Vehicle Motorized Door Industry Perspective: Market Size, Share, Current Trends, and Forecast by 2032

Other |

2026-06-02 10:07:53

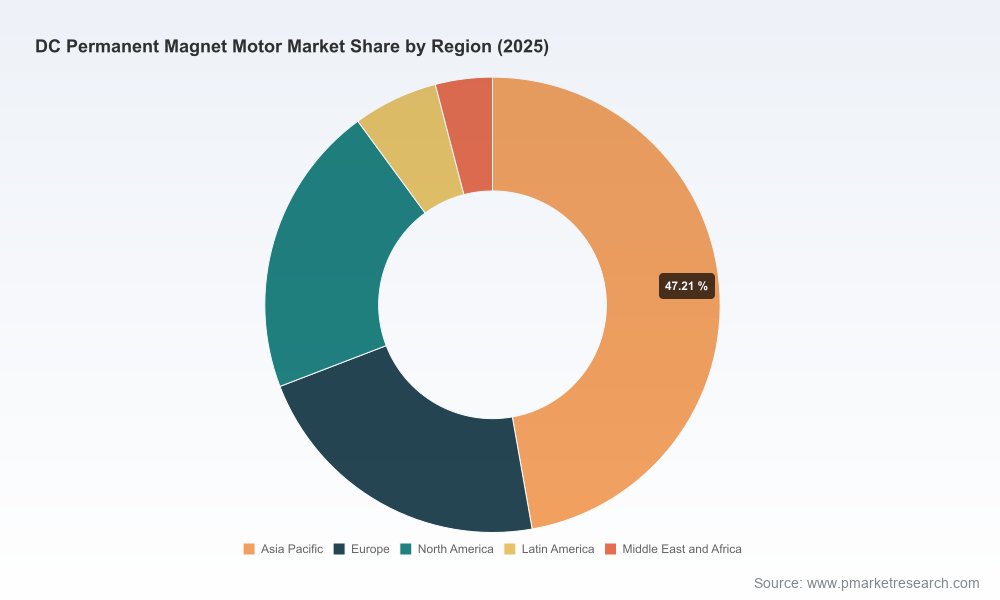

PW Consulting’s new Dc Permanent Magnet Motor Market report delivers a pragmatic, board‑level playbook for organizations that must translate the sector’s steady growth into durable competitive advantage. Our analysis shows the global market — measured on a consistent USD million basis — reached roughly USD 41.9 billion in 2025 and is forecast to expand at a compound annual growth rate (CAGR) of about 6.5% over the 2026–2032 forecast window, reaching an estimated USD 65.1 billion by 2032. These headline figures capture a market that is large, growing and simultaneously being reshaped by raw material dynamics, regulation, and shifting end‑use economics.

Dc Permanent Magnet Motor Market

Actionable foresight: 2026 is a hinge year for procurement, product roadmaps and regional manufacturing footprints. Our report converts macro momentum into decision‑ready intelligence — including scenario models for pricing, supplier continuity and technology adoption — so executives can set strategy that anticipates disruptions rather than reacts to them.

Dc Permanent Magnet Motor Market

Risk‑to‑return calibration: With market concentration measured as modest (CR3 ≈ 28.4%; CR5 ≈ 42.2%), incumbents and challengers alike must weigh consolidation, vertical integration and partnership as imperfect substitutes for operational agility. Our work frames which levers yield the highest expected risk‑adjusted returns by 2028 and beyond.

Dc Permanent Magnet Motor Market

Compliance and competitiveness: New and evolving energy efficiency standards and raw material supply constraints are non‑negotiable drivers of product design and go‑to‑market strategy. The report lays out compliance timetables and cost impact pathways so product and regulatory teams can align by mid‑2026.

The market’s projected expansion at a 6.5% CAGR through 2032 is not evenly distributed across technologies or end‑uses, but the aggregate growth signals sustained demand across electrification, automation and high‑precision applications. For strategy teams, the key takeaway is that base demand provides ample runway for differentiated players, while structural shifts (materials, regulations, and systems integration) will be the primary determinants of margin and share outcomes.

This report is organized around modules designed for immediate operationalization by C‑suite and business unit leaders:

Market sizing and top‑down scenario models — baseline, constrained supply and accelerated demand cases to stress‑test volume and price assumptions through 2032.

Supplier and material risk matrix — granular guidance on sourcing strategies, inventory hedging and strategic partnerships for magnet materials and other key inputs.

Regulatory impact playbook — timelines and compliance cost estimates related to recent efficiency standards and their implications for motor design and retrofit markets.

Go‑to‑market and channel strategies — differentiated approaches for automotive, industrial, medical and other system integrators that balance direct sales, distribution and OEM partnerships.

Technology and R&D prioritization framework — investment logic for control electronics, magnet optimization, and system‑level integration to maximize lifetime value.

M&A and partnership playbook — valuation heuristics and capability maps to guide bolt‑on versus platform acquisition decisions.

The sector combines global systems players, specialized motor houses and a robust cohort of precision OEMs. Executives should focus on capability adjacencies as much as market share numbers — innovation cycles and application domain expertise are decisive.

Nidec Corporation (Kyoto, Japan; https://www.nidec.com) — broad PMDC portfolio and scale across industrial and consumer markets position Nidec as a volume and systems integrator. Expect continued investments in efficiency upgrades and integrated drive systems.

ABB Ltd. (Zurich, Switzerland; https://new.abb.com/motors-generators) — leverage in automation and industrial drives, with a focus on energy‑efficient permanent magnet solutions targeted at large OEMs and infrastructure projects.

Siemens AG (Munich, Germany; https://www.siemens.com) — strength in process industries and motion control, where system reliability and lifecycle services command premium economics.

WEG S.A. (Jaraguá do Sul, Brazil; https://www.weg.net) — provides cost‑competitive PM solutions for industrial and specialist applications, often winning on total cost of ownership.

Johnson Electric, Maxon Motor and Portescap — represent segments where miniaturization, precision and high‑reliability engineering open margin opportunities in automotive, medical and aerospace niches.

Mid‑tier and regional specialists (Kollmorgen, Parvalux, MET Motors, ElectroCraft, Mabuchi, Twirl Motor and Hansen Motors) — these players compete on customization, speed to market and application engineering.

Recent vendor activity — trade shows, catalog releases and certification updates in 2025 — indicates an active competitive landscape where product refreshes and compliance announcements are being used to secure design‑wins and sustain channel momentum.

Two external forces demand immediate attention from procurement and strategy teams:

Rare earths and magnet supply: Elevated prices and constrained availability of neodymium and NdPr are reshaping cost structures. These dynamics increase the value of magnet efficiency improvements, alternative material pathways and backward integration options. Companies should model sensitivity of gross margins to magnet price shocks and identify realistic mitigation strategies (long‑term contracts, inventory hedging, magnet recycling partnerships).

Energy efficiency regulation: Amended energy conservation standards for expanded scope electric motors in key markets introduce new minimum performance baselines. Compliance timelines mean R&D roadmaps must prioritize higher efficiency topologies and validated life‑cycle testing within current product development cycles to avoid retrofit costs or market access restrictions.

Additionally, geopolitical and policy actions — including export controls on rare earth elements in strategic supply jurisdictions — create regional sourcing asymmetries that affect where to locate assembly versus high‑value R&D.

Recast procurement from cost‑only to cost‑resilience: negotiate multi‑year magnet supply agreements with built‑in flexibility and consider strategic inventory to buffer short‑term price spikes.

Prioritize efficiency upgrades in new product designs: allocate near‑term R&D budget toward motor topologies and control electronics that reduce magnet usage per unit of performance.

Embed regulatory compliance into product roadmaps: ensure that testing, certification and documentation timelines are integrated into 2026 launch plans to avoid missed opportunities in regulated segments.

Adopt a layered market entry strategy: combine selective direct penetration in high‑value verticals (medical, aerospace) with distribution and OEM partnerships in commoditized industrial channels.

Evaluate targeted M&A and JV plays: use the report’s capability maps to identify bolt‑on targets that accelerate electrification, control‑electronics know‑how or magnet recycling capabilities.

Stress‑test financial plans: run scenarios that reflect both a constrained material supply and faster‑than‑expected adoption of high‑efficiency standards to determine breakeven investment levels for new product lines.

Strategy teams will find this report most useful as a decision‑support tool in three practical ways: (1) as an empirical basis for capital allocation and R&D prioritization; (2) as a procurement playbook for managing magnet and component risk; and (3) as a market access guide for aligning product portfolios with evolving regulatory frameworks. The report’s scenario models and supplier risk matrix are specifically calibrated to inform board‑level discussions scheduled in H1 and H2 of 2026.

The DC permanent magnet motor market presents a clear growth runway, but converting top‑line expansion into sustained profit pools requires disciplined responses to materials and regulatory pressures, sharper product differentiation, and nimble customer engagement models. PW Consulting’s Dc Permanent Magnet Motor Market report equips leaders with the quantitative forecasts, operational playbooks and competitive intelligence needed to make high‑return decisions in 2026. For access to full segmentation, granular scenario outputs and supplier risk matrices — content intentionally summarized here to protect the depth of our proprietary analysis — visit the official report page to obtain the complete dataset and executive toolkit.

For detailed analysis of this topic, please visit the official page:Dc Permanent Magnet Motor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com