialty papers, and environmental applications — are re‑shaping the revenue mix and product specs that matter to end‑buyers. Second, upstream cost pressure and reliability of supply chains are influencing procurement strategies and prompting capital investment in beneficiation and value‑added processing. Third, regulatory and ESG imperatives — most acutely visible in emerging market jurisdictions — are forcing operators to rethink processing technologies and emissions management. For boards and investors, 2026 will be a year for deciding whether to double down on organic capacity, pursue targeted M&A, or partner on technology and decarbonization initiatives.

Carbonate Ore Market

What the PW Consulting Carbonate Ore Market Report Delivers

- Proprietary supply‑demand model covering 2020–2032: granular vintage of historical flows and a scenario‑based forecast calibrated to macroeconomic and commodity cycles (central, downside, and upside scenarios).

- Price and margin connectors: rolling price curves and cost‑of‑supply ladders to help you stress‑test projects and contracts against input volatility and tightening environmental costs.

- Reserve & resource quality matrix: metallurgical profiles, recoveries, and beneficiation complexity scores to rank deposits by near‑term commercial potential.

- CapEx/Opex benchmarking: plant‑level cost comparators and engineering sanity checks for quarry expansion, crushing/grinding circuits, and thermal processing lines.

- Route‑to‑market playbooks: procurement optimization templates, offtake negotiation levers, and commercial contract structures for tiered product specifications.

- ESG and decarbonization pathways: techno‑economic assessment of emissions abatement levers (fuel switching, kiln efficiency, CCS readiness) and an investor‑grade ESG materiality matrix.

- M&A and partnership toolkit: target screening criteria, synergy capture worksheets, and integration risk checklists for consolidation or bolt‑on strategies.

- Operational due diligence protocol: metallurgical test templates, environmental permitting hot‑spots, and community/stakeholder readiness indicators.

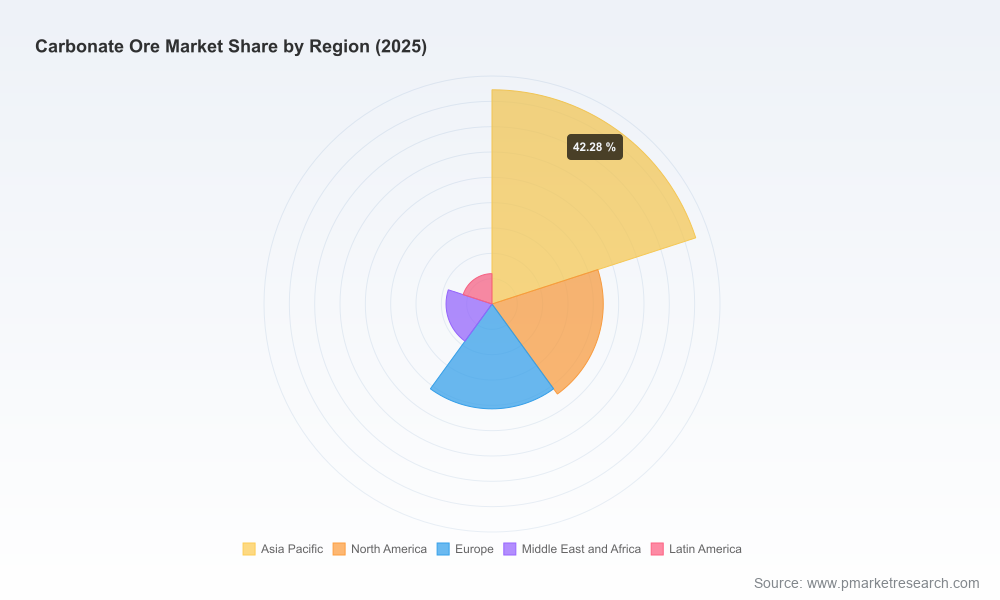

- Interactive data annex (restricted): time‑series market sizing (2020–2032), plant lists, and a searchable vendor/technology directory. Note: core segmentation data and detailed regional/application breakouts are reserved for the full report to preserve commercial value and ensure readers receive the complete dataset.

Competitive Landscape — Strategic Map

The carbonate ore space remains commercially fragmented, with the three largest producers accounting for less than 15% of global market share and the top five around one‑fifth of the market (CR3 ≈ 14.8%, CR5 ≈ 21.35%). That fragmentation creates distinct strategic opportunities depending on size and ambition.

Carbonate Ore Market

- Global integrators and performance‑materials leaders — for example, firms with a heavy industrial‑minerals focus — command differentiated market access and technical capability. These players typically invest in high‑value filler and coating applications and maintain broad geographic footprints, enabling offtake flexibility and R&D synergies.

- Regional quarry specialists and building‑materials groups are often embedded in local construction and infrastructure value chains. Their competitive advantage rests on logistics efficiency, established relationships with cement and aggregates customers, and cost control at scale.

- Technology‑led processors and specialty carbonate suppliers concentrate on engineered grades — precipitated, ground, or surface‑treated carbonates — that demand closer collaboration with downstream formulators in plastics, paper, and specialty chemicals.

- Magnesite and refractory specialists serve distinct industrial end‑markets and follow different engineering and commercial rhythms from bulk limestones.

Key names covered in our competitive intelligence include established leaders and regional champions whose strategic choices will materially shape market structure over the coming cycle:

- Omya Group (Switzerland) — a global leader in industrial minerals and specialty calcium carbonate. Their scale and R&D emphasis make them a bellwether for high‑value filler markets.

- Carmeuse (Belgium) — noted for high‑purity limestone and dolomite, with strength in steel and environmental applications.

- Lhoist Group (Belgium) — experienced in lime and dolomite processing, with deep exposure to industrial and agricultural markets.

- Imerys (France) — focuses on performance materials across plastics, paper and coatings; strategic moves here signal shifts in premium markets.

- Minerals Technologies Inc. (USA) — specialist in precipitated and ground calcium carbonates for paper and packaging segments.

- Sibelco (Belgium), Graymont (Canada), Mississippi Lime (USA), J.M. Huber Corporation (USA), CRH plc (Ireland), Nordkalk (Finland) — a mix of regional leaders and engineered‑product suppliers, each with unique strengths in feedstock, processing, or end‑market access.

- Grecian Magnesite (Greece) and RHI Magnesita (Austria) — magnesite and refractories specialists serving steel and cement industries where high temperature performance and product purity drive supplier choice.

For executives considering M&A or partnerships, the report includes a mapped matrix of strategic fits: who to buy for reserves, who to partner with for technology scale, and where bolt‑ons deliver the fastest route to margin expansion.

Technology, Raw‑Material Complexity and Regulatory Dynamics

- Beneficiation & processing complexity: Certain carbonate ores — including manganese‑associated carbonates and talc‑carbonate mixes — present fine mineral associations that require high‑intensity magnetic separation or gravity separation and dedicated metallurgical circuits. These technical realities materially affect project capex and recovery assumptions.

- Mineralogical constraints: Variants such as siderite (iron carbonate) alter processing flows and often require calcination before use in iron‑making routes; they also tend to be associated with other carbonates that complicate beneficiation and product specification.

- Regulatory tightening: Jurisdictions in Africa and elsewhere are tightening environmental requirements for mining and processing — including CO2 management and waste handling — which is already redirecting investment toward lower‑emission and higher‑recovery beneficiation methods. Such regulatory drift increases time‑to‑market and requires earlier engagement with permitting stakeholders.

- Implication for capital planning: Asset owners need to model not only commodity price risk but also retrieval risk (metallurgical recoveries), technology obsolescence, and compliance capex. Our report quantifies these vectors and translates them into investment readiness levels for project screening.

How Executives Should Use This Intelligence in 2026

- Adopt an outcomes‑based capital allocation framework: use scenario outputs to size investments across threshold IRR buckets, factoring in ESG capex and potential carbon pricing.

- Recalibrate procurement and offtake contracts: move from simple spot pricing to hybrid contracts that hedge against quality variance and processing cost inflation.

- Prioritize metallurgical due diligence: fund desktop and pilot testing early to de‑risk recovery assumptions that can make or break project economics.

- Screen M&A targets by strategic value, not just reserves: focus on proximity to customers, permitted capacity, and technology or product‑level differentiation.

- Design decarbonization pilots: test kiln fuel switching, waste‑heat recovery, and low‑carbon binders at operating quarries to create replicable blueprints for scaling emissions reductions.

Next Steps and Access

PW Consulting’s Carbonate Ore Market report is designed as an operational playbook for 2026 decisions. The press briefing above highlights the report’s strategic value while preserving the core segmentation datasets and application‑level detail for licensed readers. Corporates, investors, and advisors seeking the full dataset, interactive models, and proprietary annexes should contact PW Consulting to request access and arrange a briefing with our senior industry team. Our advisory practice also offers short, bespoke workshops to translate the report’s findings into roll‑out plans for procurement, technology investment, and M&A pipelines.

For leaders assessing near‑term capital deployment, procurement strategy, or M&A positioning in carbonate ores, the time to act is now: the market’s mid‑cycle growth and shifting supply fundamentals will crystallize into winners and losers during the 2026–2028 window. PW Consulting’s market intelligence turns complexity into clear, executable options — but the detailed segmentation and plant‑level data that drive tactical playbooks are available in the full report and accompanying datasets.

For detailed analysis of this topic, please visit the official page:Carbonate Ore Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com