High Purity Acids Market: Strategic Imperatives for 2026 — A PW Consulting Preview

Executive teaser

As global electronics, semiconductor fabrication, advanced materials and pharmaceutical production accelerate, the high purity acids market has emerged as a strategic upstream battleground. PW Consulting’s new market study — anchored on a 2025 base year and projecting through 2032 — quantifies this momentum and translates it into actionable guidance for executives planning capital, sourcing and M&A moves in 2026. With the market expanding at a projected CAGR of 7.42% through the forecast window, our analysis highlights where near‑term supply constraints, feedstock volatility and policy incentives intersect to create both risk and differentiated opportunity.

High Purity Acids Market

Market trajectory: what the topline numbers reveal

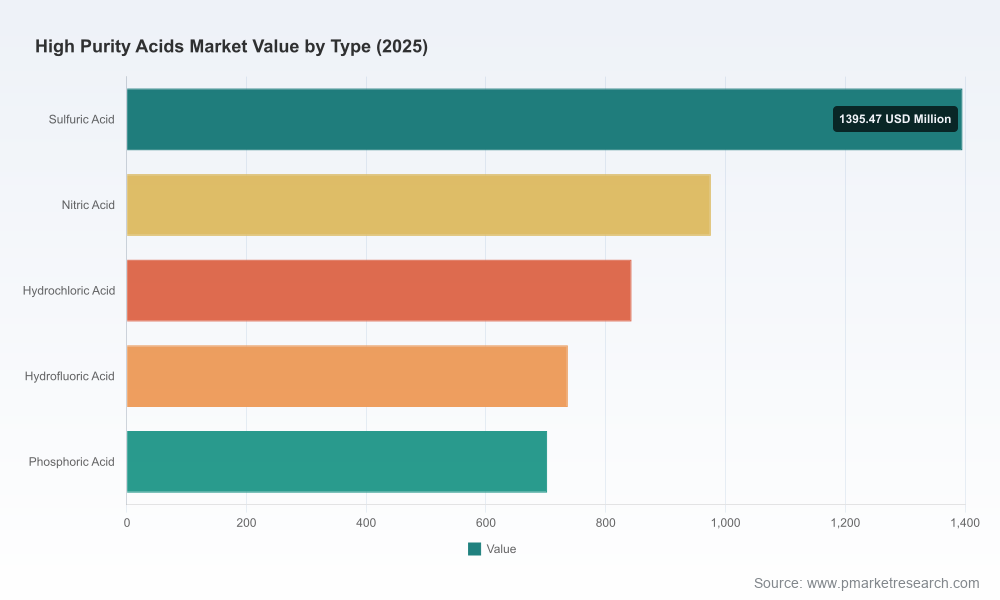

Between 2020 and 2025 the global high purity acids market demonstrated consistent expansion, driven by rising demand from semiconductor wet processing, life sciences, and renewable energy supply chains. Our base-year calibration for 2025 captures that momentum: the market sits in the multi‑billion USD bracket and continues into a growth phase in 2026 and beyond, with the forecast pathway showing sustained compound annual growth through 2032. This growth is not evenly spread — it is concentrated along a handful of critical applications and geographies, and it is meaningfully shaped by supply-side investment cycles and raw material swings.

High Purity Acids Market

Key macro drivers shaping 2026 decisions

- Electronics and semiconductor capex cycles: Ongoing fab investments and node transitions continue to raise specifications for ultra‑low impurity acids. Procurement teams and plant engineers should assume tightening technical tolerances and faster replacement cadences for consumables.

- Feedstock volatility and cost pass‑through: Elemental sulfur — the primary feedstock for many acid production routes — experienced pronounced price volatility in recent periods. That volatility has transmitted into purification costs for ultra‑high‑purity grades, compressing margins for commodity intermediaries and favoring players with secured backward integration or long‑term feedstock contracts.

- Industrial policy and on‑shoring: Regional industrial initiatives aimed at strengthening semiconductor ecosystems have incentivized local production of critical inputs. Expect governments and anchor tenants to continue prioritizing supply‑chain resilience, which will create opportunities for new capacity and for suppliers able to structure compliant, localized supply agreements.

- Regulatory and trade dynamics: Tariff regimes, environmental permitting timelines and increasingly prescriptive chemical handling rules are raising both cost and complexity for cross‑border suppliers. Buyers must bake in regulatory scenario analyses when evaluating multi‑year contracts.

Supply‑side dynamics and risk contours

Capacity additions announced by leading specialty chemical producers signal industry recognition of demand growth, but they do not eliminate execution risk. Recent investments and M&A activity have expanded the footprint for electronic‑grade and ultra‑high‑purity acids, yet the market remains sensitive to: feedstock cost shocks, long lead times for high‑purity line qualification, and logistics constraints for hazardous inbound/outbound flows.

High Purity Acids Market

Concentration metrics show a moderately consolidated landscape at the top end of the market — creating strategic implications for buyers and investors alike. A handful of incumbent suppliers maintain scale and deep technical capabilities, but pockets of regional specialization and boutique ultra‑pure producers continue to command strategic premiums. For executives, this means supplier selection is not binary: sourcing strategies that blend large‑scale anchors with nimble regional specialists often yield the optimal balance of price, lead‑time and quality assurance.

Competitive landscape — what to watch in 2026

Our competitive assessment profiles leading global and regional players that are shaping access to ultra‑pure acids for electronics, laboratory and pharmaceutical customers. These organizations combine product pedigree, manufacturing discipline and compliance capabilities in different configurations:

- BASF SE — Leveraging integrated chemical platforms and targeted investments to support regional semiconductor ecosystems; focus on qualification speed and low‑impurity grades.

- Kanto Chemical and Sumitomo Chemical — Deep engineering and product specialization tailored to electronic‑grade acids and wet process chemistries; strong customer intimacy in Asia.

- Avantor and Merck KGaA — Supply chain breadth across laboratory, pharmaceutical and electronic segments; positioning through acquisitions and dedicated ultra‑pure lines.

- Honeywell, Solvay and Entegris — Emphasis on ultra‑high purity process chemicals with strong technical support offerings for wafer‑level processing and analytical trace metal control.

- Regional specialists — Firms such as PVS Chemicals, Moses Lake Industries and several Japanese players maintain important roles in specific clusters where proximity and rapid qualification are decisive.

Recent corporate moves — capacity expansions, strategic acquisitions of specialty UHP facilities and commissioning of dedicated production lines — underscore an industry in active reconfiguration. Executives should interpret these moves as forward signaling: incumbents are securing technical capacity and customer lock‑in, while M&A and greenfield projects create selective entry points for new suppliers and private capital.

Strategic implications for 2026 corporate decisions

For leadership teams setting 2026 priorities, the accelerated normalization of elevated purity requirements combined with feedstock cost exposure yields a clear set of imperatives:

- Procurement: shift from spot to structured partnerships. Robust supplier qualification programs, multi‑year off‑take frameworks with embedded quality clauses, and optionality for localized supply are critical. The most resilient contracts will include triggers for feedstock pass‑through, agreed escalation mechanisms and shared risk provisions for force majeure related to raw material shortage or logistics disruption.

- Operations: invest in specification harmonization and inbound quality controls. Process engineering teams should prioritize inline monitoring, tighter acceptance testing and vendor scorecards tied to impurity profiles rather than solely to nominal grades. This reduces failed batch risk during qualification of new lines or when switching suppliers.

- CapEx and site selection: New acid purification lines require not only capital but extended qualification timelines. Decisions on greenfield vs. tolling should be informed by scenario modeling that includes regulatory permitting timelines and potential supply chain localization incentives from regional policy.

- M&A and JV screening: Look for targets with certified quality systems, cleanroom‑compatible packaging solutions, and proximity to end customers. Smaller, specialized producers with strong technical documentation and rapid qualification capabilities can be accretive to integrated suppliers seeking to broaden product portfolios.

- Risk management and hedging: Given feedstock volatility, senior finance teams should evaluate integrated hedging strategies — from long‑term feedstock contracts to financial hedges — coupled with product pricing provisions that protect margin while retaining competitiveness.

What PW Consulting’s report delivers — practical, executable content

We designed the report as a decision‑grade toolkit for commercial, procurement and strategy teams. Highlights include:

- Market sizing and projection model (base year 2025; forecast 2026–2032) with scenario toggles that allow leaders to stress‑test demand under alternative fab capex and feedstock cost assumptions.

- Supplier scorecards and a capability map that evaluate not only capacity but qualification speed, packaging and contamination control practices — presented in a format tailored for sourcing RFIs and RFPs.

- Practical playbooks for contract design, local compliance checklists, and an operational readiness matrix for bringing UHP acid supply online in proximity to wafer fabs or pharma clusters.

- Transaction support materials for M&A diligence: sample technical due diligence templates, integration risk heatmaps, and a shortlist of acquisition criteria that prioritize scalability and traceability.

- Procurement levers and costsaving opportunities identified through benchmarking of purification routes, logistics optimizations and waste‑minimization programs.

To preserve commercial confidentiality and competitive integrity, the report intentionally omits granular disclosure of proprietary customer relationships and certain per‑plant financials in the public summary. Subscribers receive the full dataset and supplier matrices to enable immediate sourcing or investment action.

Methodology and confidence intervals

Our conclusions are grounded in iterative triangulation: company filings and press releases, proprietary supplier interviews, trade and customs analytics, and on‑the‑ground validation with fabs and laboratory users. The forecast model embeds sensitivity bands around feedstock cost trajectories and regional policy adoption rates, enabling users to examine upside and downside scenarios relevant for 18–36 month planning horizons.

How executives should use this report in 2026

- Chief Procurement Officers: Rebase supplier scorecards and renegotiate framework agreements with explicit purity and logistics KPIs before contracts roll into their next renewal window.

- Head of Operations/Engineering: Prioritize investments in inbound analytical capabilities and supplier co‑qualification programs to reduce qualification time for new acid lines.

- Corporate Development: Use our M&A diligence toolkit to filter opportunities where certification, traceability and customer proximity create defensible premiums.

- Risk & Compliance: Integrate the report’s regulatory scenario outputs into stress testing for 2026 business continuity plans, particularly for cross‑border flows of hazardous materials.

Final note — why this is a must‑read for 2026 planning

The high purity acids market sits at the nexus of advanced manufacturing and raw material exposure. Our study quantifies where growth will appear, but—critically—translates that quantification into operational steps and contracting constructs that materially reduce execution risk. PW Consulting’s synthesis enables decision makers to convert headline growth into secured supply, validated quality, and defensible margins.

Next step

This preview intentionally omits core segment tables and certain supplier‑level metrics to protect commercially sensitive detail. For access to the full report — including the complete regional and application market split tables, supplier scorecards, scenario model sheets and downloadable RFP templates — please visit the PW Consulting report page or contact our research team to schedule a data demo and tailored briefing.

For detailed analysis of this topic, please visit the official page:High Purity Acids Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com